Introduction

Real estate investing in 2026 offers genuine opportunity, but the financing landscape is more demanding than it was a few years ago. According to the Mortgage Bankers Association, the spread between investment property mortgage rates and primary residence rates has widened to nearly 1.5 percentage points — a gap that's squeezing margins on deals that would have penciled out easily in 2021.

Many investors struggle with one core challenge: matching the right loan structure to the right deal. Bank lending standards remain selective, the menu of available loan types has expanded significantly, and choosing the wrong financing path can kill a deal before it closes.

This guide covers investors at every stage — whether you're buying a first rental property, running fix-and-flip projects, or scaling a multi-property portfolio. You'll find a clear breakdown of conventional mortgages, DSCR loans, hard money, seller financing, government-backed programs, and alternative options, plus a framework for choosing the right path when traditional lenders pass.

Key Takeaways

- Investment property loans require 15–25% down payments, higher credit scores, and stronger reserves than primary residence mortgages

- DSCR loans qualify based on rental income — not W-2 income — making them ideal for self-employed investors and LLC borrowers

- Hard money and bridge loans close fast but carry rates typically ranging 9–14% and short repayment windows

- Government-backed loans (FHA, VA, SBA) can lower entry barriers for investors purchasing owner-occupied multifamily properties or small business real estate

- Bank rejection is not the end — alternative lenders and financing intermediaries serve investors that traditional banks won't touch

Why Real Estate Investment Financing Works Differently in 2026

The rate gap between investment properties and primary residences is real and meaningful. According to Bankrate, investors should expect to pay 1–2 percentage points more than owner-occupied loans — with investment property 30-year fixed rates sitting around 6.59% in June 2026, compared to roughly 6.34% for primary residences. That spread has a direct impact on how you analyze deals.

How Lenders Evaluate Investment Properties Differently

The bigger difference lies in how lenders underwrite the loan, not just the rate.

Traditional banks evaluate the borrower: personal income, W-2 history, debt-to-income ratio, and credit score. Investment property lenders evaluate the asset: what does the property generate, and can that income service the debt? This distinction opens or closes financing paths depending entirely on your financial profile.

Because borrowers are statistically more likely to default on an investment than their primary home, lenders respond with stricter requirements:

- Credit score minimums of 640–680+ depending on unit count and LTV (per the Fannie Mae April 2026 Eligibility Matrix)

- Down payments of 15% for single-unit properties and 25% for 2–4 unit properties under conventional guidelines

- Reserve requirements of at least 6 months of PITIA payments for manually underwritten investment properties

Of these three, the reserve requirement catches the most investors off guard — having 6+ months of payments sitting idle is a real capital commitment that affects how much you can deploy elsewhere.

Traditional Real Estate Investment Financing Options

Conventional Investment Property Mortgages

The conventional mortgage remains the baseline option for investors with strong W-2 income and solid credit. It works like a standard home loan but with stricter parameters:

- Down payment: 15% (single-unit) or 25% (2–4 units)

- Underwriting: personal income, credit score, DTI ratio all evaluated

- Rate premium: expect 1–2% above primary residence rates

- Best for: investors with documentable income who plan to hold properties long-term

You get lower rates and longer terms, but full personal income documentation is required. If your income is complex or your portfolio is already large, this path narrows quickly.

DSCR Loans

DSCR (Debt Service Coverage Ratio) loans have become one of the most useful tools for rental property investors. Instead of your W-2 or tax returns, lenders evaluate whether the property's rental income covers its debt payments.

Most lenders require a DSCR of 1.0–1.25, meaning the property needs to generate at least as much income as the monthly payment, ideally 25% more. According to S&P Global Ratings, DSCR loans now make up over half the non-QM securitized loan population — a reflection of how much demand exists for income-based underwriting.

Key features:

- No personal income documentation required — self-employed investors and LLC borrowers qualify on property cash flow

- Available for single-family, multi-family, and short-term rentals

- Typically 30-year fixed or adjustable terms

- Property must be rent-ready to qualify — this distinguishes DSCR from hard money loans

For Griffin Funding borrowers using DSCR products in 2025, the average credit score was 739, though many lenders start at 620+.

Home Equity-Based Financing

Investors who already own property can use that equity to fund new acquisitions without going through a full loan application:

- HELOC: Revolving credit line secured by existing equity — useful for ongoing deal flow

- Home equity loan: Lump sum at a fixed rate, better for single acquisitions

- Cash-out refinance: Replace your existing mortgage with a larger one and take the difference as cash

The advantage is typically lower rates than investment-specific loans. The core risk: your existing property is the collateral. If the new investment underperforms, you're putting what you already own on the line.

Portfolio Loans and Construction Financing

Portfolio loans are originated and held by the lender rather than sold to the secondary market. This unlocks flexible underwriting — useful for investors with multiple properties, non-standard income, or LLC ownership structures. They're also the standard tool for scaling beyond Freddie Mac's 10-property limit on conventional financing.

Construction loans work differently: funds are released in stages as building milestones are completed. Key terms to know:

- Typical duration: 6–18 months with Loan-to-Cost (LTC) ratios set at origination

- Draw-based structure keeps interest costs lower than borrowing the full amount upfront

- At completion, you exit via a sale or refinance into a permanent loan

The staged funding requires active project management, but it's well-suited to ground-up builds and major renovations.

Alternative and Creative Financing Options

Hard Money, Seller Financing, and Private Money

Hard money loans are the fix-and-flip investor's primary tool. These are short-term, asset-based loans underwritten on the property's After-Repair Value (ARV) rather than borrower income. Approvals happen within days, making them viable for distressed property acquisitions where speed matters.

Current benchmarks:

- Rates typically 9–14% depending on experience and project details

- Many lenders cap total loan amounts at 70–75% of ARV

- Terms generally 6–18 months

That speed comes at a price. Hard money is significantly more expensive than conventional financing, so it works best for flips where the deal margin is strong — not for long-term holds.

Seller financing removes the bank entirely. The seller acts as the lender, with terms negotiated directly. This can mean lower closing costs, faster timelines, and more flexible structures — but the seller must be willing, and many deals include balloon payments that require refinancing within 3–7 years.

Private money is relationship-based lending from individual investors rather than institutions. Terms are typically shorter (months to a year), rates vary widely, and qualification depends on trust and track record rather than formal underwriting.

Bridge Loans

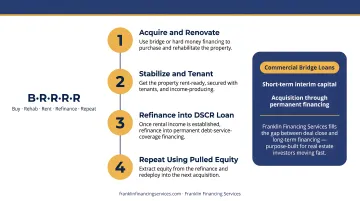

All three options above share a common use case: moving fast when a deal surfaces. Bridge loans serve the same urgency, but as structured gap financing — used to secure a property while permanent financing is arranged or another asset is sold. They're central to the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat):

- Use bridge or hard money to acquire and renovate the property

- Get the property stabilized and tenanted

- Refinance into a DSCR loan once rental income is established

- Repeat using the equity pulled out

Franklin Financing Services offers Commercial Bridge Loans specifically for investors needing short-term interim capital during transactions — filling the gap between acquisition and permanent financing.

Crowdfunding and Peer-to-Peer Lending

Real estate crowdfunding platforms let investors pool capital to fund deals or loans, with minimum investments often in the hundreds to low thousands of dollars. Zion Market Research projects the global real estate crowdfunding market will grow from $21.99 billion in 2023 to $538.79 billion by 2032 — a sign of how mainstream the model has become.

The trade-offs: limited control over the investment, profit-sharing arrangements, and often multi-year lock-up periods. Useful for passive investors or those building exposure while accumulating capital for direct deals.

Government-Backed and Specialty Loan Programs

FHA and VA Loans for Investors

These programs aren't designed for pure investors — but they're powerful entry points for house-hackers.

Key terms at a glance:

- FHA loans: 1–4 unit properties, 3.5% down (580+ credit score), flexible qualifying — requires owner-occupancy of one unit for at least one year

- VA loans: No down payment, no private mortgage insurance, up to 4 units — eligible veterans must occupy one unit

Both programs give investors access to lower-cost financing upfront. After the occupancy period, many refinance into investment-specific products to free up capacity for the next property.

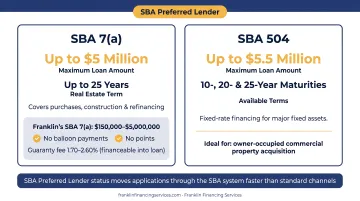

SBA Loans for Commercial Real Estate

SBA programs serve a specific but valuable niche: business owners purchasing commercial property they intend to occupy.

- SBA 7(a): Up to $5 million, terms up to 25 years for real estate, competitive rates — covers commercial real estate purchases, construction, and refinancing

- SBA 504: Fixed-rate financing for major fixed assets up to $5.5 million, with 10-, 20-, and 25-year maturities

Lender selection matters here. Working with an SBA Preferred Lender — like Franklin Financing Services — moves applications through the SBA system faster than standard channels. Franklin's SBA 7(a) program covers $150,000 to $5 million with no balloon payments and no points, which removes two of the more common friction points in conventional commercial loans.

The SBA guaranty fee of 1.70–2.60% can be financed into the loan itself, keeping upfront costs manageable.

Opportunity Zones and Self-Directed IRAs

Beyond traditional loan products, two tax-advantaged vehicles are worth knowing.

Opportunity Zone funds let investors deploy capital gains into designated real estate markets, deferring existing gains and potentially eliminating new gains on the OZ investment entirely. Novogradac reports that tracked Qualified Opportunity Funds raised $2.67 billion in 2025, up from $2.47 billion in 2024.

Self-directed IRAs let investors purchase real estate using retirement funds while deferring taxes on income and gains. Both tools carry real tax advantages — but also real complexity. Work with a tax advisor before committing capital to either structure.

How to Choose the Right Financing Option

Match Loan Type to Strategy

| Investment Strategy | Best Financing Options |

|---|---|

| Fix-and-flip | Hard money, bridge loans |

| Buy-and-hold rental | DSCR loans, portfolio loans |

| Ground-up construction | Construction loans |

| House-hacking | FHA or VA (with occupancy) |

| Commercial property | SBA 7(a), commercial bridge loans |

| Existing equity available | HELOC, cash-out refinance |

Evaluate Your Financial Profile Honestly

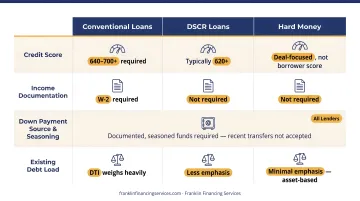

Before applying, assess these factors — each financing type weighs them differently:

- Credit score: Conventional loans need 640–700+; DSCR loans typically start at 620+; hard money lenders focus on the deal, not the borrower

- Income documentation: W-2 required for conventional; not required for DSCR; not required for hard money

- Down payment source and seasoning: Most lenders require documented, seasoned funds — not recent transfers

- Existing debt load: DTI matters heavily for conventional; less so for DSCR and asset-based loans

Look Beyond the Interest Rate

Total cost of financing includes more than the rate:

- Origination fees and points

- Prepayment penalties (common on hard money)

- Draw fees on construction loans

- Reserve requirements that tie up capital

- Balloon payment timelines

Always get a full term sheet in writing. Stress-test the deal at 0.5–1% above the quoted rate: if the numbers stop working at a slightly higher rate, the margin isn't thick enough.

When Traditional Banks Say No

A bank rejection leaves more options open than most investors expect. Those with imperfect credit, recent late payments, or non-standard income can still find workable paths:

- Hard money lenders focus on the asset, not the borrower

- Private money lenders work on relationships and deal quality

- Seller financing removes bank qualification entirely

- Financing intermediaries like Franklin Financing Services match investors to lenders across a broad network — including programs for borrowers that standard banks won't serve

Franklin's FAST TRACK program provides approvals within 24–48 hours using just a loan application and four months of bank statements. For investors who need capital quickly or have been turned away elsewhere, a financing partner that specializes in non-standard situations can keep viable deals from dying on the vine.

Frequently Asked Questions

What is the outlook for real estate investment in 2026?

CBRE projects multifamily construction starts have fallen 74% below their 2021 peak, pointing toward supply shortages and above-average rent growth. Rental demand remains strong — as of Q3 2024, average new mortgage payments were 35% higher than average apartment rents, keeping renters in the market.

How do real estate investors get financing?

Investors use traditional banks, private lenders, government-backed programs, and non-bank intermediaries. Unlike primary residence mortgages, investment property loans are often underwritten on the property's income potential — making DSCR loans viable even for self-employed borrowers without W-2 income.

What is the difference between a hard money loan and a DSCR loan?

Hard money loans are short-term (typically 6–24 months), asset-based, and used for acquisitions and renovations. DSCR loans are long-term rental loans underwritten on the property's rental income. Many investors use both in sequence through the BRRRR strategy — hard money to buy and renovate, then refinance into a DSCR loan once the property is stabilized.

How much down payment do you need for an investment property in 2026?

Most conventional investment property loans require 15% down for single-unit properties and 25% down for 2–4 unit properties per current Fannie Mae guidelines. Some hard money and alternative programs offer higher leverage.

Can you get real estate investment financing with bad credit or after a bank turndown?

Yes. Hard money loans are asset-based and have limited credit requirements. Private money lenders, seller financing, and financing intermediaries like Franklin Financing Services can find solutions for investors with imperfect credit, recent late payments, or prior bank rejections. Programs like the Easy Pay Cash Advance explicitly accept poor credit with no personal guarantee required.

What documents do you typically need to apply for a real estate investment loan?

It depends on the loan type:

- DSCR loans: Property income documentation and a lease or rent schedule — no personal tax returns required

- Conventional loans: Full income documentation including tax returns, W-2s, and bank statements

- Hard money loans: Property details, ARV, and exit strategy; some fast-track programs need only an application and four months of bank statements