Introduction

Growing a business costs money — and not just a little. Opening a second location, buying equipment, or adding staff all require capital that most businesses don't have sitting in a checking account. The timing is never perfect, and traditional banks make it worse: only 42% of small business applicants received the full amount they sought, according to the 2026 Federal Reserve Small Business Credit Survey.

That gap between capital needed and capital available is where expansion plans stall, not because the business idea is flawed, but because the financing structure doesn't match the scale of the opportunity.

Term loans are one of the most effective tools for bridging that gap. This guide covers what term loans actually deliver for expanding businesses, when they make the most sense, and the financing mistakes worth avoiding before you commit.

Key Takeaways

- Term loans provide a fixed lump sum with predictable monthly payments — purpose-built for planned expansion, not reactive borrowing.

- Fixed repayment schedules let owners map cash flow against debt payments before committing to a growth decision.

- Business credit cards carry 16.74%–24.74% APR; merchant cash advances can imply APRs near 70% — term loans are significantly cheaper across a multi-year repayment period.

- SBA-affiliated lenders and specialized financing partners offer viable paths for businesses that traditional banks have turned down.

- Matching loan term to the useful life of the asset being funded is the single most important structural decision a borrower makes.

What Is a Term Loan for Business Expansion?

A business term loan is straightforward: a lender provides a fixed lump sum, and the borrower repays it — with interest — over a defined period through scheduled payments. That structure comes in three general ranges:

- Short-term: 1–2 years

- Intermediate: 2–5 years

- Long-term: 5–10+ years

The SBA describes most 7(a) term loans as repaid monthly from business cash flow, with fixed-rate payments remaining constant throughout the loan term. That consistency is intentional — fixed payments make debt service predictable and easier to plan around.

How Term Loans Apply to Expansion

Term loans fit expansion scenarios that have a defined capital need and a multi-year return horizon. Common uses include:

- Purchasing or leasing a new commercial location

- Acquiring equipment, machinery, or vehicles

- Funding leasehold improvements for a new space

- Hiring and onboarding staff for a new operation

- Entering a new market with upfront marketing and inventory investment

The critical distinction from revolving credit or short-term financing is purpose: a term loan is for investments, not expenses. It's the right tool when a business needs to fund something with a productive life measured in years, not weeks.

For businesses ready to put that structure to work, Franklin Financing Services offers conventional business term loans from $20,000 to $500,000 with fixed rates and repayment terms up to four years, plus SBA 7(a) loans from $150,000 to $5 million for larger expansion initiatives.

Key Advantages of Term Loans for Business Expansion

Advantage 1: Predictable Repayment That Supports Financial Planning

Expansion is expensive before it's profitable. New overhead, new staff, new inventory — all of it costs money before the revenue catches up. In that environment, a variable or unpredictable repayment obligation adds financial risk at exactly the wrong time.

Term loans eliminate that variable. Fixed monthly payments mean the debt obligation is known from day one, which allows owners to:

- Build the payment into the operating budget before the expansion launches

- Model whether projected revenue from the new location or equipment covers debt service

- Identify cash flow problems in the projection stage rather than after commitment

The median U.S. small business holds just 27 days of cash buffer, according to JPMorgan Chase Institute research. Restaurants average just 16 days. With that little margin, a payment structure that fluctuates week to week creates serious financial exposure — not a manageable obligation.

Fixed repayment directly affects three metrics that lenders and operators track:

- Monthly cash flow variance — fixed payments reduce volatility

- Budget adherence rate — owners can plan around a known number

- Debt-service coverage ratio (DSCR) — the ratio of net operating income to debt service, a key underwriting benchmark; a DSCR above 1.0x indicates income exceeds debt obligations

This predictability matters most when opening a second location or making a large equipment purchase — scenarios where the investment horizon runs three to seven years and multi-year cash flow visibility isn't optional.

Advantage 2: Access to Substantial Capital for Long-Term Investment

Most short-term financing products weren't built for capital-intensive expansion. A merchant cash advance might solve a 90-day cash flow gap — it wasn't designed to fund a $400,000 equipment purchase or a full commercial buildout.

Term loans scale to the actual capital requirement. SBA 7(a) loans — the benchmark for government-backed expansion financing — carry a maximum of $5 million per loan, with eligible uses covering real estate, equipment, working capital, leasehold improvements, and business acquisitions. The SBA also raised its cumulative 7(a) and 504 loan limit to $10 million in 2026, increasing the ceiling for multi-phase growth.

Why Underfunding Is an Expansion Risk

Underfunding is one of the most common expansion failure modes. A business opens a second location or installs new equipment but runs short on working capital during the ramp-up period. The expansion itself is sound — the financing structure just wasn't sized correctly.

A properly structured term loan covers the full capital need upfront, preserving operating liquidity throughout the growth phase.

KPIs impacted:

- Revenue per new location

- Time-to-profitability for the new operation

- Asset utilization rate

- Return on expansion investment

This capital access is most critical when expansion requires physical infrastructure — commercial real estate, manufacturing equipment, fleet vehicles — where asset value justifies long-term borrowing and short-term financing is structurally mismatched.

Advantage 3: Lower Cost of Capital vs. Alternative Financing

Cost of capital is cumulative. On a one-month bridge loan, a higher rate barely registers. On a five-year expansion investment, even a few percentage points of difference adds up to tens of thousands of dollars.

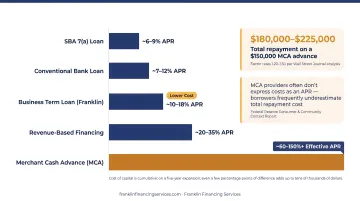

Here's what the rate comparison looks like across common financing options:

| Financing Type | Typical Cost |

|---|---|

| SBA 7(a) term loan | Base rate + up to 3.0% (loans above $350K) |

| Business credit card (Chase Ink Business Cash) | 16.74%–24.74% variable APR after intro period |

| Merchant cash advance (typical factor rate) | 1.20–1.50 factor rate |

| MCA APR equivalent (Fed example) | ~70% APR for a 1.15 factor rate |

The Federal Reserve's Consumer & Community Context report notes that MCA providers often don't express costs as an APR — which means borrowers frequently underestimate total repayment cost. A Wall Street Journal analysis puts typical MCA factor rates at 1.20 to 1.50, meaning a $150,000 advance costs $180,000 to $225,000 back — often over a compressed repayment window.

SBA Rate Structure

SBA 7(a) loans carry rate caps tied to a base rate plus a spread — currently capped at base rate plus 3.0% for loans above $350,000. For most growing businesses, that's a substantially lower effective rate than credit cards or MCAs, particularly over a multi-year repayment horizon.

Every dollar saved on interest stays in the business. On a five-year expansion loan, the gap between term loan rates and credit card APRs can represent six figures in cumulative financing charges — money that would otherwise fund staffing, marketing, or operations.

The rate advantage compounds most on long-term loans (5+ years) and large loan amounts — making it most impactful in capital-intensive industries like manufacturing, hospitality, and healthcare.

What Happens When Businesses Expand Without Adequate Financing

The pattern is recognizable: a business owner sees an opportunity, moves on it before proper financing is in place, and funds the gap with whatever is available: personal credit cards, a merchant cash advance, or a short-term loan at unfavorable terms.

The consequences compound quickly:

- Higher cost of capital — reactive borrowing means accepting whatever terms are available, not optimal ones

- Compressed cash flow — short-term financing with weekly or daily repayments leaves less working capital for the expansion to operate

- Credit damage — missed payments under financial strain reduce the business's ability to access better financing later

- Collateral risk — the FTC has documented MCA providers seizing personal and business assets in enforcement actions against deceptive operators

The BLS reports that only 34.7% of business establishments born in 2013 were still operating in 2023 — a 10-year survival rate that reflects the fragility of small businesses under financial pressure. Expansion amplifies that pressure.

That survival gap is largely a financing problem. Term loans secured before expansion begins — structured to match the actual investment horizon — carry better rates, more manageable repayment schedules, and leave the business in a stronger negotiating position than reactive borrowing ever will.

How to Get the Most Value from a Business Term Loan

Getting full value from a term loan comes down to three things: matching it to the right purpose, tracking performance against your projections, and choosing the right lender. Here's what that looks like in practice:

Match loan term to asset life. A seven-year loan on equipment with a 10-year lifespan makes sense. A two-year loan on the same equipment creates unnecessary payment pressure and misaligns repayment with productive use. The SBA's own guidance on 7(a) loan structure reflects this: loan terms vary by purpose because the investment horizon varies.

Track KPIs from day one. The business plan that justified the loan should have revenue and margin projections. Track actual performance against those numbers quarterly — DSCR, monthly cash flow, and expansion-location revenue are the most relevant metrics. Catching a revenue shortfall in month three gives you options. Catching it in month eighteen does not.

Compare lender types before you apply. Not all term loans are priced or structured the same. SBA-backed loans typically offer more favorable rates and longer terms than conventional alternatives, but qualification requirements differ by lender type. Large banks approve roughly 40% of small business applicants; small banks approve 89%, according to the Kansas City Fed's 2024 lending survey.

Those approval gaps matter — especially if a major bank has already turned you down. Franklin Financing Services works beyond the standard approval window. Franklin works with businesses carrying imperfect credit histories, prior bank rejections, or non-traditional revenue structures. As a Preferred Financial Services company designated by SBA lenders, Franklin processes SBA 7(a) loans faster than most intermediaries. Its FAST TRACK conventional term loan program requires only an application and four months of bank statements — with approval in 24–48 hours and funding in as little as 3–7 days.

Conclusion

The case for term loans in business expansion rests on three compounding advantages: financial predictability, capital adequacy, and lower borrowing cost. Each matters on its own. Together, they give a growing business the structural foundation to expand without putting day-to-day operations at risk.

Term loan financing should be treated as a strategic tool, not a last resort. The earlier a business secures the right structure — before expansion is underway, before cash flow is under pressure — the more control it maintains throughout growth. Businesses that plan financing proactively consistently outperform those that borrow reactively: they access better rates, negotiate stronger terms, and avoid the compounding cost of urgency.

If you're evaluating term loan options for an upcoming expansion, Franklin Financing Services works with small and mid-sized businesses across the country to identify the right loan structure — whether that's a conventional term loan, an SBA 7(a) program, or another product that fits your specific growth stage.

Frequently Asked Questions

What are the advantages of using term loans?

Term loans offer predictable fixed monthly payments and access to substantial capital for long-term investments. Rates are generally lower than credit cards or merchant cash advances, and consistent repayment builds your business credit over time.

What is a term loan for business expansion?

It's a lump-sum loan repaid with interest over a fixed period — typically one to ten or more years — used to fund capital-intensive expansion goals like opening new locations, purchasing equipment, or entering new markets.

What types of business expansion can a term loan fund?

Common uses include purchasing or leasing commercial space, acquiring equipment or machinery, hiring and onboarding staff, funding leasehold improvements, investing in technology infrastructure, or financing a market-entry campaign.

How is a term loan different from a line of credit for expansion?

A term loan delivers a fixed lump sum upfront, making it the right fit for defined, one-time capital needs like a new location or major equipment purchase. A line of credit allows repeated draws, making it better suited for ongoing or variable expenses.

How do I qualify for a term loan for business expansion?

Lenders typically evaluate business credit history, cash flow, revenue, time in business, and sometimes collateral. Businesses that don't meet traditional bank criteria may still qualify through SBA-affiliated lenders or specialized financing partners with broader eligibility standards.

Can a business get a term loan after being turned down by a bank?

Yes. A bank rejection doesn't close off all options. Specialized lenders and SBA Preferred Financial Services companies work with businesses that have limited collateral, imperfect credit, or prior rejections — often with faster approval timelines than traditional institutions.