Service businesses, restaurants, healthcare practices, and other asset-light operations generate consistent revenue without accumulating significant physical assets. Traditional secured lending was never designed for them. Unsecured business loans fill that gap.

The problem is that while these products are increasingly accessible, most business owners don't fully understand how repayment works, what "flexibility" actually means in practice, or how lenders evaluate risk when no collateral is involved. That confusion leads to poor product selection — or missed funding opportunities entirely.

This guide breaks down how unsecured business loans work from application to repayment, covering the key repayment structures, flexibility mechanisms, and what it takes to qualify.

Key Takeaways

- Unsecured loans require no collateral; approval is based on creditworthiness, revenue history, and cash flow consistency

- Repayment structures differ significantly by product: fixed installments, daily/weekly ACH deductions, or a percentage of sales

- Approvals arrive within 24–48 hours; funding follows in as little as 3–7 days

- Prior bank rejections don't disqualify a business — alternative lenders evaluate cash flow and revenue, not just credit scores

- Revenue-tied repayment and no prepayment penalties make unsecured loans a stronger fit than traditional bank products for many businesses

What Are Unsecured Business Loans?

An unsecured business loan is financing issued without a specific asset pledged as collateral. Approval is based on the borrower's financial profile — credit history, cash flow, and revenue — rather than the value of property or equipment.

The SBA defines unsecured business funding as financing based on the business owner's creditworthiness, with no requirement to pledge real estate, inventory, or equipment.

What "Unsecured" Doesn't Mean

Unsecured does not mean no recourse. Lenders still protect themselves — just through different mechanisms:

- Personal guarantees — a legal commitment by the owner to repay if the business cannot

- Revenue pledges — lender rights to future receivables

- Blanket UCC liens — a public filing giving the lender a security interest in general business assets

According to Federal Reserve research, 65% of nonemployer firms used a personal guarantee or collateral to secure financing. Unsecured refers to the absence of a specific pledged asset — not a lender walking away empty-handed if repayment fails.

Primary Unsecured Loan Types

| Product | Repayment Structure |

|---|---|

| Working capital / term loans | Fixed daily, weekly, or monthly installments |

| Business lines of credit | Revolving; repay only what you draw |

| Merchant cash advances (MCAs) | Percentage of card sales withheld from batches |

| Revenue-based financing | Percentage of total monthly revenue |

| SBA micro-loan programs | Fixed installments; varies by program |

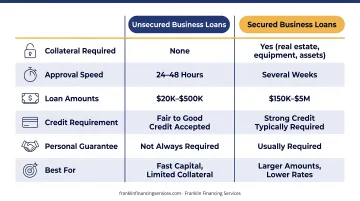

Unsecured vs. Secured: A Quick Comparison

| Factor | Unsecured | Secured |

|---|---|---|

| Approval speed | Days | Weeks |

| Asset risk | No specific asset at risk | Pledged asset can be seized |

| Credit requirements | More flexible | Generally stricter |

| Typical loan amounts | Varies widely | Often higher ceiling |

How Unsecured Business Loans Work

Unsecured business loans move through a defined sequence: application, underwriting, approval, funding, and repayment. Understanding each stage helps avoid surprises.

Application and Underwriting

The application process is leaner than secured lending. No asset appraisals or title searches are required. Typical requirements include:

- 3–6 months of business bank statements

- Basic business information (entity type, industry, time in business)

- Credit authorization (often a soft pull that doesn't affect your score)

Without collateral to fall back on, lenders underwrite based on data. The FDIC and federal banking agencies recognize cash-flow data as a legitimate alternative underwriting input. In practice, lenders analyze:

- Average monthly deposit balances and deposit frequency

- Overdraft and NSF history

- Monthly revenue consistency

- Personal and business credit scores

- Time in business

Franklin Financing Services' FAST TRACK Loan Program illustrates this well — requiring only an application and the last four months of bank statements, with approval decisions returned in 24–48 hours.

Approval and Funding

Once approved, you receive a loan agreement detailing the loan amount, repayment term, payment frequency, and cost. For term loans, lenders express cost as an APR; for MCAs, they use a factor rate. Once you sign, disbursement follows based on the product type:

- Term loans and MCAs: Lump-sum direct deposit

- Lines of credit: Access to a revolving credit limit, drawn as needed

Funding typically occurs within 3–7 days for businesses working with alternative lenders — a meaningful advantage over traditional secured bank loans, where long approval timelines are a common friction point with traditional banks.

Repayment in Motion

Most lenders collect repayments through automated ACH debits on a set schedule — daily, weekly, or monthly. MCAs work differently: repayment is a fixed percentage withheld from credit card processing batches.

Consistent on-time repayment builds business credit history over time, which can translate into larger amounts and better terms on future financing.

Repayment Terms Across Unsecured Loan Types

"Repayment terms" means something different depending on the product. Structure, frequency, duration, and cost all vary in meaningful ways across unsecured loan types — and matching the wrong product to your cash flow pattern creates real strain, even with strong revenue. Here's how each structure works.

Working Capital / Term Loans

Fixed daily, weekly, or monthly installments over a defined term. The Federal Reserve's review of online lenders found advertised terms ranging from 3 months to 5 years, with payment frequencies spanning daily to monthly.

Franklin Financing Services' standard Business Term Loans run $20,000–$500,000 with 1–4 year repayment terms. Predictable payments make budgeting straightforward — and many lenders offer no prepayment penalty, so a strong revenue month can translate into early payoff and reduced total cost.

Business Lines of Credit

Revolving structure with no fixed repayment schedule per draw. Key mechanics:

- Borrow only what you need, repay only what you've drawn

- Interest accrues on the outstanding balance only

- Available credit replenishes as principal is repaid

Best suited for ongoing or unpredictable cash flow needs — covering a payroll gap one month, restocking inventory the next.

Merchant Cash Advances (MCAs)

Repayment comes from a fixed percentage of daily credit and debit card sales, withheld from processing batches until the advance is fully repaid. Lenders express this cost as a factor rate, not an APR.

Key cost benchmarks from the Federal Reserve's review of online lender websites:

- Factor rates typically range from 1.14 to 1.48

- The FTC notes MCA factors often represent 20% to 50% of the advance amount

- Repayment timeline fluctuates with sales volume — faster in strong periods, slower during downturns

Franklin Financing Services' Easy Pay Cash Advance advances 80–120% of average monthly credit card receipts, up to $150,000. Businesses with at least $8,000 in monthly card sales can qualify, with repayment set at 15–20% of future card receipts.

Revenue-Based Financing

Repaid as a percentage of total monthly revenue rather than card sales specifically. Payments rise in strong months and fall in slow ones — a natural fit for seasonal businesses such as restaurants, retailers, and farms.

Franklin Financing Services offers revenue-based financing from $50,000 to $1,000,000, with repayment typically set at 3–9% of monthly cash receipts over 2–5 year terms. The program is specifically designed to serve women-owned, veteran-owned, minority-owned, and LGBTQ+-owned businesses — as well as companies operating in low-to-moderate income areas.

Choosing the Right Structure

| Business Type | Best-Fit Product |

|---|---|

| Stable, predictable revenue | Fixed-installment term loan |

| High card transaction volume | MCA |

| Seasonal or variable income | Revenue-based financing |

| Ongoing, unpredictable needs | Line of credit |

Flexibility Features That Set Unsecured Loans Apart

Revenue-Tied Repayment

MCAs and revenue-based financing adjust automatically to what a business actually earns. A fixed bank loan demands the same payment regardless of whether last month was your best or worst. Revenue-tied products scale with what you bring in, which matters most when cash flow tightens.

The FTC confirms that MCA daily payments rise or fall based on daily card receipts. California's DFPI defines sales-based financing specifically as repayment based on a percentage of sales or revenue. That variability is structural — written directly into how the repayment formula works.

Prepayment Flexibility

Many unsecured term loans and lines of credit carry no prepayment penalty. If you have a strong revenue month, you can pay down principal early and reduce your total interest cost.

By contrast, the SBA notes that SBA 7(a) loans with maturities of 15 years or longer carry prepayment penalties when borrowers voluntarily prepay 25% or more of the outstanding balance in the first three years. Some alternative lenders go further, advertising interest discounts for loans repaid within 90–100 days.

Speed as Functional Flexibility

Prepayment terms help when business is good — but speed determines whether you can act at all. Funding in 3–7 days means unsecured loans can respond to real-time needs:

- Purchasing inventory before a peak season

- Covering a short-term payroll gap

- Acting on a sudden expansion or acquisition opportunity

A traditional secured loan's multi-week timeline makes these scenarios impractical. By the time approval comes through, the inventory is gone or the opportunity has moved on.

Who Qualifies: How Lenders Assess Risk Without Collateral

Without collateral, lenders rely on four core pillars to evaluate applicants:

- Personal and business credit score — The Federal Reserve categorizes applicants with FICO scores of 720+ as low credit risk; 719 and below as medium/high risk

- Time in business — Generally 6–12 months minimum, though programs vary

- Monthly and annual revenue consistency — Lenders look for stable deposit patterns, not just revenue totals

- Cash flow health — Average daily bank balance, deposit frequency, and absence of NSF events

A strong profile across all four typically results in larger amounts and better terms.

General Qualification Benchmarks

These thresholds vary by lender and product — but as a practical reference:

- Personal FICO score: 600 or higher (some programs more flexible)

- Time in business: At least 6–12 months

- Monthly revenue: Roughly $10,000 or more, consistent

The Federal Reserve found that approval rates at online lenders reached 82%, compared to 71% at small banks and 58% at large banks — reflecting the broader eligibility range alternative lenders typically work with.

What About Poor Credit or Prior Bank Rejections?

Bank rejections don't disqualify a business from unsecured financing. Alternative lenders weigh cash flow, revenue history, and processing volume — not just a credit score.

Franklin Financing Services works with businesses across a wide range of credit profiles — including those with poor credit, late payments, or prior bank turndowns. The Easy Pay Cash Advance program qualifies applicants based on credit card processing volume alone. Requirements include:

- No financials

- No tax returns

- No asset documentation

- No personal guarantee

That shift is broader than one company. The 2024 Small Business Credit Survey found 29% of applicants turned to online fintech lenders — showing how many businesses now look beyond traditional banks when conventional financing falls through.

Frequently Asked Questions

What are the repayment terms and how flexible are no-collateral loans?

Repayment terms vary by product: fixed daily, weekly, or monthly installments for term loans (typically 6 months to 5 years), revolving repayment for lines of credit, and sales-percentage-based repayment for MCAs and revenue-based financing. Both adjust automatically with business performance, so payments flex with your revenue without renegotiating terms.

What is the main advantage of non-recourse loans compared with unsecured loans?

Non-recourse loans limit lender recovery to the specific collateral pledged, protecting the borrower's other assets even in default. Unsecured loans carry no collateral requirement at all, but typically include a personal guarantee — meaning the borrower remains personally liable. Choose non-recourse if protecting specific assets is the priority; choose unsecured if you want to avoid pledging collateral altogether.

Can I get an unsecured business loan if I've been turned down by a bank?

Bank rejections do not disqualify a business from unsecured financing. Alternative lenders evaluate cash flow and revenue rather than relying solely on credit score, and many businesses that fail to meet bank standards qualify through non-bank financing partners like Franklin Financing Services.

Do unsecured business loans require a personal guarantee?

Most do — a personal guarantee is a legal commitment by the owner to repay if the business cannot. However, some programs explicitly waive this requirement. Franklin Financing Services' Easy Pay Cash Advance, for example, requires no personal guarantee and no financial documentation.

How quickly can I get funded with an unsecured business loan?

Most unsecured business loans can be approved within 24–48 hours and funded within 3–7 days, since no asset appraisal is required. Franklin Financing Services' FAST TRACK Loan Program and Easy Pay Cash Advance both fall within this timeline — often weeks faster than traditional secured bank financing.

What is the difference between a merchant cash advance and an unsecured business term loan?

A term loan provides a lump sum repaid in fixed installments at a set APR over a defined period — straightforward and predictable. An MCA provides a lump sum repaid as a percentage of daily card sales at a factor rate, making payments flexible but the total cost potentially higher. Businesses with steady monthly revenue typically benefit more from a term loan; those with variable daily card sales often find an MCA easier to manage.