For small and mid-sized businesses in healthcare, construction, food service, agriculture, and manufacturing, this distinction matters. It affects how much working capital you have available, how quickly you can scale, and whether you can access critical equipment without draining reserves.

This guide covers what equipment lease financing is, how it compares to loans, the step-by-step process, lease structures, what lenders evaluate, and the misconceptions that cause businesses to walk away from financing they could actually qualify for.

Key Takeaways

- Equipment lease financing provides immediate equipment access through fixed payments to a lessor who retains ownership—no large upfront purchase required

- Lease structures (FMV, $1 buyout, capital lease) differ significantly in monthly payment amounts, ownership outcomes, and tax treatment

- Lenders weigh credit history, revenue, time in business, and equipment type together — a strong application is more than just a credit score

- Businesses with prior bank rejections or imperfect credit can still qualify through specialized lenders that work outside traditional bank criteria

- Picking the wrong lease structure at the start can lock you into payments without ever gaining ownership — structure selection matters before you sign

What Is Equipment Lease Financing and Why Businesses Use It

Equipment is expensive, and tying up capital in depreciating assets limits what a business can do with its money. Equipment lease financing solves that directly.

In an equipment lease, a lessor—typically a lender or leasing company—acquires the specific equipment your business needs and rents it to you (the lessee) for a defined term at fixed monthly payments. The lessor holds legal title throughout the term. At the end, you typically choose to return the equipment, renew the lease, or purchase it at a predetermined price.

According to the Equipment Leasing & Finance Foundation's 2024 Horizon Report, the U.S. equipment finance industry reached $1.34 trillion in 2023, up 7.1% year-over-year. In that same year, 82% of businesses that acquired equipment or software used at least one financing method.

Which Industries Use Equipment Leasing Most

Virtually every equipment-intensive sector uses lease financing, but some rely on it more heavily than others:

| Industry | Why Leasing Makes Sense |

|---|---|

| Construction | Heavy equipment is capital-intensive; leasing preserves cash for payroll and materials |

| Healthcare | Imaging equipment and diagnostic devices cost hundreds of thousands; leasing avoids capital lock-up |

| Manufacturing | Production lines and machinery can be upgraded without owning obsolete assets |

| Agriculture | Seasonal revenue patterns make fixed loan payments difficult; leasing offers more flexibility |

| Food Service | Commercial kitchen equipment needs periodic upgrading as menus and volumes evolve |

| Transportation | Fleet vehicles and logistics equipment have predictable depreciation cycles |

| Technology | Hardware and systems become outdated quickly; FMV leases allow regular refreshes |

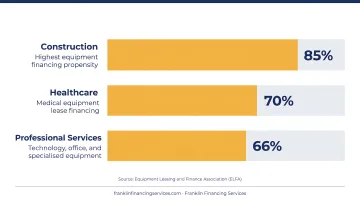

ELFA data breaks this down further: construction end users had the highest financing propensity at 85%, followed by healthcare at 70% and professional services at 66%.

Equipment Lease vs. Equipment Loan: Key Differences

| Factor | Equipment Lease | Equipment Loan |

|---|---|---|

| Ownership during term | Lessor retains title | Borrower owns the asset |

| Down payment | Often not required | Typically 10–20% |

| Monthly payments | Generally lower (especially FMV) | Higher (paying down principal) |

| End of term | Return, renew, or buy | Equipment is fully owned |

| Balance sheet | Varies by lease type (ASC 842) | Asset and liability recorded |

| Best for | Equipment that depreciates fast or needs upgrading | Equipment you intend to own long-term |

How Equipment Lease Financing Works

The process runs in three distinct stages: application, approval and structuring, and delivery with payment commencement.

Before submitting anything, have these ready:

- Equipment description plus a quote or vendor invoice

- Basic business financials or recent bank statements

- Business and personal credit information

- Intended use of the equipment

Step 1: Application and Lender Selection

You submit a lease application along with supporting documents—equipment specs, financials, and credit authorization. Lender selection at this stage shapes every term that follows.

A single bank evaluates your application against its own criteria—if you don't fit, you're declined. Businesses with prior bank turndowns, imperfect credit, or non-traditional revenue structures often have more options through a financing intermediary. Franklin Financing Services, for example, maintains relationships with multiple national lenders, giving applicants access to programs that standard bank channels simply don't offer.

Step 2: Review, Approval, and Lease Structuring

Lenders evaluate several factors during underwriting:

- Equipment value and collateral quality — New equipment with a clear invoice is easier to finance than used equipment

- Business credit and payment history — Patterns matter as much as scores

- Personal credit score — Weighted more heavily for businesses under two years old

- **Annual revenue and cash flow** — Whether your business can service the new payment obligation

- Time in business — Longer history generally means more lender options

These factors together determine your lease term, monthly payment amount, and residual or buyout value. Some alternative programs can deliver approvals within 24–48 hours, particularly for straightforward applications.

Step 3: Equipment Delivery and Lease Payments Begin

After approval, the lessor pays the equipment vendor directly. The equipment is delivered to your location, and your fixed monthly payments begin per the lease agreement.

From that point, you're typically responsible for insuring the equipment. Maintenance responsibility depends on the lease type—some structures pass that obligation to you, others include it. Read the agreement carefully before signing.

Types of Equipment Leases Explained

Equipment leases fall into two broad categories. Operating leases treat equipment use as a business expense—no ownership intent, payments expensed monthly, equipment returned at term end. Finance leases (also called capital leases) are structured for ownership transfer, with both the asset and liability appearing on your balance sheet under ASC 842.

Within those categories, three structures come up most often:

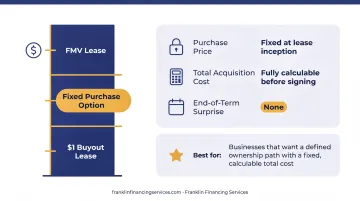

Fair Market Value (FMV) Lease

Monthly payments are lower because the lessor absorbs the residual value risk at term end. When the lease expires, you can return the equipment, renew, or purchase at current fair market value.

- Best for: Technology, software, medical imaging, or any equipment with a short useful life

- Ideal when staying current matters more than ownership — a radiology practice, for example, can upgrade to a newer MRI model at term end without the hassle of offloading outdated equipment

$1 Buyout Lease

Monthly payments run higher here — the $1 buyout price means the full equipment cost is built into the payment schedule. At term end, ownership transfers for $1.

- Best for: Businesses certain they'll keep the equipment long-term and want to claim depreciation deductions

- A printing company leasing a commercial press they plan to run for 15+ years after the lease ends is the textbook use case

Fixed Purchase Option Lease

Payments fall between FMV and $1 buyout levels. The purchase price is locked in at lease inception, so you know your total acquisition cost before signing — no surprises at term end.

- Best for: Businesses that want a defined ownership path with a fixed, calculable total cost

Equipment Finance Agreement (EFA)

The three structures above are all lease products. An EFA is different — it uses loan language ("lender" and "borrower" rather than "lessor" and "lessee") and transfers ownership to the borrower from day one.

That means you can claim Section 179 deductions or bonus depreciation immediately. The tradeoff: the asset and liability appear on your balance sheet from the start, which matters for financial reporting. EFAs work best when maximizing near-term tax deductions outweighs the balance sheet impact.

What Lenders Look at When Reviewing Your Application

The Five Core Underwriting Factors

- Business credit score and payment history — Lenders look at how consistently you've paid existing obligations

- Personal credit score — Especially influential for businesses under two years old or with limited business credit

- Time in business — Traditional banks like Bank of America require at least two years under existing ownership; alternative lenders are more flexible

- Annual revenue and cash flow — Your ability to cover the new payment is a primary concern

- Equipment type, value, and useful life — The collateral has to justify the risk

Credit Score Realities

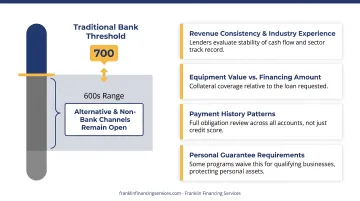

Banks typically want personal credit scores above 700 for equipment financing. Below that threshold, options narrow at traditional lenders—but they don't disappear entirely.

Alternative lenders and financing intermediaries evaluate the full picture. For businesses with scores in the 600s, recent late payments, or prior bank rejections, non-bank channels remain a viable path. Key factors these lenders weigh include:

- Revenue consistency and industry experience

- Equipment value relative to the financing amount

- Payment history patterns across all obligations

- Whether a personal guarantee is required — some programs waive this for qualifying businesses, keeping personal assets out of the equation

The Role of Equipment as Collateral

The equipment itself is a primary factor in underwriting. New equipment with a clear vendor invoice is straightforward to finance. Used equipment may require an appraisal to establish current value, and lenders check:

- Whether a secondary resale market exists if the lessee defaults

- How the equipment's useful life compares to the lease term — a 5-year lease on a 6-year asset carries more risk than the same term on a 20-year asset

- Projected residual value, which drives pricing on FMV leases

Common Misconceptions About Equipment Lease Financing

"Leasing always costs more than buying."

Total lease payments often exceed the outright purchase price. But this comparison misses the full picture. It ignores:

- The opportunity cost of tying up capital in a depreciating asset

- Tax deductibility of operating lease payments as business expenses

- The ability to upgrade equipment on a regular cycle

- Avoided ownership costs like obsolescence risk

For many businesses, leasing produces better financial outcomes than purchasing, particularly for equipment that becomes outdated within 5–7 years.

"Poor credit or a bank rejection means no equipment financing."

The 2026 Federal Reserve Small Business Credit Survey found that 22% of applicant firms received no financing from their applications. Yet online fintech lender use has grown from 17% in 2020 to 29% as businesses seek alternatives. Bank rejections are common — not disqualifying.

Alternative lenders and intermediaries like Franklin Financing Services assess the full business picture rather than filtering on credit score alone. Franklin specifically works with businesses declined by traditional banks, matching them to lender programs within a national network.

"Leasing means you'll never own the equipment."

That depends entirely on the lease structure you choose. Capital leases, $1 buyout leases, and fixed purchase option leases are explicitly designed for ownership transfer. The structure you select at signing determines the outcome. Getting that choice right before you sign is one of the most important decisions in the process.

Frequently Asked Questions

What is an equipment finance lease?

An equipment finance (capital) lease is a long-term lease structured for ownership transfer. The lessee records both the asset and liability on their balance sheet and typically purchases the equipment for a nominal amount at term end. Unlike an operating lease—where you return the equipment and no ownership transfers—a finance lease is built around eventual acquisition.

What credit score is needed for equipment financing?

Traditional banks generally look for personal credit scores above 700. Alternative lenders work with lower scores, evaluating factors like revenue and equipment value instead—so prior bank rejections or imperfect credit don't automatically disqualify you.

What types of equipment can be financed through a lease?

Most business equipment qualifies: vehicles, construction machinery, medical devices, restaurant equipment, agricultural machinery, manufacturing equipment, technology hardware, and office fixtures. Real estate and land are typically excluded from equipment financing programs.

What happens at the end of an equipment lease term?

You generally have three options: return the equipment to the lessor, renew the lease (often with updated equipment), or purchase at the agreed price—which is fair market value, a fixed predetermined amount, or $1, depending on the lease structure you chose at inception.

Is equipment lease financing tax deductible?

Operating lease payments are generally fully deductible as business operating expenses. Capital/finance leases may offer depreciation deductions instead. Because treatment varies by lease classification and business situation, consult a tax professional before finalizing your structure.

Can a startup or new business qualify for equipment lease financing?

Startups face more scrutiny since they lack business credit history. Lenders often rely more heavily on the owner's personal credit and the equipment's collateral value. Some programs do accommodate businesses under two years old, especially when equipment value is strong or the lender specializes in early-stage financing.