According to the Federal Reserve's 2024 Small Business Credit Survey, 56% of small firms cited paying operating expenses as a financial challenge, and 51% cited uneven cash flows. For event planners, both problems hit at once and on a deadline.

This guide covers the financing options available to event planning businesses — from working capital loans and lines of credit to SBA loans and merchant cash advances — along with what you can use funds for, how to qualify, and how to apply. Whether you're managing your first growth push or bridging a seasonal slow period, this is a practical decision-making resource.

Key Takeaways

- Event planners face a structural cash flow gap: expenses come first, client payments come later

- Multiple loan types exist — working capital loans, equipment financing, SBA loans, MCAs — each matched to different needs, from short-term cash gaps to long-term equipment purchases

- Alternative lenders accept credit scores as low as 580–620; bad credit isn't automatically disqualifying

- Fast-track products can deliver funding in as little as 3–7 days for time-sensitive needs

- Poor credit or prior bank rejections don't close every door — specialized lenders and intermediaries like Franklin Financing Services exist specifically for these situations

Why Event Planning Businesses Need Financing

The Upfront Cost Problem

Most service businesses invoice after delivering their service. Event planners are different — they pay before the event happens. Venue deposits, catering minimums, AV rentals, staffing advances, décor orders: all of it lands on your account weeks before the event date, and often months before the client's balance clears.

That gap doesn't just create stress. It caps your capacity. If your operating capital is tied up in Event A, you may not have the liquidity to secure deposits for Event B — even if you've already signed the contract.

Seasonal Revenue Swings

Event planning revenue isn't distributed evenly across the year. According to The Knot, fall has been the most popular wedding season since 2015, with 43% of couples marrying in autumn and more than 67% choosing summer or fall. Add corporate holiday events in Q4 and spring galas, and the pattern becomes clear: most revenue concentrates in a few months, while overhead runs year-round.

Financing bridges predictable slow periods without forcing you to make difficult choices — laying off staff, declining new bookings, or draining personal savings just to cover January payroll.

The Growth Barrier

Scaling an event planning business requires spending money before you see the return. Common growth moves that demand significant upfront capital include:

- Hiring an additional coordinator or event staff

- Purchasing AV or production equipment

- Expanding into a second market or venue category

- Building out a client management or booking system

Client deposits and personal savings rarely cover these costs in full.

A business loan lets you invest ahead of demand — securing the team, tools, and capacity you need before the next busy season arrives.

Types of Loans Available for Event Planning Businesses

Event planning companies can access several financing products. The right choice depends on what the funds are for, how urgently you need them, and your current financial profile.

Working Capital Loans

Working capital loans are lump-sum, short-to-medium-term financing — typically $20,000–$500,000, repaid over 1–4 years at a fixed rate. They cover day-to-day operating costs: vendor payments, payroll, insurance, marketing, and the recurring expenses that don't pause between events.

Franklin Financing Services offers working capital loans through their Business Term Loan program, including a FAST TRACK option ($20,000–$100,000) that requires only an application and four months of bank statements, with approval in 24–48 hours and funding in as little as 3 days.

Business Lines of Credit

A revolving line of credit lets you draw funds as needed and repay on a rolling basis, paying interest only on what you use. This structure suits event planners well — you can tap the line to cover a venue deposit, repay it once the client invoice clears, and draw again for the next booking.

It's especially useful when multiple events are running concurrently and cash demands spike unpredictably.

Equipment Financing

Equipment financing is a loan designed specifically to purchase physical assets — AV systems, lighting rigs, staging, tents, furniture, transport vehicles. The equipment typically serves as collateral, which makes approval more accessible even with imperfect credit.

If you're renting the same AV rig for every event, you're paying vendor margins every time. Owning core inventory eliminates that recurring cost and improves per-event margins — and loan repayment is structured over the same period those assets are actively earning.

SBA Loans

SBA 7(a) loans offer government-backed financing up to $5 million, with repayment terms up to 10 years for equipment and working capital (up to 25 years for real estate). Rates are competitive, and there are no points or balloon payments.

Best suited for larger investments: acquiring another event company, purchasing a vehicle fleet, renovating a dedicated studio, or bulk equipment purchases. The application process is more involved, but the terms reward the effort.

Franklin Financing Services holds a Preferred Financial Services designation from SBA lenders, which enables faster loan processing for qualifying applicants — a meaningful advantage for businesses that want SBA terms without the typical wait.

Merchant Cash Advances and Revenue-Based Financing

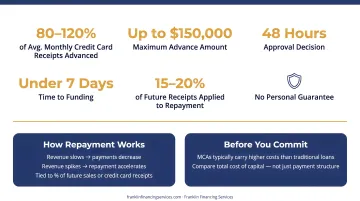

Merchant cash advances (MCAs) and revenue-based financing tie repayment to a percentage of future sales or credit card receipts rather than a fixed monthly payment. When business slows, payments decrease. When revenue spikes, repayment accelerates.

Franklin Financing Services' Easy Pay Cash Advance advances 80–120% of average monthly credit card receipts (up to $150,000), with repayment set at 15–20% of future receipts. Approvals come in 48 hours, funding in under 7 days, and no personal guarantee is required.

MCAs typically carry higher costs than traditional loans. Compare the total cost of capital — not just the payment structure — before committing.

Term Loans

Traditional term loans offer a lump sum with a fixed repayment schedule over 1–10 years. They work well for defined, larger investments with a predictable return: opening a second location, purchasing a storage warehouse, or making a bulk equipment purchase. The fixed schedule makes cash flow planning predictable, which matters when you're managing event timelines and client billing cycles simultaneously.

What Can You Use Event Planning Business Loans For?

Equipment and Operations

Owning your core inventory reduces dependency on rental vendors and captures the margin you'd otherwise pay them. Equipment financing aligns your repayment schedule with the revenue those assets generate, so the loan effectively pays for itself.

Common assets worth financing include:

- AV gear and sound systems

- Staging, tents, and lighting rigs

- Linens, décor, and tableware inventory

- Transport vehicles for load-in and setup

Staffing and Payroll

Events succeed or fail on execution, and execution is people. A working capital loan or cash advance ensures you can hire, train, and pay temporary event-day staff reliably — regardless of when client invoices clear.

This matters for quality control. A reliable freelance roster doesn't stay available if you're inconsistent with payment timing.

Marketing and Business Development

Lead flow doesn't happen passively. Bookings depend on consistent upfront investment across multiple channels:

- Professional photography and portfolio content

- Website design and SEO

- Social media advertising

- Bridal or corporate expo participation

A line of credit fits this pattern well. You draw ahead of booking season, recover costs through new contracts, then draw again for the next campaign — without tying up operating cash.

Venue Deposits and Concurrent Bookings

Holding multiple dates simultaneously means holding multiple deposits simultaneously. A revolving line of credit covers those prepayments across concurrent bookings, with each line repaid as client balances clear.

How to Qualify for an Event Planning Business Loan

Qualification requirements vary significantly between traditional banks and alternative lenders. Many event planners turned down by banks find financing through lenders that assess the full business picture — revenue trends, cash flow, and future bookings — rather than credit score alone.

Time in Business

| Lender Type | Minimum Time in Business |

|---|---|

| Alternative lenders (most products) | 6–12 months |

| Traditional banks | 2+ years |

| SBA loans (varies by lender) | Established operating history with documented cash flow |

| Easy Pay Cash Advance (Franklin) | 1 year or less |

The longer your track record, the broader your product options and the better your terms.

Annual Revenue

Most alternative lenders set minimum revenue thresholds around $100,000 annually, though some lower-entry products accept less. Forbes Advisor's 2026 benchmark cites $100,000 as a common floor, with Bankrate noting the same threshold for competitive products.

Seasonal revenue patterns are common in event planning. Explain them in your application with supporting booking data, signed contracts, or projected revenue schedules.

Credit Score

- 580–620: Minimum range for certain alternative lending products

- 680+: Unlocks better rates and more product options

- Below 580: May still qualify for secured products like equipment financing

Franklin Financing Services' Easy Pay Cash Advance explicitly accepts poor credit, late payments, and prior bank turndowns — qualification is based on credit card processing volume, not FICO score.

Cash Flow and Bank Statements

Lenders review 3–6 months of business bank statements to verify revenue consistency and spot irregularities. Frequent overdrafts are a red flag; seasonal dips are expected.

Where possible, attach upcoming contracts or signed bookings to your application — this context goes a long way with underwriters reviewing a seasonal business.

Business Plan and Use of Funds

Alternative lenders don't always require a formal business plan, but a brief explanation of how the funds will be used and what return you expect strengthens any application. SBA loans are the exception — a full business plan with financial projections is a standard requirement.

How to Apply for an Event Planning Business Loan

Step 1 — Determine Your Funding Need and Match It to the Right Product

Calculate exactly how much capital you need and what it's for. Equipment purchase? Equipment financing. Covering concurrent venue deposits? Line of credit or cash advance. Seasonal staffing push? Working capital loan. The right match accelerates approval and ensures repayment terms fit your cash flow timeline.

Step 2 — Gather Your Documentation

For most alternative lenders, this means:

- 3–6 months of business bank statements

- Government-issued ID

- Proof of business ownership

- Basic revenue information

SBA and traditional bank applications additionally require tax returns, a business plan, and financial projections. Organized documents can cut days off the review process.

Step 3 — Submit and Compare Offers

Once your documents are ready, the process moves quickly. Alternative lenders like Franklin Financing Services can deliver approvals in 24–48 hours and fund within 3–7 days for qualifying products. Before accepting any offer, review:

- Total cost of capital (not just the monthly payment)

- Prepayment penalties or hidden fees

- Whether the repayment structure fits your revenue cycle

Compare multiple offers when possible. A slightly higher monthly payment on a shorter term can cost far less overall than a lower payment stretched over years.

Frequently Asked Questions

What can event planners write off on taxes?

Event planning businesses can typically deduct ordinary and necessary business expenses including equipment purchases (Section 179 deductions — see IRS Publication 334 for current limits), marketing costs, software subscriptions, vehicle mileage, subcontractor fees, and business insurance. Consult a tax professional for your specific situation.

How hard is it to get a $1,000,000 business loan?

A $1M loan is achievable but requires strong financials — typically 2+ years in business, documented revenue, a solid credit profile, and a clear use of funds. SBA 7(a) loans support up to $5M for qualified businesses. Franklin Financing Services works with both the SBA 7(a) program and Revenue-Based Financing at this size, and Preferred Lender status helps speed up SBA processing.

Is a merchant cash advance a legal business financing product?

Yes. Merchant cash advances are legal commercial financing products in the U.S., structured as a purchase of future receivables rather than a traditional loan. Because of that structure, they're subject to less federal regulation than conventional loans — several states including California and New York have enacted their own commercial disclosure requirements. Read all terms carefully and compare total cost against other options before signing.

Can I get an event planning business loan with bad credit?

Bad credit doesn't automatically disqualify you. Alternative lenders assess revenue, cash flow, and business activity — and secured products like equipment financing may be available regardless of score. Franklin Financing Services' Easy Pay Cash Advance accepts poor credit, prior bank turndowns, and late payments; one party planner secured $45,000 through that program.

What documents do I need to apply?

Most alternative lender applications require 3–6 months of business bank statements, a government-issued ID, proof of business ownership, and basic business information. The FAST TRACK program at Franklin Financing Services requires only an application and four months of bank statements. SBA loan applications additionally require tax returns, a formal business plan, and financial projections.

How quickly can an event planning business get funded?

Alternative lenders can typically approve applications within 24–48 hours and deposit funds within 3–7 business days. Franklin Financing Services' FAST TRACK loan and Easy Pay Cash Advance both fall within this window. SBA loans involve more extensive underwriting and generally take 30–90 days from application to funding, though Preferred Lender status can reduce that timeline.