According to the 2026 Federal Reserve Report on Employer Firms, 22% of small business applicants received no financing at all, while another 36% received only part of what they sought. Meanwhile, the share of businesses turning to online fintech lenders nearly doubled — from 17% in 2020 to 29% in 2025 — as traditional banks tightened their standards.

Unsecured business loans fill that gap. No collateral required. Approval based on your revenue, credit history, and business profile. And in many cases, funding within days.

This guide covers the best unsecured business loan options in 2026, what separates them, and how to choose the right fit for your business.

Key Takeaways

- Unsecured business loans require no collateral — lenders assess creditworthiness, revenue, and business history instead

- Minimum credit scores range from 500 (Fundible) to 700 (Bank of America) depending on the lender

- Online lenders typically fund in 24–48 hours; traditional banks may take days to weeks

- Most unsecured loans still require a personal guarantee — review terms carefully before signing

- Poor credit or prior bank rejections don't disqualify you — marketplace lenders and financing intermediaries offer viable alternatives

What Are Unsecured Business Loans?

An unsecured business loan provides capital without requiring the borrower to pledge assets as collateral. As the SBA explains, lenders instead evaluate your cash flow, creditworthiness, and repayment ability to assess risk.

That means no appraisals, no lien on your equipment, and no requirement to put up property upfront.

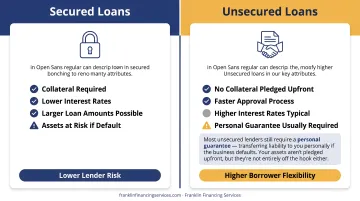

Secured vs. Unsecured: Key Differences

| Factor | Secured Loans | Unsecured Loans |

|---|---|---|

| Collateral required | Yes (property, equipment, inventory) | No |

| Interest rates | Generally lower | Generally higher |

| Loan amounts | Higher maximums | Lower maximums |

| Approval speed | Slower (asset appraisal needed) | Faster |

| Application complexity | More documentation | Simpler |

| Personal guarantee | Sometimes | Usually required |

That said, most unsecured lenders still require a personal guarantee. This transfers liability to you personally if the business defaults — so while your assets aren't pledged upfront, they're not entirely off the hook either.

Common Uses for Unsecured Business Loans

- Working capital and payroll

- Inventory purchases

- Marketing and growth campaigns

- Equipment upgrades (smaller purchases)

- Business expansion or new locations

- Startup capital for newer ventures

- Debt consolidation

Best Unsecured Business Loans in 2026

These lenders were selected based on approval accessibility, funding speed, loan flexibility, interest rates, and suitability across different credit profiles and business types. The list spans lending marketplaces, direct lenders, and a traditional bank — covering credit scores from 500 to 700+ and loan sizes from $30,000 to $6 million.

Lendio — Best for Comparing Multiple Lenders

Lendio is a lending marketplace that connects small business owners with 75+ lending partners through a single application. Rather than making credit decisions itself, Lendio submits your profile across its network — making it the most efficient way to compare multiple offers without multiple hard pulls.

What stands out:

- Loan types include term loans, lines of credit, SBA loans, equipment financing, and revenue-based financing

- Unsecured financing available up to $2 million through the marketplace

- Funding available as soon as 24 hours after approval

- Credit score requirements start around 625 for unsecured products (varies by partner)

| Detail | Info |

|---|---|

| Starting Rate | From 6% (term loans); lines of credit from 8%–60% |

| Max. Funding Amount | Up to $2M (unsecured); up to $5M across all products |

| Min. Credit Score | ~625 (unsecured); varies by partner lender |

The main advantage: one application generates competing offers, which gives you real leverage when choosing terms.

Kapitus — Best for Revenue-Based Financing

Kapitus operates as both a direct lender and marketplace, offering revenue-based financing, term loans, lines of credit, and equipment financing. It's particularly well-suited for businesses with strong monthly revenue but irregular or seasonal cash flow.

What stands out:

- Flexible payment schedules — daily, weekly, or monthly

- Up to $5 million in funding across product types

- Revenue-based options don't rely solely on credit score

- Minimum credit score of 625

One drawback: rate transparency requires speaking with a representative, which some borrowers find frustrating compared to lenders that publish clear APR ranges upfront.

| Detail | Info |

|---|---|

| Starting Rate | From ~6.2%–6.25% (verify current rate at kapitus.com) |

| Max. Funding Amount | Up to $5 million |

| Min. Credit Score | 625 |

Bank of America — Best Traditional Bank Option

For established businesses that prefer working with a major institution, Bank of America offers unsecured term loans and business lines of credit with competitive starting rates. Its requirements are stricter, but so are its terms — in a good way.

What stands out:

- Fixed rates as low as 7.00% APR (effective March 23, 2026)

- SBA loan access for government-backed options

- Requires 2 years in business under current ownership and $100,000+ annual revenue

- Repayment terms from 12 to 60 months

The 700 minimum FICO score makes this a poor fit for lower-credit borrowers, but for creditworthy business owners who qualify, it's one of the most cost-effective unsecured options available.

| Detail | Info |

|---|---|

| Starting Rate | From 7.00% APR |

| Max. Funding Amount | Up to $100,000 (unsecured; verify at bankofamerica.com) |

| Min. Credit Score | 700 |

Fundbox — Best for Startups and Newer Businesses

Fundbox offers revolving business lines of credit with some of the most accessible entry requirements on the market — just 3–6 months in business and a 600 minimum FICO score. That makes it one of the few legitimate options for businesses that haven't yet built a long financial track record.

What stands out:

- Soft credit pull for prequalification — no impact on your score until you draw funds

- Draw only what you need; pay interest only on what you use

- Funding as soon as the next business day after approval

- $30,000+ annual revenue required

The trade-off: repayment terms are shorter and costs run higher than traditional lenders. Fundbox fees for a 12-week repayment schedule start at 4.66% of the drawn amount — that's a fee, not an APR — the true annualized cost runs significantly higher.

| Detail | Info |

|---|---|

| Starting Rate | From 4.66% (12-week term fee on drawn amount) |

| Max. Funding Amount | Up to $250,000 |

| Min. Credit Score | 600 |

Fundible — Best for Businesses with Lower Credit Scores

Fundible is an online lending marketplace designed to serve businesses across all credit profiles, including scores as low as 500. If you've been turned down by traditional banks or stricter alternative lenders, Fundible may be the most accessible option available.

What stands out:

- Minimum 500 FICO score — one of the lowest thresholds in the market

- Requires 6+ months in business and $8,000+ in average monthly revenue

- Products include term loans, lines of credit, equipment financing, bridge loans, invoice factoring, and SBA loans

- Line of credit rates start at 1% per month (approximately 12% annualized, before fees)

Note that borrowing costs can be higher for lower-credit borrowers, and the full fee structure isn't always disclosed upfront — get everything in writing before committing.

| Detail | Info |

|---|---|

| Starting Rate | From ~1% per month (≈12% annualized) |

| Max. Funding Amount | Up to $250,000 (line of credit); up to $6M (term loans) |

| Min. Credit Score | 500 |

Pros and Cons of Unsecured Business Loans

Advantages

- No collateral requirement — business and personal assets stay protected upfront

- Faster approvals — no asset appraisal means quicker processing

- Simpler documentation — especially with online lenders

- Flexible use of funds — working capital, payroll, expansion, and more

Disadvantages

- Higher interest rates than secured equivalents

- Shorter repayment terms — often 1–3 years versus 5–25 for secured options

- Lower maximum amounts in most cases

- Personal guarantee often required — transfers default liability to you personally

When an Unsecured Loan Is NOT the Right Fit

Skip unsecured if you're financing long-term capital expenditures, large equipment purchases, or commercial real estate — secured loans or SBA programs deliver lower rates and better terms for those use cases. If your business qualifies for an SBA 7(a) loan, that's worth pursuing first.

How We Chose the Best Unsecured Business Loans

Evaluation Criteria

Each lender in this guide was assessed across six factors:

- Interest rate competitiveness: starting APR or equivalent cost across lenders

- Maximum funding amounts: whether limits realistically match business needs

- Credit score accessibility: minimum FICO thresholds required for approval

- Approval and funding speed: time from application to capital in hand

- Loan type variety: flexibility to cover different business situations

- Transparency of terms: how clearly fees, guarantees, and prepayment penalties are disclosed

What Business Owners Often Miss

Rate comparisons alone don't capture the full cost. NerdWallet notes that business loan prepayment penalties commonly range from 1%–5% of the remaining balance — a cost that doesn't show up in the headline rate.

Beyond rate, evaluate:

- Payment structure fit — does daily, weekly, or monthly repayment match your cash flow cycle?

- Personal guarantee terms — what happens to your personal assets if the business can't repay?

- Total cost of borrowing — including origination fees, draw fees, and any monthly maintenance charges

The best unsecured loan isn't always the cheapest. It's the one that aligns with your revenue cycle, repayment capacity, and growth timeline.

When to Work with a Financing Intermediary

If self-evaluation reveals credit challenges, recent bank rejections, or a non-traditional ownership structure, applying lender-by-lender often leads to a string of hard pulls and denials. Working with a partner who has established lender relationships is a faster path.

Franklin Financing Services works as this type of intermediary. As an SBA Preferred Financial Services company, they match businesses with appropriate funding solutions even when traditional banks have already said no.

Their unsecured loan program has served clients across a range of profiles, including a startup manufacturer who secured $100,000 and a real estate investor who accessed $125,000, without requiring traditional collateral.

Conclusion

The right unsecured business loan in 2026 depends on your credit profile, revenue, time in operation, and how quickly you need capital. A startup with a 610 credit score has completely different options than an established business with a 740, so there's no universal answer here.

Before signing anything, assess:

- Total loan cost, including fees and factor rates, not just the stated interest rate

- Personal guarantee terms and what assets you're putting at risk

- Repayment structure — match payment frequency to your actual cash flow

If you've been turned away by banks or aren't sure where to start, Franklin Financing Services offers a free evaluation of your financing needs. Their team of certified financial professionals works as an SBA Preferred Financial Services company, connecting businesses with lenders across 16+ product categories — including options for challenging credit profiles and prior bank turndowns.

Connect with Franklin Financing Services for a free financing evaluation →

Frequently Asked Questions

Who is eligible for unsecured business loans?

Eligibility varies by lender. Most require a minimum credit score between 500 and 700, a set period in business (as few as 3–6 months for online lenders, up to 2 years for banks), and a minimum revenue threshold. Businesses with poor credit can still qualify through marketplace lenders like Fundible, which accepts scores as low as 500.

How much is the monthly payment on a $50,000 unsecured business loan?

It depends on your rate and term. At 10% APR over 24 months, expect roughly $2,307/month; over 60 months, about $1,062/month. At 15% APR, those figures rise to approximately $2,424 and $1,190 respectively. Use a business loan calculator to model your specific scenario before applying.

Can I get an unsecured business loan with bad credit?

Yes. Lenders like Fundible accept scores as low as 500, and marketplace platforms like Lendio can match lower-credit borrowers with appropriate partners. Expect higher rates and lower loan amounts. Working with a financing intermediary like Franklin Financing Services — which has relationships with multiple national lenders — improves your chances of finding a workable match.

What is the difference between a secured and unsecured business loan?

Secured loans require collateral, such as property, equipment, or inventory, and typically offer lower rates and higher amounts as a result. Unsecured loans require no collateral but carry higher rates, shorter terms, and in most cases a personal guarantee that holds the business owner personally liable for repayment.

How fast can I get funded with an unsecured business loan?

Online lenders can approve and fund within 24 to 48 hours — some even fund as soon as the next business day. Traditional banks may take several days to weeks. The absence of a collateral appraisal is the primary reason unsecured loans process faster.

What documents do I need to apply?

Typical requirements include a government-issued ID, 3–6 months of business bank statements, business license or registration, and a voided check. Some lenders also request business tax returns or financial statements. Online lenders generally require fewer documents — some require only an application and recent bank statements.