According to the 2026 Federal Reserve Small Business Credit Survey, 22% of small business financing applicants received no funding at all. That gap is exactly where recurring revenue financing (RRF) steps in.

This guide covers what RRF is, how it works, who qualifies, what it costs, and how to use it strategically — including options for businesses that don't fit the typical SaaS mold.

Key Takeaways

- Access upfront capital based on future subscription or contract payments — no equity required

- Approval is based on revenue quality (MRR, ARR, churn rate), not hard assets or personal credit

- Funding can arrive in days, not weeks — far faster than traditional bank loans

- RRF suits any business with low-churn, contract-based recurring revenue — not just SaaS companies

What Is Recurring Revenue Financing?

Recurring revenue financing is a form of debt funding where a lender advances capital based on the strength and predictability of a business's recurring revenue streams. Repayment flows from those future payments — structured as either a percentage of monthly revenue collected or fixed periodic payments — rather than traditional loan installments.

RRF is non-dilutive. No equity changes hands, no board seats are required, and the total repayment amount is agreed upon upfront — making it a debt instrument rather than an equity arrangement.

What Counts as Recurring Revenue?

Recurring revenue is income that repeats predictably at regular intervals under a contract, subscription, or structured arrangement. This is different from "re-occurring" revenue — repeat customers who buy again without any contractual commitment.

Qualifying recurring revenue typically includes:

- SaaS subscription fees

- Membership dues (gyms, associations, professional networks)

- Maintenance and support contracts

- Legal, accounting, or consulting retainer agreements

- Licensing renewals

- Healthcare service agreements

- Managed service provider (MSP) contracts

Lenders value recurring revenue because it represents a committed, foreseeable income stream rather than one-time or irregular sales. That predictability is what makes it financeable.

MRR vs. ARR: What's the Difference?

Monthly Recurring Revenue (MRR) is the total predictable revenue a business expects to collect in a single month from active subscriptions or contracts. Annual Recurring Revenue (ARR) is the annualized version — MRR × 12 — used to gauge total contracted recurring revenue on a yearly basis.

A simple example: 500 customers paying $100/month = $50,000 MRR = $600,000 ARR.

| Metric | Use Case |

|---|---|

| MRR | Month-to-month performance tracking, shorter billing cycles |

| ARR | Annual planning, lender underwriting, multi-year contracts |

Per Chargebee, ARR should exclude one-time implementation charges, professional services fees, and non-recurring add-ons. The MRR × 12 formula works cleanly only after normalizing all contracts into comparable recurring values.

How Recurring Revenue Financing Works

A lender evaluates your recurring revenue profile and advances a lump sum, typically a multiple of MRR or a percentage of forward-looking ARR. Repayment happens as revenue flows in — the lender either pulls payments directly from subscription revenue or sets fixed monthly draws, depending on their structure.

Capchase notes that SaaS RBF funding commonly ranges from 3x to 12x MRR, with repayment structured as 5% to 15% of revenue until a pre-agreed total is repaid.

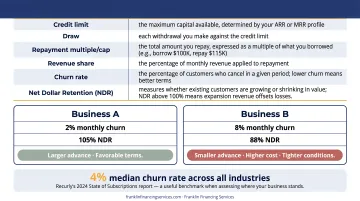

Key Terms to Understand

Before signing any RRF agreement, know what each term means:

- Credit limit — the maximum capital available, determined by your ARR or MRR profile

- Draw — each withdrawal you make against the credit limit

- Repayment multiple/cap — the total amount you repay, expressed as a multiple of what you borrowed (e.g., borrow $100K, repay $115K)

- Revenue share — the percentage of monthly revenue applied to repayment

- Churn rate — the percentage of customers who cancel in a given period; lower churn means better terms

- Net Dollar Retention (NDR) — measures whether existing customers are growing or shrinking in value; NDR above 100% means expansion revenue offsets losses

Churn directly affects both how much you can borrow and what it costs. Consider two businesses:

- Business A: 2% monthly churn, 105% NDR → qualifies for a larger advance at more favorable terms

- Business B: 8% monthly churn, 88% NDR → smaller advance, higher cost, tighter repayment conditions

Recurly's 2024 State of Subscriptions report found a 4% median churn rate across all industries — a useful benchmark when assessing where your business stands. If your churn runs above that threshold, it affects more than your growth trajectory — lenders will notice, and your agreement terms reflect it.

What Happens If a Customer Churns?

Most RRF agreements include recourse provisions. If a customer cancels mid-term:

- You can typically substitute another subscription to keep repayment on track

- If substitution isn't possible, the lender may reduce your credit limit

- In more severe cases, the lender may accelerate the balance, requiring immediate full repayment

Review these provisions carefully before drawing. Covenant-like triggers — such as revenue falling below a specified threshold — can create unexpected pressure if your business hits a rough patch.

Who Qualifies for Recurring Revenue Financing?

Eligibility benchmarks vary by lender, but common thresholds include:

- Minimum MRR: $10,000–$15,000+ (Lighter Capital requires $15K MRR; Founderpath starts at $10K MRR)

- Churn rate: Generally below 5% monthly

- Revenue history: At least 3–6 months of subscription data

- Customer concentration: No single customer should represent a disproportionate share of total revenue

- Gross margins: Many lenders look for 40%+ margins, though thresholds vary

Beyond SaaS: Who Else Can Qualify?

RRF is not exclusively for tech companies. Any business with structured, contract-based recurring revenue may qualify — including:

- Healthcare practices with service agreements or recurring billing

- Legal and accounting firms with active retainer clients

- Maintenance and repair companies with service contracts

- Managed service providers (MSPs)

- Gym and fitness studios with membership models

Across every industry, lenders are asking the same question: is your revenue committed, predictable, and unlikely to disappear suddenly? If the answer is yes, the sector you're in matters far less than you might expect.

What About Businesses Turned Down by Banks?

Because RRF underwriting relies on revenue data and contract quality — not tangible collateral, personal credit scores, or years of profitability — it opens doors for businesses that conventional lenders have already declined.

That's where Franklin Financing Services comes in. Working with national lenders, Franklin helps small and medium-sized businesses explore RRF and complementary funding structures — including businesses in healthcare, legal services, pet care, and professional services that don't fit a standard bank's criteria.

Who Is NOT a Good Fit?

- Businesses with no recurring revenue or purely transactional sales models

- Companies with monthly churn above 8–10%

- Pre-revenue businesses or those with fewer than a few months of data

- Capital-intensive operations that cannot generate predictable revenue before requiring significant upfront investment

Benefits and Risks of Recurring Revenue Financing

Benefits

- Non-dilutive — retain full ownership; no equity, no board seats

- Fast funding — some lenders deliver decisions within 24–72 hours; overall timelines often run days to a few weeks vs. months for SBA loans

- Revenue-aligned repayment — slower months mean smaller payments, reducing burden during downturns

- No hard collateral typically required — underwriting is based on revenue quality, not physical assets

For businesses that qualify, the speed advantage alone can be decisive. SBA 7(a) processing runs 5–10 business days on the lender side — and that's before closing. Lighter Capital reports its full process for new clients takes 3 to 4 weeks, while some lenders like Clearco advertise funding in as little as 24–72 hours.

Risks and Considerations

Those same features can work against you, though. RRF can become expensive capital when the structure doesn't match your growth trajectory:

- High revenue share + fast growth = shorter repayment window but a higher implicit annualized cost. The faster your revenue grows, the more you pay each month — and the effective APR can end up well above a traditional loan's stated rate

- Revenue-tied payments spike in strong months, creating unexpected cash flow pressure precisely when you might want to reinvest that capital

- Acceleration clauses — if revenue drops below a covenant threshold, the lender may demand full repayment immediately

As K&L Gates notes, the effective cost of RBF can be difficult to calculate without assumptions, since payments depend on actual revenue performance. Before signing, model the total repayment amount across multiple revenue scenarios, not just the monthly rate.

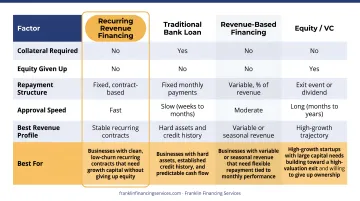

Recurring Revenue Financing vs. Other Funding Options

Not every funding option fits every business. The table below breaks down how recurring revenue financing compares to three common alternatives across the factors that matter most.

| Feature | RRF | Traditional Bank Loan | Revenue-Based Financing (RBF) | Equity/VC |

|---|---|---|---|---|

| Repayment | % of recurring revenue or fixed | Fixed monthly payments | % of all revenue monthly | No repayment required |

| Collateral | Usually not required | Often required | Usually not required | Not required |

| Dilution | None | None | None | Yes — equity given up |

| Speed | Days to weeks | Weeks to months | Days to weeks | Months |

| Best for | Low-churn subscription businesses | Businesses with hard assets and stable cash flow | High-variable-revenue businesses | High-growth, exit-oriented startups |

| Cost | Moderate to high | Lower (if approved) | Moderate to high | No repayment, but ownership cost |

When each option makes sense:

- RRF: Best for businesses with clean, low-churn recurring contracts that need growth capital without giving up equity

- Traditional bank loan: Best for businesses with hard assets, established credit history, and predictable cash flow

- RBF: Best for businesses with variable or seasonal revenue that need flexible repayment tied to monthly performance

- Equity/VC: Best for high-growth startups with large capital needs that are building toward a high-valuation exit and willing to give up ownership

How to Get Started with Recurring Revenue Financing in 2026

Step 1: Organize Your Revenue Data

Lenders need clean, verifiable data to make an offer. Before applying:

- Connect billing tools (Stripe, Chargebee) and accounting software (QuickBooks, NetSuite) to generate consistent monthly reports

- Prepare at least 2 years of monthly financial statements: balance sheet, P&L, and cash flow

- Pull a revenue-by-customer breakdown to demonstrate concentration isn't a risk

- Compile your debt schedule and any available projections

Step 2: Calculate and Benchmark Your Key Metrics

Run these numbers before approaching any lender:

- MRR = total active monthly subscription/contract revenue

- ARR = MRR × 12

- Monthly churn rate = customers lost ÷ total customers at start of period

- NDR = (starting revenue + expansion − contraction − churn) ÷ starting revenue × 100

- Gross margin = (revenue − cost of goods sold) ÷ revenue × 100

Compare your numbers against typical lender thresholds to gauge eligibility before investing time in a full application.

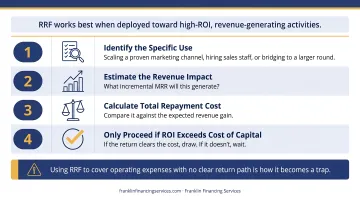

Step 3: Define Your Use of Funds Before Drawing

RRF works best when deployed toward high-ROI, revenue-generating activities. A practical test before drawing:

- Identify the specific use: scaling a proven marketing channel, hiring sales staff, or bridging to a larger round

- Estimate the revenue impact — what incremental MRR will this generate?

- Calculate total repayment cost and compare it against the expected revenue gain

- Only proceed if the ROI exceeds the cost of capital. Using RRF to cover operating expenses with no clear return path is how it becomes a trap

Step 4: Work with a Financing Specialist

Navigating RRF lenders and terms is complex, particularly for businesses in industries lenders don't typically prioritize. Franklin Financing Services works with national lenders to place qualifying businesses — across a wide range of industries — into revenue-based financing and complementary structures. They offer a free financing evaluation to identify the right fit for your situation.

Frequently Asked Questions

What is a recurring revenue loan?

A recurring revenue loan is debt financing where the lender advances capital based on a business's predictable, contract-based income — such as subscriptions or service agreements. Repayment is structured around those future payments rather than fixed bank installments — specifically designed for businesses with stable, committed revenue.

What is an example of revenue-based financing?

A B2B SaaS company with $30,000 MRR takes a $200,000 advance and agrees to repay 10% of monthly revenue until the full agreed amount is covered. In a $40,000 revenue month, they'd repay $4,000; in a $25,000 month, they'd repay $2,500 — the schedule flexes with actual performance.

Is revenue-based financing a good idea?

RBF/RRF works well for businesses with low churn, healthy margins, and a clear revenue-generating use for the capital. It gets expensive if revenue grows quickly or if terms aren't reviewed carefully. Always compare the total repayment cost against alternative options before committing.

What's the difference between MRR and ARR?

MRR measures predictable monthly subscription or contract income; ARR is simply MRR multiplied by 12. MRR is used for month-to-month operational tracking, while ARR is the figure lenders typically use for underwriting and annual planning purposes.

What types of businesses can qualify for recurring revenue financing?

While RRF is common in SaaS, any business with consistent contract-based or subscription income can potentially qualify — including healthcare practices, legal and accounting firms with retainer clients, maintenance service companies, and MSPs — as long as churn is low and revenue is predictable.

How fast can I get funded with recurring revenue financing?

Faster than most traditional options. Some lenders issue decisions within 24–72 hours, with overall timelines running days to a few weeks — compared to weeks for SBA loans or months for equity rounds.