The SBA 504 loan program addresses this gap directly. It's designed for fixed-asset financing — real estate, construction, major renovations — with long-term fixed rates and a structure that brings the required equity down to 15% for most hotel buyers. That's a meaningful difference when you're looking at a $3 million acquisition.

This article covers how the 504 program works for hotels specifically: the three-part loan structure, eligible uses, qualification requirements, what lenders actually evaluate in hotel underwriting, and how to move through the application process.

Key Takeaways

- Hotels are classified as special-purpose properties, requiring 15% down (or 20% for new businesses) rather than the standard 10%

- The 504 loan splits into three parts: ~50% from a bank, 35–40% from a CDC, and 10–20% from the borrower

- Eligible uses include acquisition, new construction, major renovations, and fixed long-life equipment

- Loan approval hinges on hotel-specific metrics like RevPAR, ADR, and DSCR, in addition to standard commercial real estate factors

- The program is for owner-operators only — passive investors do not qualify

Why SBA 504 Loans Are a Strong Fit for Hotel Financing

Hotels occupy an unusual position in commercial real estate. Because they can't easily be repurposed — a hotel building isn't readily converted to office space or retail — the SBA classifies them as Limited or Special Purpose Properties. That classification affects the equity requirement, but it doesn't disqualify hotels from the program. The 504 is well-suited to them.

Structural Advantages Over Conventional Financing

| Factor | SBA 504 | Conventional Bank Loan |

|---|---|---|

| Minimum down payment | 15% (hotel) | 25–35% |

| Amortization | Up to 25 years | Typically 15–20 years |

| Interest rate | Fixed (CDC portion) | Often variable |

| Balloon payments | None | Common |

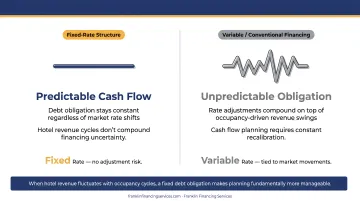

The fixed-rate structure matters more than it might seem. Hotel revenue fluctuates with occupancy cycles, and a fixed debt obligation — rather than one tied to rate adjustments — makes cash flow planning more predictable.

Who This Program Is Built For

SBA 504 financing is structured for owner-operators, not passive investors. If you're planning to run the hotel yourself, the program fits. If you're looking to acquire a property and lease operations to someone else, you're outside the program's core intent — though Eligible Passive Company structures exist for specific situations.

The 504 is a natural fit for hospitality entrepreneurs, including:

- First-time hotel buyers entering the market with limited capital reserves

- Motel operators expanding to a second property

- Experienced operators turned away by conventional lenders because their down payment didn't meet the bank's threshold

How SBA 504 Hotel Loans Are Structured

The 504 program uses a three-party financing model — knowing the split upfront lets you plan your equity contribution before you're deep into a deal.

The Three-Part Structure

According to SOP 50 10 8, the structure works as follows:

| Project Type | Bank (1st Lien) | CDC/SBA Debenture | Borrower Equity |

|---|---|---|---|

| Standard (non-special-purpose) | 50% | 40% | 10% |

| Hotel (special-purpose property) | 50% | 35% | 15% |

| New business + hotel (special-purpose) | 50% | 30% | 20% |

The bank takes the first-lien position and carries approximately half the project cost. The Certified Development Company (CDC) issues an SBA-guaranteed debenture for the middle portion. The borrower contributes the remaining equity at closing.

CDCs are SBA-regulated nonprofits that originate and service the debenture portion of 504 loans. According to NADCO, over 200 CDCs serve all 50 states, and 504 loans are available exclusively through them. Each CDC covers a specific geographic area, so the right one depends on where your property is located.

A Concrete Example

On a $3 million hotel acquisition:

- Bank loan (50%): $1,500,000

- CDC debenture (35%): $1,050,000

- Borrower equity (15%): $450,000

If the buyer is also a new business (operating under two years), the equity requirement shifts to 20%: $600,000 — and the CDC debenture drops to 30% ($900,000).

The Green 504 Option

Hotels undergoing energy upgrades may qualify for the SBA 504 Green Program. Standard CDC debentures are capped at $5 million, but qualifying energy projects can access up to $5.5 million. To qualify, the project must reduce existing building energy consumption by at least 10% or generate more than 15% of its energy from renewable sources. Evaluate this option early — it's a natural fit for any property improvement plan (PIP) that includes mechanical or energy system upgrades.

What an SBA 504 Loan Can (and Cannot) Be Used For

Eligible Uses for Hotel Projects

- Acquisition of an existing hotel, motel, or lodging property

- New construction of a hotel building on purchased land

- Major renovations and structural improvements, including parking, utilities, and landscaping upgrades

- Fixed long-term equipment — commercial laundry, HVAC systems, kitchen equipment for on-site restaurants — provided the equipment has a useful life of at least 10 years and is fixed to the location

- Soft costs directly tied to the project: appraisals, title insurance, surveys, environmental reports, and architect fees — confirm eligible items with your CDC before budgeting these in

What 504 Funds Cannot Cover

- Working capital or inventory

- Rolling stock or vehicles

- Refinancing of existing SBA or federally guaranteed debt (permitted only under narrow conditions, not as a general rule)

If you need working capital alongside your hotel acquisition, an SBA 7(a) loan is the more appropriate vehicle — and you can use both programs together to cover real estate costs and day-to-day operational needs simultaneously. Franklin Financing Services offers SBA 7(a) loans from $150,000 to $5 million with experience working specifically with hotel and motel operators — so if your project calls for both programs, that's a conversation worth having early in the process.

Who Qualifies: SBA 504 Eligibility for Hotel Buyers

Business Eligibility Criteria

To qualify under current SBA standards:

- Must be a for-profit business operating in the United States

- Tangible net worth must not exceed $20 million

- Average net income after federal taxes must not exceed $6.5 million over the prior two fiscal years

(Note: older sources cite $15M/$5M thresholds — those figures are outdated. The current SOP 50 10 8 uses the $20M/$6.5M standards.)

Owner-Occupancy Requirement

This is non-negotiable. For existing hotel buildings, the borrower must occupy and operate at least 51% of the space. For new construction, the initial occupancy requirement is 60%, with the expectation of expanding use over time.

Passive investors or holding companies that don't actively operate the hospitality business cannot qualify for a 504 loan.

Eligible Property Types

The SBA explicitly lists hotels, motels, and other lodging facilities as eligible. To qualify in this category, the business must derive more than 50% of revenue from transients staying 30 days or less. Beyond traditional hotels, the program covers:

- Motels

- Resorts (evaluated under "other lodging" criteria)

- Bed and breakfasts

Job Creation Requirements

The 504 program ties borrowing capacity to job creation. Under SOP 50 10 8, the current threshold is 1 job per $90,000 of CDC debenture. For energy public policy projects, the ratio is 1 job per $140,000. That means a project supporting 10 jobs could support up to $900,000 in CDC financing — so it's worth running this math before you lock in your deal structure.

Credit and Experience

No official SBA minimum credit score exists, but most lenders treat a score in the 680+ range as a practical floor. For hotel deals specifically, demonstrated hospitality management experience carries just as much weight. Lenders want confidence that whoever is taking on a $2–5 million property knows how to run it. First-time buyers with limited hospitality backgrounds should present a strong management team to offset that gap.

What Lenders Evaluate: Hotel-Specific Underwriting

Hotels are operating businesses, not just real estate. Lenders assess both the property and the business performance, which makes hotel underwriting more involved than a standard commercial real estate loan.

Key Performance Metrics

STR, which aggregates data from 94,000 hotels representing 12 million guest rooms, provides the benchmarking data lenders rely on most. The core metrics:

- ADR (Average Daily Rate): Room revenue divided by rooms sold

- RevPAR (Revenue Per Available Room): Occupancy rate multiplied by ADR, or total room revenue divided by available rooms

- RevPAR Index: Compares your hotel's RevPAR against its competitive set. A score of 100 means parity; above 100 means outperforming the comp set

These figures are drawn from STR reports, which your lender will use to benchmark the subject property against comparable hotels in the same market.

DSCR and Global Cash Flow

Lenders require sufficient cash flow to service the new debt. Key things lenders examine here:

- DSCR floor: No SBA-mandated minimum exists in the official SOP, but lenders typically apply their own overlays — often around 1.25x as a practical floor

- Global cash flow analysis: Accounts for all borrower obligations — personal debt, other business interests, and the proposed new debt — not just hotel operating income

- Lender overlays: The exact threshold varies by lender, so expect some variation between institutions

Feasibility Studies

For acquisitions, lenders commonly require a third-party feasibility study covering local market conditions, demand drivers, competitive supply, and the property's projected financial performance. Properties with limited operating history or those located in new or unproven markets face the most scrutiny here — a strong feasibility study can make or break the loan decision.

Steps to Apply for an SBA 504 Hotel Loan

Documentation to Prepare

- Business tax returns (2–3 years)

- Personal financial statements for all principals

- Purchase contract and property appraisal

- STR report or comparable market data

- Third-party feasibility study

- Franchise agreement (if applicable)

- Renovation or PIP cost estimates with contractor bids

- Proof of liquidity post-closing

- SBA Form 1244 (the official 504 Borrower Information Form)

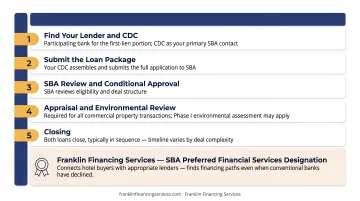

The Application Process

- Find your lender and CDC — You'll need both a participating bank for the first-lien portion and a CDC for the debenture. The CDC is your primary point of contact for the SBA-guaranteed portion.

- Submit the loan package — Your CDC will assemble and submit the full application to SBA.

- SBA review and conditional approval — The SBA reviews eligibility and the deal structure.

- Appraisal and environmental review — Required for all commercial property transactions; SBA may also require a Phase I environmental assessment.

- Closing — Both loans close, typically in sequence. Timeline varies by deal complexity; work with experienced hotel lenders to avoid unnecessary delays.

An experienced intermediary can cut through the complexity at every step above. Franklin Financing Services holds a Preferred Financial Services designation from SBA lenders, which speeds up processing and reduces back-and-forth with the SBA. They connect hotel buyers with appropriate lenders and identify financing paths even when conventional banks have declined — which happens more often in hotel deals than most borrowers expect.

Frequently Asked Questions

What is the minimum loan amount for an SBA 504 loan?

There is no official SBA minimum for the 504 program. In practice, CDCs typically work with loans starting around $250,000, though this varies by CDC. Hotel transactions almost always exceed this floor given acquisition and renovation costs.

How hard is it to get an SBA 504 loan?

For hotel buyers, approval hinges on credit history, business viability, sufficient equity injection, and demonstrated hospitality management experience. The 504 program is structured to be more accessible than conventional financing — a strong operational plan addresses most lender concerns.

What is the 20% rule for SBA?

The 20% equity injection applies when a borrower is both starting a new business (under two years old) and acquiring a special-purpose property like a hotel. This replaces the standard 15% requirement for established operators buying special-purpose properties.

What is an SBA acquisition loan?

An SBA acquisition loan uses an SBA-backed program — 504 or 7(a) — to purchase an existing business or commercial property. For hotels, this covers the real estate, existing improvements, and where applicable, business goodwill.

Can I use an SBA 504 loan to buy a motel or bed and breakfast?

Yes. Motels, resorts, and bed and breakfasts are eligible under the 504 program, provided the borrower is an owner-operator and the property meets the special-purpose property equity requirements. The business must derive more than 50% of revenue from short-term transient guests.

What is the down payment for an SBA 504 hotel loan?

Because hotels are classified as special-purpose properties, most borrowers need 15% down. New businesses purchasing a hotel must contribute 20%. The standard 10% down payment applies only to established businesses buying non-special-purpose properties.