This guide is built for established small to mid-sized businesses — restaurants, medical practices, manufacturers, franchises, gas stations, and others — that need substantial capital and want a clear picture of the process before applying. We cover qualification criteria, the step-by-step application process, current rate ranges, and when a term loan may not be the right tool.

Key Takeaways

- A $500K business term loan is a lump-sum disbursement repaid in fixed monthly installments, not a revolving line of credit

- Most lenders require a credit score of 620–680 minimum, 2+ years in business, and strong annual revenues

- Your debt service coverage ratio (DSCR) determines whether lenders believe you can repay — revenue alone won't close the deal

- SBA 7(a) loans offer the best rates and longest terms; online lenders move faster but carry higher costs

- A bank denial isn't the end of the road — alternative lenders and SBA-preferred brokers work with a wider range of borrower profiles

What Is a $500K Business Term Loan?

A business term loan provides a single lump-sum disbursement (in this case, $500,000) which the borrower repays with interest in fixed monthly installments over a defined period. Terms typically range from 1 to 25 years depending on the lender type and loan purpose.

How It Differs from Similar Products

| Product | Key Difference |

|---|---|

| Line of credit | Revolving — draw, repay, redraw as needed |

| Equipment financing | Asset-tied — the equipment serves as collateral |

| Revenue-based financing | Payments fluctuate with monthly revenue |

| Term loan | Fixed schedule, fixed payments, lump disbursement |

The distinction matters when choosing a product: a term loan works best when you need a defined amount for a specific purpose and can service a fixed monthly payment from existing cash flow.

Common Uses at the $500K Level

- Commercial real estate acquisition or renovation

- Business or franchise acquisition

- Large equipment purchases

- Working capital to support rapid growth

- Debt consolidation and refinancing

According to the SBA, eligible uses for 7(a) term loans include acquiring or improving real estate, working capital, equipment purchases, and refinancing existing business debt, covering the full range of uses listed above.

Do You Qualify? What Lenders Look For

At $500K, lenders don't evaluate just one factor. They look at a combination of credit, history, cash flow, collateral, and industry. Being underprepared on any one of these is a leading cause of denial.

Credit Score

- 700+: Strong position with traditional banks and most SBA lenders

- 620–680: Acceptable for SBA programs and many alternative lenders

- 580–620: Some online lenders will consider this range, but rates increase and terms shorten significantly

Personal credit is the primary filter at most banks, though established businesses will also have their Dun & Bradstreet and Experian Business profiles reviewed. The SBA doesn't publish a universal minimum FICO, but Lendio's marketplace lists 625 as a common threshold for term loans up to $500K.

Time in Business

Most banks and SBA lenders want 2–3 years of operating history at this loan size. Some online lenders will consider 12–18 months if revenue and credit are strong. Startups have narrow options — substantial collateral or an SBA program built for new businesses is typically required.

Annual Revenue and DSCR

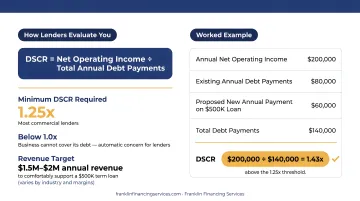

Lenders don't evaluate revenue in isolation. The key metric is your Debt Service Coverage Ratio:

DSCR = Net Operating Income ÷ Total Annual Debt Payments

Most commercial lenders require a DSCR of at least 1.25x. Here's what that looks like in practice:

- Annual net operating income: $200,000

- Existing annual debt payments: $80,000

- Proposed new annual payment on $500K loan: $60,000

- Total debt payments: $140,000

- DSCR: $200,000 ÷ $140,000 = 1.43x ✅ (above the 1.25x threshold)

A DSCR below 1.0 means the business can't cover its debt — an automatic concern for most lenders. Most lenders want to see annual revenues in the $1.5M–$2M range to comfortably support a $500K term loan, though this varies by industry and margins.

Collateral and Personal Guarantee

- Traditional and SBA lenders: Require collateral (real estate, equipment, inventory, receivables) to the extent available. SBA policy requires lenders to take available collateral for loans above $50,000, though lack of collateral alone isn't grounds for denial.

- Personal guarantee: Nearly universal at this loan size. SBA requires personal guarantees from all owners holding 20% or more equity.

- Alternative lenders: Some offer unsecured term loans, but expect shorter terms and much higher rates.

Industry Considerations

Lender appetite varies by industry. Franklin Financing Services' term loan program, for example, explicitly includes restaurants, healthcare, gas stations, hotels, professional services, and agriculture — while excluding cannabis/marijuana businesses, non-profits, and certain financial services firms. Construction businesses often find a better fit through dedicated equipment financing programs rather than general term loans.

Either way, ask any lender directly about their appetite for your specific industry before committing to a full application.

How to Apply: A Step-by-Step Process

Applying for a $500K term loan is more involved than smaller loan amounts. Coming in organized — with clean financials and a clear story — gives you a measurable edge in both approval odds and processing speed.

Step 1: Audit Your Financial Position

Before approaching any lender, compile your key figures:

- Last 2–3 years of revenues and net income (or EBITDA)

- Current monthly debt obligations

- Personal and business credit scores

- Assets available as collateral

Knowing your numbers before the lender finds them lets you address weaknesses proactively — in writing — rather than getting caught off guard during underwriting.

Step 2: Define Your Use of Funds

"General working capital" is not a compelling answer at this loan size. Lenders want to know specifically what the capital will do for your business and how it connects to revenue growth or cost reduction.

A one-page use-of-funds plan that ties the investment to a projected financial outcome will strengthen your application.

Step 3: Gather Required Documentation

Most lenders at this level will require:

- 2–3 years of business and personal tax returns

- Current P&L, balance sheet, and cash flow statement

- 6–12 months of business bank statements

- List of existing business debts

- Collateral documentation (property appraisals, equipment schedules)

- Business formation documents (articles of incorporation, operating agreements, licenses)

- For SBA loans: a business plan and SBA-specific forms, plus a loan packaging fee

SBA applications carry the heaviest documentation load. Working with a qualified intermediary at this stage can meaningfully reduce processing delays.

Step 4: Match Yourself to the Right Lender Type

| Lender Type | Best Fit | Typical Timeline |

|---|---|---|

| Traditional bank | 700+ credit, 3+ years, strong collateral | 4–8 weeks |

| SBA-approved lender | 620+ credit, 2+ years, clear use of funds | 30–90 days |

| Online/alternative lender | Speed priority, less-than-perfect credit | 2–10 business days |

| SBA-preferred broker | Broad credit range, bank turndowns welcome | Varies by product |

Franklin Financing Services — designated as a Preferred Financial Services company by SBA lenders — can help businesses identify the right fit across these categories, including those turned down by traditional banks. Their standard Business Term Loan program (up to $500K) can fund in as little as 3 days; their FAST TRACK program (up to $100K) offers approvals in 24–48 hours.

Step 5: Submit a Complete and Consistent Application

Incomplete applications and inconsistencies between documents are the most common causes of delays and rejections. Before submitting:

- Cross-check figures across all documents for consistency

- Address any blemishes (a late payment, a down year) proactively in a written narrative

- Respond to lender follow-up requests quickly — delays on your end can cause applications to lose momentum or expire

Rates, Terms, and Estimated Monthly Payments

Interest rates on a $500K business term loan vary widely depending on lender type, collateral, and your business profile. Here's what to expect across the most common lending channels.

Rate and Term Ranges by Lender Type

| Lender Type | Approximate Rate Range | Typical Term |

|---|---|---|

| SBA 7(a) — working capital/equipment | Up to prime + 3.0% (cap ~9.75% with prime at 6.75%) | Up to 10 years |

| SBA 7(a) — real estate | Same cap, lower market rates common | Up to 25 years |

| Conventional bank | Varies; Chase publishes 5-year standard terms | 3–10 years |

| Online/alternative lender | Higher rates, lender-specific | 1–5 years |

For FY2026, the SBA has waived both the upfront guaranty fee and annual service fee for standard 7(a) loans — a meaningful cost reduction for borrowers who qualify.

Illustrative Monthly Payments on $500,000

These estimates help you gauge whether the debt service fits your cash flow:

| Rate | Term | Approx. Monthly Payment |

|---|---|---|

| 8% | 10 years | ~$6,066 |

| 10% | 10 years | ~$6,608 |

| 12% | 7 years | ~$8,674 |

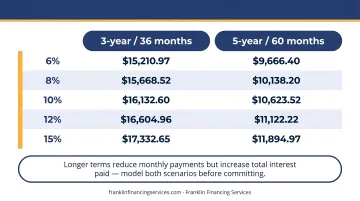

Longer terms reduce monthly payments but increase total interest paid — model both scenarios before committing.

Fees Beyond the Interest Rate

The interest rate alone doesn't tell the full story. Watch for:

- Origination fees (some lenders, like Chase, charge $0; others charge 1–3%)

- SBA loan packaging fees ($750–$2,000 for broker-facilitated SBA applications)

- Appraisal fees for real estate-secured loans

- Prepayment penalties on loans above certain thresholds

- Closing costs for real estate-backed structures

Always request the full fee schedule and calculate the APR rather than comparing interest rates alone.

Common Misconceptions and When a Term Loan Isn't the Right Fit

Three Misconceptions Worth Addressing

"You need perfect credit to qualify." Not true. SBA programs and alternative lenders regularly work with borrowers in the 620–680 range. Strong cash flow, collateral, or a co-borrower can all offset credit weaknesses.

"The lowest rate automatically means the best deal." Term length, prepayment penalties, and total fees all affect the true cost of capital. A 7% loan with a 3% origination fee and a 5-year term may cost more than a 9% loan with no fees and a 10-year term.

"All $500K term loans work the same way." An SBA 7(a) loan, a conventional bank term loan, and an online term loan differ enormously in structure, speed, documentation requirements, and total cost. They are not interchangeable products.

When a Term Loan May Not Be the Right Tool

- A revolving line of credit works better for seasonal or cyclical businesses that need to draw and repay as cash flow shifts

- Revenue-based financing is worth considering if monthly income varies significantly and fixed payments create strain

- Equipment financing typically closes faster and at lower rates when the purchase itself can serve as collateral

Why Applying to Every Lender Backfires

Submitting applications to every lender you can find is a counterproductive strategy. According to FICO, hard inquiries affect your score for up to 12 months — and business loan inquiries don't receive the same rate-shopping grouping protections that mortgage inquiries do. Targeting 2-3 lenders that match your credit profile and loan size is more effective, and it protects your score in the process.

Frequently Asked Questions

How hard is it to get a $500,000 business loan?

Difficulty depends on the lender and your profile. Traditional banks set the highest bar — strong credit, 3+ years, collateral. SBA lenders and alternative lenders serve a broader range. Strong financials, 2+ years of operating history, and organized documentation dramatically improve your odds at any lender type.

How much is the monthly payment on a $500,000 business loan?

Monthly payments vary by rate and term. At 8% over 10 years, expect roughly $6,066/month. At 10% over 10 years, approximately $6,608/month. At 12% over 7 years, around $8,674/month. Fees and loan structure also affect your true monthly obligation.

What's the longest term for a business loan?

The longest terms — up to 25 years — are available through SBA 7(a) and SBA 504 programs for real estate-secured loans. Working capital and equipment loans max out at 10 years under SBA programs. Conventional bank loans typically run 3–10 years; online lenders offer 1–5 years.

What credit score do I need for a $500K business term loan?

Traditional banks generally want 700+. SBA programs and many alternative lenders work with 620–680. Some online lenders consider scores as low as 580, though lower scores bring higher rates and shorter terms.

What documents are needed to apply for a $500K business term loan?

Plan to provide 2–3 years of tax returns, current financial statements (P&L, balance sheet, cash flow), 6–12 months of bank statements, business formation documents, and a debt schedule. SBA loans also require collateral documentation and a business plan.

Can I get a $500K business term loan with bad credit?

Bad credit makes qualifying harder but not impossible. Alternative lenders and some SBA programs weigh offsetting strengths (strong revenue, significant collateral, or a co-borrower) alongside credit history. Businesses turned down by banks often find options through a financing intermediary with access to multiple lender types, like Franklin Financing Services.