Introduction

Most business owners know that accounts receivable exists. Fewer run it as the structured system it needs to be.

That gap matters. The accounts receivable (AR) cycle is the end-to-end process a business follows to collect payment for goods or services sold on credit, starting from the sale and ending when cash hits the bank account. It's not just bookkeeping. For small and mid-sized businesses, it's the primary mechanism that converts revenue into usable cash for payroll, inventory, and daily operations.

The problem? According to the Federal Reserve's 2025 Small Business Credit Survey, 51% of small employer firms cite uneven cash flows as a top financial challenge, and 56% struggle to cover operating expenses. Slow collections are rarely the only cause, but they're a consistent contributor.

Running AR informally, with no credit checks, inconsistent invoicing, and reactive follow-up, leaves cash stranded in outstanding invoices while expenses keep arriving on schedule.

This guide walks through every stage of the AR cycle, the factors that affect it, and what to do when collections stall.

TL;DR

- The AR cycle starts with a credit sale and ends when payment is collected and recorded

- A structured cycle covering credit checks, invoicing, collections, and reconciliation directly reduces late payments and bad debt

- DSO (Days Sales Outstanding) and AR Turnover Ratio are the two core metrics for monitoring cycle health

- Most AR breakdowns happen at the invoicing, collections, and dispute stages — usually due to missing process, not missing effort

- AR financing lets businesses access outstanding invoice value immediately rather than waiting months for customers to pay

What Is the Accounts Receivable Cycle?

The AR cycle is the structured sequence of steps a business follows to manage, track, and collect money owed by customers after a credit sale. It covers everything from the moment an invoice is issued to the moment payment is received and recorded.

This is distinct from accounts payable, which tracks what the business owes to others. AR is a current asset on the balance sheet; AP is a current liability. They are opposite sides of the same credit-based transaction. Understanding that distinction also clarifies where the AR cycle fits within a broader operational process.

AR Cycle vs. Order-to-Cash

The AR cycle is sometimes confused with the broader order-to-cash (O2C) process — but they don't cover the same ground:

- Order-to-Cash (O2C): Covers the full customer journey — order intake, fulfillment, shipping, invoicing, and payment collection

- AR Cycle: Focuses specifically on the post-sale, invoice-to-payment workflow

The AR cycle sits inside O2C. It begins after delivery and ends at reconciliation.

When the AR cycle breaks down — through slow invoicing, missed follow-ups, or disputed charges — cash flow suffers even when sales are strong. The entire process exists to convert outstanding invoices into collected revenue without letting bad debt erode the bottom line.

How the Accounts Receivable Cycle Works: Step by Step

The specifics vary by industry and business size, but the logical sequence holds regardless of whether two people handle your accounting or a full AR team does. Each stage directly affects the next, so a delay early on compounds by the time you reach collections.

Step 1: Credit Evaluation

Before extending credit terms, assess whether the customer can actually pay. This means reviewing payment history, checking financial stability, and requesting trade references when appropriate. Set a credit limit and define payment terms (Net 30, Net 60) upfront.

Skipping this step is one of the most common — and costly — mistakes in the AR cycle. Customers who weren't creditworthy at the start rarely improve mid-cycle.

Step 2: Invoice Creation and Delivery

Once goods or services are delivered, generate an accurate invoice and send it immediately. Every complete invoice should include:

- Total amount due with itemized line items

- Invoice date and payment due date

- Accepted payment methods

- Business contact information for questions

One thing many businesses overlook: the payment clock starts when the customer receives the invoice, not when you deliver the product. Delayed invoicing directly delays payment.

Step 3: Payment Tracking

Use an accounts receivable aging report to monitor outstanding invoices. Aging reports categorize invoices as:

- Current (not yet due)

- 1–30 days overdue

- 31–60 days overdue

- 61–90 days overdue

- 90+ days overdue (high risk of becoming bad debt)

Reviewing this report weekly — not monthly — lets you catch problems before they escalate.

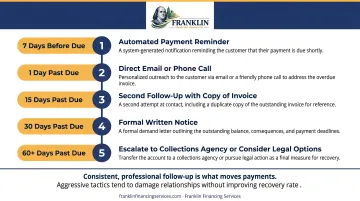

Step 4: Collections and Follow-Up

A structured escalation schedule outperforms ad hoc follow-up every time. A practical sequence:

- 7 days before due date: Automated payment reminder

- 1 day past due: Direct email or phone call

- 15 days past due: Second follow-up with copy of invoice

- 30 days past due: Formal written notice

- 60+ days past due: Escalate to collections agency or consider legal options

Consistent, professional follow-up is what moves payments. Aggressive tactics tend to damage relationships without improving recovery rates.

Step 5: Dispute Resolution and Cash Application

When customers dispute invoice amounts (pricing errors, missing documentation, incorrect quantities), resolve them fast. Unresolved disputes stall the entire collection cycle and damage the business relationship.

Once payment arrives, match it accurately to the correct invoice. This process is called cash application, and getting it right matters: mismatched payments create reconciliation headaches and make aging reports unreliable.

Step 6: Reconciliation and Reporting

The final step closes the loop. Reconcile AR records against payments received, update the balance sheet, and calculate key performance metrics:

- Days Sales Outstanding (DSO): Average time from sale to cash receipt

- AR Turnover Ratio: How often AR is collected within a period

- Bad Debt Write-Offs: Confirmed uncollectible balances removed from AR to keep reporting accurate

Tracking these metrics over time reveals patterns — slow-paying customer segments, seasonal cash flow gaps, or credit policy gaps worth tightening.

Why the AR Cycle Matters for Small and Mid-Sized Businesses

A business can show strong revenue on paper while struggling to cover basic operating expenses. This happens when collections consistently lag behind sales — a cash-poor company that looks profitable.

The Cash Flow Connection

The Federal Reserve's 2024 Payments Report found that roughly 4 in 5 small firms face challenges related to customer payments, and customer payments are the primary cash source for these businesses. For most small businesses, that makes collections a core operational risk, not a back-office afterthought.

A well-managed AR cycle shortens the gap between delivery and cash receipt. That cash funds:

- Payroll

- Supplier payments

- Inventory replenishment

- Reinvestment in growth

Bad Debt Risk Is Real

Atradius's 2024 U.S. B2B Payment Practices report found that 8% of all B2B invoices resulted in bad debts on average. For businesses operating on thin margins, that figure can be the difference between a profitable year and a loss.

A structured AR cycle reduces this risk through:

- Credit checks that keep poor-risk customers off credit terms

- Timely invoicing that starts the payment clock immediately

- Consistent follow-up that catches delinquency early

- Allowance for doubtful accounts — a balance sheet reserve that anticipates likely write-offs and avoids income statement surprises

The Customer Relationship Factor

Managing bad debt risk is only part of the picture — how you handle billing also shapes how customers perceive your business. Professional, consistent AR processes build trust. Accurate invoices, clear terms, and respectful follow-up signal that you run a serious operation. Inconsistent billing — wrong amounts, missing details, random follow-up timing — creates friction and gives customers a reason to delay.

The businesses with the fewest collection problems tend to be the ones that make payment easy and expectations obvious from day one.

Key Factors That Affect the AR Cycle

These factors determine how fast and smoothly the AR cycle completes:

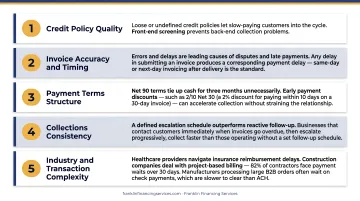

- Credit policy quality: Loose or undefined credit policies let slow-paying customers into the cycle. Front-end screening prevents back-end collection problems.

- Invoice accuracy and timing: Errors and delays are leading causes of disputes and late payments. Atradius's credit management guidance states that any delay in submitting an invoice produces a corresponding payment delay. Same-day or next-day invoicing after delivery is the standard to aim for.

- Payment terms structure: Net 90 terms tie up cash for three months unnecessarily. Early payment discounts — such as 2/10 Net 30 (a 2% discount for paying within 10 days on a 30-day invoice) — can accelerate collection without straining the relationship.

- Collections consistency: A defined escalation schedule outperforms reactive follow-up. Businesses that contact customers immediately when invoices go overdue, then escalate progressively, collect faster than those operating without a set follow-up schedule.

- Industry and transaction complexity: Healthcare providers navigate insurance reimbursement delays. Construction companies deal with project-based billing and contractor payment chains — one 2024 report found 82% of contractors face payment waits over 30 days. Manufacturers processing large B2B orders often wait on check payments, which are slower to clear than ACH. Knowing your industry's typical DSO benchmarks gives you a concrete baseline for setting terms and measuring collections performance.

Common AR Cycle Mistakes and What to Do When Collections Stall

The Most Common Breakdowns

These four mistakes create the majority of AR problems:

- Skipping credit checks : Extending credit to unqualified customers without due diligence puts bad debt into the cycle from day one

- Late or inaccurate invoicing : Delayed invoices delay payment; errors generate disputes that stall collection

- Inconsistent follow-up : Businesses that follow up only when they think about it lose weeks of collection time compared to those with defined escalation schedules

- Ignoring aging reports : Without weekly review, 30-day overdue balances quietly become 90-day problems

The Revenue vs. Cash Flow Trap

Many business owners focus on sales growth while underestimating the AR backlog. A company generating $500,000 in monthly revenue while carrying $400,000 in overdue receivables is cash-constrained, regardless of how the income statement reads. The income statement looks strong; the bank account tells a different story.

When Internal Process Isn't Enough

Even with solid AR practices, some businesses face persistent cash flow gaps — particularly those in industries with long payment cycles (healthcare, construction, manufacturing) or those experiencing rapid growth that outpaces collections.

In these situations, accounts receivable financing provides an alternative. Rather than waiting 60 or 90 days for a customer to pay, a business sells or pledges its outstanding invoices to a financing partner, which advances cash against that invoice value. The business gets working capital now; the financing partner collects from the customer later.

Franklin Financing Services works with small and mid-sized businesses in healthcare, construction, manufacturing, and other industries to close cash flow gaps through AR financing. As an intermediary with relationships across national lenders, Franklin can often find options for businesses that haven't qualified through traditional banks.

Their accounts receivable financing program advances working capital against outstanding invoices, and their free evaluation is a practical starting point for businesses exploring this option.

One practical note on AR financing: costs vary significantly by structure, and understand the full pricing before committing. The Federal Reserve notes that small business financing costs are sometimes quoted as factor rates rather than APR, so asking for a full cost breakdown is a reasonable first step.

Frequently Asked Questions

What is the full cycle of accounts receivable?

The full AR cycle runs from credit evaluation through invoice creation, delivery, payment tracking, collections, cash application, and final reconciliation — ending when payment is collected and recorded on the books.

What are the 4 basic revenue cycles?

The four primary transaction cycles in accounting are the revenue (sales/AR) cycle, the expenditure (purchasing/AP) cycle, the conversion (production) cycle, and the financing cycle. Each cycle tracks a distinct flow of business transactions. The AR cycle is the collections component within the revenue cycle.

What is Days Sales Outstanding (DSO) and why does it matter?

DSO measures the average number of days a business takes to collect payment after a sale. It's calculated as: (Accounts Receivable ÷ Total Credit Sales) × Number of Days. A lower, stable DSO relative to your payment terms indicates healthy, consistent collections.

What happens when customers don't pay on time?

The escalation path runs from automated reminders to direct calls, formal demand notices, collections agency referral, and — if the debt is unrecoverable — a bad debt write-off. At that point, you should also reassess whether to keep extending credit to that customer.

How is accounts receivable different from accounts payable?

AR represents money owed to your business by customers — a current asset. AP represents money your business owes to suppliers — a current liability. They are opposite sides of credit-based transactions.

How can small businesses speed up AR collections?

Invoice immediately after delivery, set clear payment terms upfront, send automated reminders before and after due dates, and offer early payment discounts. For persistent gaps, AR financing lets businesses access outstanding invoice value without waiting for customers to pay.