Securities-based loans outstanding reached $138 billion as of Q1 2024, according to the Federal Reserve—and when combined with margin loans, asset-backed consumer lending approaches $318 billion. That's not a niche strategy; it's a mainstream liquidity tool.

This guide covers exactly how to borrow against an investment portfolio: which assets qualify, how much you can realistically access, what lenders evaluate, and the risks you need to plan around before signing anything.

Key Takeaways

- Stocks, bonds, ETFs, and mutual funds in taxable brokerage accounts can serve as collateral—retirement accounts do not qualify

- Securities-based lines of credit typically allow borrowing 50%–95% of portfolio value, depending on asset type

- Loan proceeds cannot be used to purchase additional securities — most lenders prohibit this by contract

- The biggest risk is a margin call: portfolio declines can force immediate repayment or asset liquidation

- Business owners who lack a qualifying portfolio can still access financing through SBA loans, merchant cash advances, or revenue-based programs

How to Borrow Against Your Investment Portfolio

Step 1: Assess Your Portfolio's Eligibility

Before approaching any lender, audit what you actually hold.

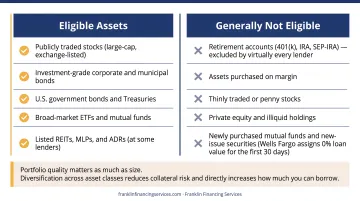

Eligible assets typically include:

- Publicly traded stocks (large-cap, exchange-listed)

- Investment-grade corporate and municipal bonds

- U.S. government bonds and Treasuries

- Broad-market ETFs and mutual funds

- Listed REITs, MLPs, and ADRs (at some lenders)

What generally doesn't qualify:

- Retirement accounts (401(k), IRA, SEP-IRA)—excluded by virtually every lender

- Assets purchased on margin

- Thinly traded or penny stocks

- Private equity and illiquid holdings

- Newly purchased mutual funds and new-issue securities (Wells Fargo assigns 0% loan value for the first 30 days)

Portfolio quality matters as much as size. A concentrated position in a single stock—even a high-quality one—reduces borrowing power and raises lender concern. Diversification across asset classes reduces collateral risk and directly increases how much you can borrow.

Step 2: Determine How Much You Can Borrow

LTV ranges vary by asset type and lender. FINRA states that a typical SBLOC permits borrowing 50% to 95% of investment account value, depending on the assets held. In practice, most investors with a diversified equity and bond portfolio land in the 50%–70% range.

Wells Fargo's published guide shows eligible stocks, ETFs, and mutual funds may carry borrowing power up to 60%. Volatile securities and concentrated positions receive lower advance rates—though exact percentages aren't publicly standardized across lenders.

Before calculating your ceiling, clarify how you'll use the funds. This matters because:

- SBLOCs cannot be used to purchase or carry additional securities

- Most lenders prohibit using proceeds to repay margin loans

- Permitted uses include real estate purchases, business expenses, taxes, tuition, and major personal expenditures

Knowing your purpose before applying prevents a mismatch with lender restrictions—and positions you to choose the right lender from the start.

Step 3: Choose a Lender and Submit an Application

Lender minimums vary considerably. Here's what major providers currently require:

| Lender | Minimum Portfolio/Line | Custody Requirement |

|---|---|---|

| Wells Fargo Priority Credit Line | $75,000 initial borrowing power | Wells Fargo Advisors assets |

| Schwab Pledged Asset Line | $100,000 minimum line | Schwab non-retirement assets |

| Merrill Loan Management Account | $100,000 minimum line | Merrill/Bank of America accounts |

| Fidelity SBLOC | $500,000 pledged assets; $100,000 min line | Fidelity non-retirement accounts |

| E*TRADE/Morgan Stanley Line of Credit | Not publicly specified | E*TRADE brokerage account |

Most lenders require assets to be custodied with them—so if your portfolio sits at Vanguard and you apply at Schwab, you'll likely need to transfer assets first.

Documentation typically required:

- Current portfolio statements

- Account ownership verification

- Statement of intended use of proceeds

Unlike a mortgage, there's no home appraisal or extensive income underwriting. Schwab and Merrill both indicate approvals can occur within one business day, with funds available shortly after.

Step 4: Review Terms, Pledge Collateral, and Draw Funds

Read every line of the loan agreement before signing. Focus specifically on:

- Variable rate tied to SOFR: As of mid-June 2026, SOFR sits at approximately 3.62%. Schwab's tiers run from SOFR + 4.40% (~8.03%) for smaller lines to SOFR + 2.40% (~6.03%) for balances above $2.5 million. Fidelity's spread ranges from 1.90%–3.10% based on line size

- Maintenance threshold: The collateral value floor below which a margin call is triggered—understand this number before you draw

- Demand feature: Many SBLOCs are uncommitted lines, meaning the lender can demand full repayment at any time regardless of whether you've met your obligations

- Repayment structure: Confirm whether you can repay and redraw freely, or whether the facility operates on a fixed term

Once terms are agreed, the designated securities are pledged in a restricted account. Draw only what you need, and map out a repayment timeline before accessing funds—with variable rates, your borrowing cost can rise even when your balance stays the same.

What Lenders Evaluate: Key Factors That Affect Your Loan Terms

Portfolio size is just the starting point. Four variables determine what you actually qualify for—and understanding them helps you negotiate from a position of knowledge.

Portfolio Size and Diversification

Larger, diversified portfolios get better terms in LTV, spreads, and available credit. A $500,000 portfolio spread across large-cap equities, Treasuries, and broad ETFs will qualify for higher LTVs and lower spreads than the same dollar amount concentrated in a single sector.

Most bank-issued SBLOCs set the floor at $75,000–$500,000 in pledged assets. Below those minimums, a margin loan through a brokerage account is typically the only option.

Asset Type and Liquidity

Lenders price risk based on how quickly they can liquidate collateral if needed. The asset hierarchy roughly looks like this:

- Most favorable: U.S. Treasuries, broad-market ETFs, large-cap blue-chip stocks

- Acceptable with lower LTV: Investment-grade corporate bonds, diversified mutual funds

- Reduced or rejected: Thinly traded equities, volatile single stocks, private equity, crypto

The less liquid the holding, the lower the advance rate—and some assets can drag down the LTV for an otherwise strong portfolio.

Loan-to-Value Ratio and Maintenance Thresholds

Asset quality feeds directly into your LTV ceiling—but the maintenance threshold is the figure that creates real risk. Wells Fargo's published guide illustrates this clearly:

Assuming a 36% maintenance requirement on a $100,000 portfolio:

- At 60% leverage ($60,000 borrowed): a margin call triggers after just a 6% portfolio decline

- At 50% leverage ($50,000 borrowed): the buffer extends to a 22% decline

- At 25% leverage ($25,000 borrowed): the portfolio can fall 60% before a call is triggered

Those numbers explain why most financial advisors recommend drawing no more than 25%–35% of portfolio value—even when the lender permits more. The buffer you leave today determines how much volatility you can survive tomorrow.

Interest Rate Type and Market Environment

All major SBLOC providers currently price off SOFR. When benchmark rates rise, your borrowing cost increases automatically—the portfolio's performance doesn't insulate you. Federal Reserve data shows this dynamic in practice: securities-based loans peaked at $174.7 billion in Q3 2022. By Q1 2024, that figure had dropped to $138 billion as rising rates eroded the strategy's appeal.

In a rising-rate environment, the cost of keeping the loan can exceed the benefit of staying invested.

Common Mistakes and Risks to Avoid

Most bad outcomes in securities-based lending trace back to one of four avoidable errors:

Overborrowing near the LTV ceiling. A 60% LTV borrower has little buffer before a market dip triggers a margin call. Forced liquidation at a market low is exactly the capital gains event most borrowers were trying to avoid.

No contingency plan for margin calls. FINRA warns that maintenance calls must typically be met within 2 to 3 business days. Without liquid cash reserves outside the pledged portfolio, your only options are an immediate deposit or a forced asset sale — so write this plan down before drawing funds.

Misusing loan proceeds. SBLOCs contractually prohibit using proceeds to purchase securities or repay margin loans. These restrictions are enforced by lenders, and violations can trigger immediate loan demand.

Treating the demand feature as hypothetical. Unlike a term loan, an SBLOC can be called by the lender at any time. This is a short-to-medium-term liquidity tool — not a permanent financing solution. Have a clear exit strategy before you draw.

Alternatives to Borrowing Against Your Investment Portfolio

Not every investor qualifies for an SBLOC—and not every situation calls for one.

Margin Loans

Best for active investors with very short repayment timelines (days to weeks). Margin loans require no separate application and funds are available immediately through an existing brokerage account. The trade-offs: higher interest rates (Fidelity and Schwab currently carry base rates above 10%), a hard 50% initial margin cap under Regulation T, and strict maintenance enforcement. Funds can be used for any lawful purpose, including additional securities purchases.

Home Equity Line of Credit (HELOC)

Better suited for homeowners who need larger amounts over longer timeframes. Current national average HELOC rates sit near 7.47%, and interest may be tax-deductible when funds are used for home improvement per IRS Publication 936. The trade-offs: HELOCs take weeks to arrange, require home appraisal and income underwriting, and put the borrower's home at risk if payments are missed.

Business Financing Solutions

For business owners who need capital but lack a qualifying investment portfolio—or whose portfolio falls below lender minimums—dedicated business financing is often more accessible and doesn't carry margin call risk. Franklin Financing Services works with a national network of lenders to identify the right structure for each business, including:

- SBA 7(a) loans: $150,000–$5 million, suited for established businesses with steady cash flow and a clean bankruptcy history

- Merchant cash advances: up to $150,000, with 48-hour approvals for businesses processing $8,000 or more monthly in credit card sales

- Revenue-based financing: $50,000–$1 million, available to businesses generating $1 million or more in annual revenue

- Business term loans: $20,000–$500,000, with funding in as little as three days

None of these options require pledging a personal investment portfolio, and they're structured for businesses that don't meet traditional bank criteria. Franklin Financing Services offers a free financing evaluation for any business unsure of which path fits best.

Frequently Asked Questions

Can you borrow against an investment portfolio?

Yes. Investors can use publicly traded stocks, bonds, ETFs, and mutual funds held in taxable brokerage accounts as collateral through an SBLOC or margin loan, without selling the underlying holdings. Retirement accounts like IRAs and 401(k)s do not qualify.

Is it smart to borrow against your investment portfolio?

Yes, when the expected investment return or avoided tax cost outweighs the borrowing cost. The strategy requires careful risk management around market volatility, variable interest rates, and the lender's ability to call the loan at any time.

How large does a portfolio need to be to borrow against it?

Most bank-issued SBLOCs require $75,000 to $500,000 in pledged assets depending on the lender (Fidelity's minimum is $500,000; Wells Fargo's floor starts at $75,000 in initial borrowing power). Smaller portfolios typically only qualify for margin loans through a brokerage account.

What types of investments can be used as collateral?

Eligible assets generally include publicly traded stocks, investment-grade bonds, mutual funds, and ETFs held in taxable brokerage accounts. Retirement accounts, illiquid assets, crypto, and concentrated single-stock positions are typically excluded or heavily discounted.

What happens if my portfolio value drops after taking out the loan?

If the portfolio falls below the lender's maintenance threshold, you must deposit additional cash or securities within 2 to 3 business days, or the lender can sell pledged assets to restore the required collateral ratio, potentially triggering the capital gains you were trying to avoid.

Can I use a portfolio-backed loan for my business?

Most SBLOCs explicitly permit business uses, but proceeds cannot be used to purchase securities or repay margin loans. For ongoing operational needs, a separate business financing structure keeps your personal investment portfolio out of the equation.