Introduction

Bidding wars regularly push existing rental properties above the price point where the numbers work. When available inventory can't hit your return threshold, building from scratch is a practical alternative — you control the specs, the layout, and the cost basis.

But financing a ground-up build on an investment property works very differently from buying an existing rental. You're not applying for a standard mortgage. You're applying for a specialized, short-term product with its own draw mechanics, qualification standards, and cost structure.

This guide covers what construction loans are, how draws and interest payments work, what lenders require, and how to move from planning through permanent financing.

Key Takeaways:

- Construction loans disburse funds in stages tied to verified milestones — not as a lump sum at closing

- Interest-only payments are calculated on the drawn balance, keeping early carrying costs manageable

- Private lenders approve faster and accept more flexible credit profiles than banks — at higher rates

- Down payments for investment property construction typically run 20–30% for conventional lenders

- Budget a 10–20% contingency buffer — cost overruns typically come out of pocket

What Is a Construction Loan for an Investment Property?

A construction loan for an investment property is a short-term financing product used to fund the ground-up building of a property intended for rental income or resale — not a primary residence. That distinction matters for underwriting. The OCC defines investor-owned residential real estate as 1–4 family properties where rental income is the primary repayment source, which sets the regulatory boundary for this product category.

What Properties Qualify

According to The Federal Savings Bank, investment construction loans can finance:

- Single-family rentals

- Duplexes

- Triplexes

- Fourplexes

Properties with five or more units cross into commercial multifamily territory, which carries different underwriting criteria and typically requires separate commercial construction financing. That unit-count boundary also signals a broader structural difference between this product and a standard mortgage.

How This Differs from a Standard Mortgage

A traditional mortgage delivers the full loan amount at closing because the property already exists. A construction loan doesn't work that way. Funds are disbursed in stages — called draws — as construction milestones are completed and verified. The lender isn't financing a finished asset; it's financing a build-in-progress, which is why qualification requirements, disbursement rules, and costs are structured so differently.

How Construction Loans for Investment Properties Work

The Draw Process

Lenders release funds in stages tied to verified construction milestones. Common checkpoints include:

- Foundation pour

- Framing

- Mechanical, electrical, and plumbing rough-in

- Drywall

- Final completion

Each draw requires a lender inspection confirming that the work is complete before the next tranche is released.

The OCC treats this staged disbursement process as a core risk control — not administrative overhead. Weak progress monitoring and poor disbursement controls increase lender credit risk, which is why inspections are non-negotiable regardless of the lender type.

Interest-Only Payments During Construction

You pay interest only on funds already disbursed, not on the full loan commitment. On a $300,000 construction loan at 10%, your monthly payment when $150,000 has been drawn is $1,250 — not the $2,500 you'd owe if interest were calculated on the full balance. As draws accumulate, payments increase, but the structure cuts carrying costs in the early build phases.

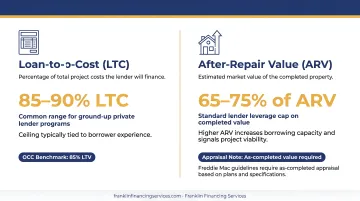

Loan Sizing: LTC and ARV

Two metrics drive how lenders size investment construction loans:

- Loan-to-Cost (LTC): The percentage of total project costs the lender will finance. Many private lenders offer ground-up programs at 85–90% LTC, with the ceiling typically tied to borrower experience.

- After-Repair Value (ARV): The estimated market value of the completed property. Most lenders cap leverage at 65–75% of ARV. The OCC's supervisory benchmark for 1–4 family residential construction sits at 85% LTV as a regulatory ceiling.

A higher ARV increases borrowing capacity and signals that the project is viable. Lenders will order an "as-completed" appraisal before funding — Freddie Mac's guidelines require that appraisals include an as-completed value based on the plans and specifications.

Construction Term Length

Most investment construction loans run 12–24 months. After construction is complete, the loan either converts to a permanent mortgage or is paid off through a refinance — often into a DSCR rental loan once the property is leased and generating income. Understanding your exit strategy before breaking ground is just as important as securing the construction funding itself.

Types of Construction Loans Available to Investors

Construction-to-Permanent Loan

This structure combines the build phase and the permanent mortgage into a single financing package. The loan starts as short-term construction financing and automatically converts to a long-term mortgage once the build is complete, eliminating a second application and closing. Fannie Mae supports both single-closing and two-closing variations of this structure.

Conventional banks primarily offer this product, but it comes with tighter credit requirements and longer approval timelines.

Stand-Alone (Construction-Only) Loan

A stand-alone construction loan covers only the building phase. Once construction is complete, the borrower separately refinances into a permanent mortgage — requiring two closings and two approval processes. The tradeoff is flexibility: you're not locked into one lender's permanent mortgage terms at the outset.

The Federal Savings Bank notes that ground-up rental financing most commonly uses this two-close structure, with investors refinancing into a long-term mortgage after completion.

Hard Money / Private Construction Loans

Private and hard money lenders offer construction loans with faster approvals and more flexible qualification standards — making them a realistic option when timelines are tight or project type doesn't fit a bank's criteria.

As a benchmark, Stormfield Capital's non-owner-occupied residential construction program illustrates typical private lender terms:

- Closes in 2–3 weeks

- 12–18 month terms with interest-only payments

- 70% ARV cap

- Sample rate of 10.99% with a 2.00% origination fee

For investors who've been turned down by traditional banks — due to credit history, project type, or timeline — private lenders are often the practical path. Franklin Financing Services maintains relationships with national lenders and helps real estate investors find construction financing solutions even after conventional bank turndowns.

Qualifying for a Construction Loan: Requirements and Costs

Credit Score and Financial Profile

Requirements vary considerably between lender types:

- Conventional banks: Texas Gulf Bank lists a 680 minimum credit score, with 720 as the ideal threshold

- Private lenders: RCN Capital's non-owner-occupied ground-up program lists a 650 minimum FICO

- Debt-to-income ratio and existing financial obligations are evaluated alongside credit scores — lenders are assessing whether the project's economics can support repayment

Down Payment Requirements

Non-owner-occupied construction loans require more equity than primary residence builds because repayment depends on the investment property's economics rather than owner occupancy.

- Conventional lenders: Texas Gulf Bank states down payments generally range 20–30% of total construction costs

- Private lenders: The Federal Savings Bank notes ground-up rental loans may require 10–25% down depending on the project and borrower profile

Those equity thresholds reflect what you'll need on paper — but lenders also scrutinize the documentation behind the build before approving anything.

Documentation Requirements

Beyond financial statements, lenders require:

- Detailed construction plans and blueprints

- Line-item project budget with contingency reserves

- Proposed build timeline

- Licensed contractor credentials and proof of insurance

- Permits (or evidence that permit applications are in process)

- Land ownership documentation or purchase agreement

Self-performing work is generally prohibited: most lenders require a licensed general contractor, and many will require builder approval before issuing the loan.

Once you understand what's needed to qualify, the next step is sizing up what the loan will actually cost you.

The Full Cost Picture

Private lender benchmarks from published programs:

| Cost Item | Typical Range |

|---|---|

| Interest rate (private) | 9.84%–10.99%+ |

| Origination fee | 1–2% of loan amount |

| Underwriting fee | ~$1,500 |

| Draw inspection fee | ~$300 per draw |

| Feasibility/contractor report | $650–$1,200 |

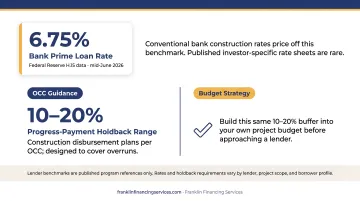

The bank prime loan rate stood at 6.75% as of mid-June 2026 per Federal Reserve H.15 data. Conventional bank construction rates price off that benchmark, though published investor-specific rate sheets are rare.

Budget for contingency before you approach a lender. The OCC describes progress-payment holdbacks of 10–20% in construction disbursement plans to help cover overruns, and that same buffer should exist in your own project budget.

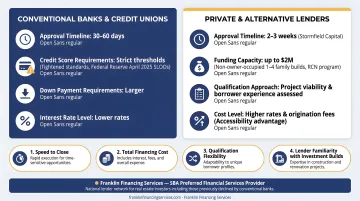

Traditional Banks vs. Alternative Lenders: Where to Get Financed

Conventional banks and credit unions typically offer lower rates for investor construction loans, but they apply strict credit score thresholds, require larger down payments, and run approval timelines of 30–60 days from application to final approval. The Federal Reserve's April 2025 Senior Loan Officer Opinion Survey reported that banks continued tightening standards for construction and land development loans — meaning the bar hasn't gotten lower.

Private lenders operate differently. Stormfield Capital closes in 2–3 weeks. RCN's program funds up to $2M for non-owner-occupied 1–4 family builds. The tradeoff is cost — private programs run higher on rates and origination fees. That gap matters, but it's rarely the only factor worth measuring.

When evaluating which path fits your project, weigh these four factors:

- How quickly you need to close — private lenders consistently outpace banks on timeline

- Total financing cost — bank rates are lower but harder to qualify for; private rates are higher but more accessible

- Qualification flexibility — private lenders assess project viability and borrower experience, not just credit thresholds

- Lender familiarity with investment builds — someone who understands draw management and investor exit strategies makes the higher cost worthwhile

Franklin Financing Services, an SBA-designated Preferred Financial Services provider, works with a national lender network specifically to help real estate investors access construction financing — including those previously turned down by conventional banks. That network access is particularly useful when a project doesn't fit standard bank underwriting but still carries strong fundamentals.

Step-by-Step: How to Apply for a Construction Loan on an Investment Property

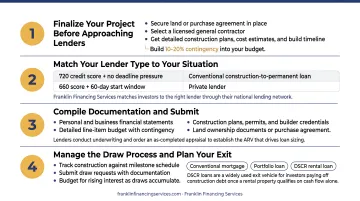

Step 1: Finalize your project before approaching lenders

Secure the land or have a purchase agreement in place. Select a licensed general contractor. Get detailed construction plans, cost estimates, and a build timeline. Build 10–20% contingency into your budget. Lenders won't take an application seriously without this foundation in place.

Step 2: Match your lender type to your situation

Assess your credit score, timeline, and project scope honestly. A 720 credit score and no deadline pressure points toward a conventional construction-to-permanent loan. A 660 score and a 60-day construction start window points toward a private lender. Franklin Financing Services works with investors to match the right lender to each scenario through their national lending network.

Step 3: Compile documentation and submit

Gather all required materials:

- Personal and business financial statements

- Construction plans, permits, and builder credentials

- Detailed line-item budget with contingency

- Land ownership documents or purchase agreement

Lenders will conduct underwriting and order an as-completed appraisal to establish the ARV that drives loan sizing.

Step 4: Manage the draw process and plan your exit

After funding, track construction against your milestone schedule. Submit draw requests with required documentation and schedule inspections promptly to avoid delays. Budget for rising interest payments as draws accumulate.

Start planning your permanent financing exit before construction wraps. Common options include:

- Conventional mortgage — if the property will be owner-occupied or meets standard qualification criteria

- Portfolio loan — for investors who don't fit agency guidelines

- DSCR rental loan — once the property is leased and rental income is documentable

According to OfferMarket, DSCR loans are a widely used exit vehicle for investors paying off construction debt once a rental property qualifies on cash flow alone.

Frequently Asked Questions

Can real estate investors get construction loans for investment properties?

Yes. Conventional banks offer investor construction loans but apply strict credit, documentation, and equity requirements. Private lenders and financing partners like Franklin Financing Services offer more accessible alternatives for investors with non-traditional credit profiles or project types.

What would the monthly payment be on a $300,000 construction loan for an investment property?

Payments during construction are interest-only on the drawn balance — not the full commitment. At 10% interest with $150,000 drawn, your monthly payment is approximately $1,250. At full draw ($300,000), that rises to $2,500. Actual payments depend on the rate, drawn balance, and lender terms.

How hard is it for a real estate investor to get a $1,000,000 construction loan?

Large construction loans require strong financial documentation, meaningful equity, and a credible build plan. Conventional banks apply very strict standards at this size, but private lenders can go up to $2M or more on non-owner-occupied residential builds. Financing partners with national lender access can find solutions for qualified investors who don't fit the traditional bank profile.

What is the difference between a construction loan and a fix-and-flip loan?

A construction loan finances building a new property from the ground up. A fix-and-flip loan finances the purchase and renovation of an existing structure. They differ in draw mechanics, term lengths, and underwriting — one starts with land, the other with an existing asset.

Can I use a construction loan to build a multifamily investment property?

Yes, for small multifamily. Duplexes, triplexes, and fourplexes qualify under standard 1–4 family residential construction loan programs. Properties with five or more units move into commercial multifamily territory with different underwriting criteria and financing requirements.

What happens if my construction project goes over budget?

Cost overruns typically must be covered out of pocket unless your lender approves a loan modification — and many won't. Budget a 10–20% contingency from the start — it isn't optional on investment construction projects. Plan for it before you close, not after the problem appears.