Commercial bridging finance exists precisely for moments like this. It provides short-term capital to close the gap between an urgent funding need and your longer-term financial solution, whether that's a property sale, a refinance, or incoming revenue.

This guide covers what commercial bridging finance is, how it works, what it costs, who it suits, and what to watch out for before you apply.

Key Takeaways

- Commercial bridge loans are short-term, asset-secured financing — not a permanent solution

- Lenders focus primarily on collateral value and exit strategy, not just credit score

- Loan-to-value ratios typically reach up to 75%, with pricing tied to variable (floating) interest rates

- Uses extend beyond property — business acquisitions and short-term cash flow gaps also qualify

- A clear, credible repayment plan is required for approval

What Is Commercial Bridging Finance?

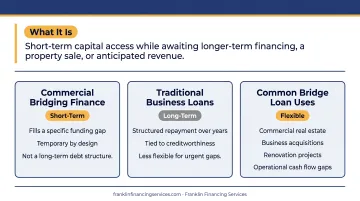

Commercial bridging finance is a short-term lending product that gives businesses immediate access to capital while they wait for longer-term financing, a property sale, or anticipated revenue to arrive. It's designed to be temporary — filling a specific funding gap rather than serving as a long-term debt structure.

Bridge loans work differently from traditional business loans in several important ways:

| Feature | Bridge Loan | Traditional Business Loan |

|---|---|---|

| Term length | Months to ~3 years | 5–25 years |

| Interest structure | Floating (SOFR-based), interest-only | Fixed or variable, principal + interest |

| Funding speed | Days to weeks | Months |

| Collateral required | Usually yes (property or assets) | Varies |

| Primary underwriting focus | Asset value + exit strategy | Credit score + cash flow history |

While commercial real estate is the most common use case, bridge loans also fund business acquisitions, renovation projects, and operational cash flow gaps. That makes them relevant across a much wider range of business situations than property development alone.

How Does a Commercial Bridge Loan Work?

A lender advances short-term capital secured against an existing or incoming asset (typically commercial property). The borrower uses those funds to complete a transaction, then repays the loan once the property sells, longer-term financing closes, or anticipated revenue arrives.

Several structural elements shape how a bridge loan is priced and approved. Understanding each one helps you anticipate what lenders will ask for — and why.

The Exit Strategy Requirement

Before approving any bridge loan, lenders require borrowers to demonstrate a clear, credible repayment plan. This is called the exit strategy, and it's the single most important factor in the approval decision.

The two most common exit types:

- Property sale: the loan is repaid from proceeds when the asset sells

- Refinancing: the borrower transitions into a long-term commercial mortgage or business loan once the property stabilizes or qualifies

As the OCC notes, refinance risk — the possibility that a borrower cannot replace existing debt under reasonable terms — is a key risk lenders assess during underwriting.

Loan-to-Value (LTV) Ratios

Lenders calculate the loan amount as a percentage of the collateral's appraised value. Based on lender program data:

- Core assets: up to 75% LTV/LTC

- Non-core or riskier assets: closer to 65% LTC

A lower LTV works in your favor. More equity in the collateral means less risk for the lender, which translates to better rates and terms.

Open vs. Closed Bridge Loans

Closed bridge loans have a fixed repayment date tied to a confirmed event, such as exchanged contracts on a property sale or a mortgage approval already in progress. Because the lender's risk is lower, rates tend to be more favorable.

Open bridge loans carry no fixed repayment date, offering flexibility when the exit timeline isn't yet confirmed. That flexibility comes at a cost: lenders charge higher rates to compensate for the uncertainty. Think of it as paying a premium for breathing room.

First Charge vs. Second Charge

First charge (first lien) loans give the lender primary claim over the collateral if the borrower defaults. Lower risk for the lender means lower rates for the borrower.

Second charge (second lien) loans sit behind an existing mortgage or first lien. The lender takes on more risk and prices accordingly. Expect noticeably higher rates on any second-position bridge loan, so factor that into your cost projections before committing.

Common Uses for Commercial Bridging Finance

Commercial bridge loans cover more ground than property purchases alone — here's where businesses actually use them.

Commercial Property Purchase

Speed is often the deciding factor in competitive property markets. Bridge loans let buyers close quickly when a seller demands a fast timeline, when a deal is at risk of collapsing, or when a buyer needs to secure a new location before their existing premises sell. J.P. Morgan notes that bridge loans provide "certainty of execution" in competitive acquisition markets where agency financing timelines are simply too tight.

Property Development and Renovation

Developers and business owners use bridge loans to fund construction, renovation, or repositioning of commercial properties while waiting on planning approvals, permanent development financing, or sale proceeds. Repayment typically comes from the completed project's sale or a long-term refinance.

Business Acquisition

When a deal needs to close before permanent financing is ready, a bridge loan locks in the acquisition while the longer-term funding catches up. Most sellers set firm closing deadlines, and a bridge loan keeps the deal on track while conventional financing is still being arranged.

Operational Cash Flow Gaps

This use case gets less attention but is entirely legitimate. Bridge financing can cover:

- Payroll during a slow revenue period

- Inventory restocking ahead of a peak season

- Costs while waiting on an insurance claim to settle

- The gap between invoicing clients and receiving payment

The Federal Reserve's Small Business Credit Survey found that 56% of firms seeking financing did so for operating expenses — a reminder that cash flow timing is a real and common challenge for small businesses.

Franklin Financing Services helps businesses across these use cases secure bridge financing, including businesses that have been turned down by traditional banks or need faster approvals than conventional lenders can offer.

How Much Does Commercial Bridging Finance Cost?

Bridge loans cost more than conventional financing. Knowing the full cost structure before you commit can save you from expensive surprises.

Interest Rates

US commercial bridge loans are typically priced as floating rates tied to SOFR (Secured Overnight Financing Rate). As a representative market example, a typical commercial bridge loan is priced at 1-Month Term SOFR + 4.50%–7.00%, reflecting the risk-based nature of the product.

Factors that affect your rate:

- Loan-to-value ratio (lower LTV = better rate)

- Asset type and quality

- Strength of the exit strategy

- Borrower and guarantor financial profile

Interest Payment Structures

Most commercial bridge loans are interest-only during the loan term, with the principal repaid at maturity. Payment structures generally include:

- Monthly payments — interest paid each month as you go

- Rolled-up interest — all interest added to the loan balance and paid in full at the end of the term (useful for cash flow during the loan period)

- Retained interest — estimated interest is deducted from the loan proceeds upfront; you receive the net amount

Fees to Expect

Based on published lender data, typical commercial bridge loan fees include:

- Origination fee: around 1.00% of the loan amount (some lenders charge more)

- Exit fee: 0.25% or more at loan payoff

- Extension fee: 0.25% or more if the loan term needs to be extended

- Appraisal and legal fees: vary by transaction; always request an itemized list

How LTV Affects Your Total Cost

Suppose you need a $1 million bridge loan against a property valued at $1.5 million. That's a 67% LTV — within lender comfort zones for most commercial bridge products.

Shift that same loan to a property valued at $1.2 million and you're looking at 83% LTV. At that level, lenders will either decline the request outright or price the loan significantly higher to offset their increased risk.

Before signing anything, add all fees to the total interest across the full loan term — the quoted rate alone won't reflect your true cost. Comparing at least two or three lenders gives you a clearer picture and meaningful negotiating leverage.

Pros, Cons, and Risks of Commercial Bridge Loans

Advantages

- Speed: Funding can happen in days to weeks rather than months

- Flexibility: Open or closed structures accommodate different exit timelines

- Opportunity access: Lets businesses act on time-sensitive deals that would otherwise be missed

- Broader qualification: Asset value and exit strategy matter more than credit score alone

- Deferred repayment options: Rolled-up interest structures preserve cash flow during the loan term

Disadvantages and Risks

- Higher cost: Rates and fees exceed conventional commercial loans — often by 3–6 percentage points or more

- Collateral at risk: If repayment fails, the lender can pursue the secured asset

- Dual debt exposure: If an existing mortgage is already in place, you may be managing two debt obligations simultaneously

- Market risk: Property values can fall, sales can take longer than planned, or refinancing conditions can tighten — all of which could leave you unable to exit on schedule

That market risk isn't theoretical. The 2023 Federal Reserve interagency policy statement specifically flags the risk that borrowers with maturing CRE loans can face difficulty obtaining credit during downturns, particularly when collateral values decline or rental absorption is prolonged (meaning vacant space takes longer than expected to lease up). Plan your exit strategy with a buffer — assume the deal takes longer than projected.

How to Apply for a Commercial Bridge Loan

What Lenders Evaluate

Lenders assess several factors during underwriting:

- Collateral value and quality — the asset securing the loan

- Exit strategy strength — how realistic and documented the repayment plan is

- Borrower and guarantor financials — cash flow, liquidity, existing obligations

- Project feasibility — for development deals, whether the business plan holds up

- Global debt service — total debt obligations relative to income across the borrower's profile

Lenders prioritize asset value and exit strategy over credit score more heavily than traditional banks do — which is why bridge loans remain accessible to borrowers who have been turned down elsewhere.

Typical Documentation Required

- Property appraisals or asset valuations

- Business financial statements (income, cash flow, balance sheet)

- Clear description of how the funds will be used

- Evidence of the exit strategy (purchase contract, mortgage approval in process, etc.)

- Business and/or personal credit history

Working with Franklin Financing Services

Gathering that documentation is straightforward when you know what lenders need — but matching it to the right loan product is where an experienced intermediary makes a real difference. Franklin Financing Services offers commercial bridge loans as part of a financing portfolio spanning 16+ product categories. As an intermediary with relationships across national lenders, they can often find solutions for businesses traditional banks have turned away — including those with prior bank rejections or credit challenges.

Their designation as a Preferred Financial Services company by SBA lenders accelerates SBA 7(a) loan processing specifically. Beyond that, their certified financial professionals can evaluate whether a bridge loan or an alternative product better fits your situation — whether that means equipment financing, accounts receivable financing, unsecured business loans, or revenue-based programs.

A free consultation gives you a clear read on which financing structure fits your timeline and exit strategy — before you commit to anything.

Frequently Asked Questions

How does commercial bridging finance work?

A lender provides short-term capital secured against an asset — usually commercial property. The borrower uses the funds for an immediate need and repays through a planned exit strategy, such as a property sale or refinancing into a long-term loan, typically within a term of up to three years.

How much does commercial bridging finance cost?

Bridge loan rates typically run 1%–3% per month, with annualized costs often ranging from 10%–24% depending on the lender and deal. Origination fees generally start around 1%, with possible exit and extension fees on top. Always request a full cost breakdown before committing.

What can commercial bridge loans be used for?

The main uses are commercial property purchase or development, business acquisitions, and operational needs like cash flow gaps, inventory restocking, or covering expenses while waiting on longer-term financing to close.

How do I qualify for a commercial bridge loan?

Lenders primarily evaluate collateral value, exit strategy viability, and overall borrower financials. Unlike traditional banks, many bridge lenders can work with borrowers who have imperfect credit or prior financing rejections, as long as the asset and repayment plan are sound.

What is the difference between an open and closed bridge loan?

A closed bridge loan has a fixed repayment date tied to a confirmed event (like exchanged contracts) and typically carries lower rates. An open bridge loan has no fixed repayment date — useful when the exit timeline is uncertain — but costs more due to the added uncertainty for the lender.

Is commercial bridging finance right for my small business?

Bridge loans work best when you have a clear, time-sensitive need and a credible repayment plan. If you're unsure, the team at Franklin Financing Services can help determine whether a bridge loan or an alternative — such as an SBA loan, term loan, or accounts receivable financing — is the right fit.