The core problem: traditional mortgages require move-in-ready properties. A distressed house with deferred maintenance, code violations, or structural issues won't clear conventional underwriting — which is exactly where rehab loans come in.

A rehab loan bundles purchase and renovation costs into one product, underwritten against the property's post-renovation value rather than its current condition. That single structural difference is what makes financing distressed properties possible.

This guide covers every major rehab loan type available to investors, what each one actually costs, who qualifies, and how to pick the right product for your specific strategy — whether you're flipping, house hacking, or building a rental portfolio through BRRRR.

Key Takeaways

- A rehab loan funds both acquisition and renovation, underwritten against after-repair value (ARV) — not the as-is price

- Investor-focused options include hard money, bridge loans, Fannie Mae HomeStyle, and Freddie Mac CHOICERenovation

- FHA 203(k) requires owner-occupancy, making it relevant mainly for house hackers buying 2–4 unit properties

- True cost goes beyond the rate: factor in origination points, draw fees, extension fees, and specialized insurance

- The right loan matches your exit strategy: flip, hold, or house hack

What Is a Rehab Loan and How Does It Work?

A rehab loan is a single financing product covering both the purchase (or refinance) of a property and its renovation costs. The key distinction from a conventional mortgage: the lender underwrites against the after-repair value (ARV) — the estimated market value once work is complete — rather than the current as-is condition.

A property worth $120,000 today but $220,000 post-renovation won't support a conventional loan large enough to justify acquisition. At 70–75% of ARV, a hard money lender can advance enough to make the deal viable — which is precisely why ARV-based underwriting exists.

How the Draw Process Works

Renovation funds aren't handed over at closing. They're held in escrow and released in stages:

- Pay contractors out of pocket to complete a defined milestone

- Request an inspection — lenders typically schedule within 1–2 business days

- Receive reimbursement once the inspection confirms the work is done

- Repeat the cycle for each subsequent project phase

Draw inspection fees commonly run $150–$300 per visit, based on typical lender rate sheets. On a multi-phase renovation, those fees add up — budget accordingly.

Two Broad Categories Investors Encounter

| Category | Products | Primary Use Case |

|---|---|---|

| Renovation mortgages | FHA 203(k), HomeStyle, CHOICERenovation | Owner-occupants; limited investor use |

| Investor-facing products | Hard money, bridge loans | Speed and flexibility over rate |

These categories serve different borrowers entirely. A fix-and-flip investor applying for an FHA 203(k) — which requires owner-occupancy — is disqualified from the start, so knowing which lane applies to your strategy saves wasted applications.

Types of Rehab Loans for Real Estate Investors

The right rehab loan depends on your investment strategy, timeline, and property type. Here's how the main options compare.

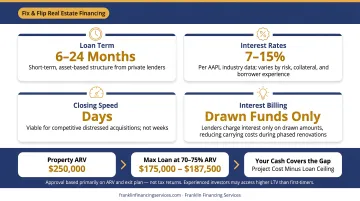

Hard Money / Fix-and-Flip Loans

Hard money loans are the most common investor rehab tool. They're short-term (typically 6–24 months), asset-based products from private lenders where approval hinges primarily on the property's ARV and your exit plan — not your tax returns.

Most hard money rehab lenders cap loans around 70–75% of ARV. So on a property with a $250,000 ARV, you're looking at a maximum loan of roughly $175,000–$187,500. Your cash contribution covers the gap between that ceiling and your total project cost.

Key characteristics:

- Rates: Private lending rates typically range 7–15% depending on risk, collateral, and borrower experience, per AAPL industry data

- Speed: Can close in days, making them viable for competitive distressed acquisitions

- Interest: Lenders often charge interest only on drawn funds — which reduces true carrying costs during phased renovations

- Leverage: Experienced investors often access higher LTV than first-timers; first deals get more conservative terms

The trade-off is real: you pay more for speed and flexibility. But when a conventional lender won't touch the property, the comparison is between hard money and no deal — not hard money versus a 30-year fixed.

Bridge Loans

Bridge loans serve a specific purpose: closing the timing gap between acquisition and permanent financing. They function similarly to hard money but are typically used when an investor needs to move fast and already has a clear path to long-term financing identified.

Common use case: Buy quickly using bridge financing, complete light work to stabilize the property, then refinance into a DSCR loan or conventional product.

AAPL reported a national average bridge loan rate of 10.83% in January 2025, with most rates falling between 9–12%. Terms commonly run 6, 12, or 24 months, with interest-only payments standard.

Choose bridge over hard money when your exit is a known refinance, not a sale — the rate difference matters less than matching the tool to the timeline.

Government-Backed Renovation Loans: FHA 203(k), HomeStyle, and CHOICERenovation

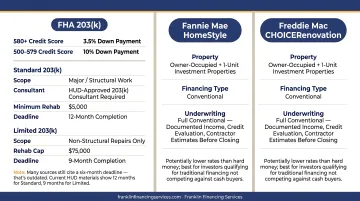

FHA 203(k) is primarily an owner-occupant program — but investors who purchase a 2–4 unit multifamily property and occupy one unit (house hacking) can use it. Key specs per current HUD guidelines:

- 580+ credit score: 3.5% down payment

- 500–579 credit score: 10% down payment

- Standard 203(k): Major/structural work; requires a HUD-approved 203(k) Consultant; $5,000 minimum rehab cost; 12-month completion deadline

- Limited 203(k): Non-structural repairs; capped at $75,000 in rehab costs; 9-month completion deadline

Note: Many sources still cite a six-month deadline — that's outdated. Current HUD materials show 12 months for Standard, 9 months for Limited.

Fannie Mae HomeStyle and Freddie Mac CHOICERenovation are conventional alternatives that do allow one-unit investment properties — a feature that opens conventional-rate financing to investors who'd otherwise default to hard money:

| Product | Investment Property | Completion Window | ADU Work |

|---|---|---|---|

| HomeStyle | Yes (1-unit) | 15 months from closing | Not primary feature |

| CHOICERenovation | Yes (1-unit) | 450 days from Note date | Yes, permitted |

These products offer potentially lower rates than hard money but require full conventional underwriting — documented income, credit evaluation, and contractor estimates submitted before closing. They're best suited to investors who qualify for traditional financing and aren't competing against cash buyers.

HELOC, Cash-Out Refinance, and DSCR Loans

These are tools for investors who already own equity-rich or stabilized properties.

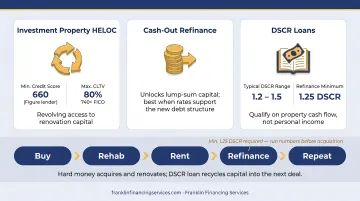

- Investment property HELOC: Revolving access to renovation capital. Lenders like Figure require a minimum 660 credit score for investment properties; Spring EQ's matrix shows maximum CLTV of 80% for 740+ FICO borrowers

- Cash-out refinance: Unlocks lump-sum capital but extends leverage on an existing asset — best when rates support the new debt structure

- DSCR loans: Qualify based on the property's cash flow, not your personal income. Lenders typically require a DSCR of 1.2 to 1.5, though this varies by lender and program

The BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat) connects these tools in sequence: use hard money to acquire and renovate, rent the property, then refinance into a DSCR loan to recycle capital into the next deal. Most lenders require a DSCR of at least 1.25 on the refinance, so run those numbers before you close on the acquisition — not after.

Key Eligibility Requirements by Loan Type

| Loan Type | Credit | Income Documentation | Occupancy | Key Requirement |

|---|---|---|---|---|

| FHA 203(k) | 580+ (3.5% down); 500–579 (10% down) | Full | Owner-occupied | HUD-approved lender; 203(k) Consultant for Standard |

| HomeStyle | No published minimum | Full conventional | Investment OK (1-unit) | Lender must have special Fannie Mae approval |

| CHOICERenovation | No published minimum | Full conventional | Investment OK (1-unit) | Prior Freddie Mac written approval required |

| Hard Money | Flexible / secondary | Minimal | None required | Strong ARV comps, renovation budget, exit plan |

| Bridge Loan | Flexible / secondary | Minimal | None required | Clear timeline to permanent financing |

| DSCR Loan | Typically 660+ | Property cash flow only | Investment | DSCR of 1.2–1.5 depending on lender |

Hard money and bridge loans are asset-based. Lenders care most about:

- ARV supported by comparable sales

- A detailed renovation budget

- A credible exit strategy

- Meaningful equity contribution

First-time investors should expect more conservative leverage and closer scrutiny on all four.

What Does a Rehab Loan Really Cost?

The interest rate is not the same as your total cost of capital. Here's what actually hits your budget:

- Origination points: Charged as a percentage of the loan amount at closing — industry rates vary by lender; get a term sheet before committing

- Draw inspection fees: $150–$300 per inspection, multiple times per project

- Extension fees: If your renovation runs over schedule, lenders charge fees to extend the loan term — these can be significant on large balances

- Insurance: Builder's risk insurance typically costs 1–5% of the total construction budget, and vacant property coverage runs 50–60% above standard homeowner premiums

A Simple Deal Model

Here's a basic framework to calculate your actual cash-to-close:

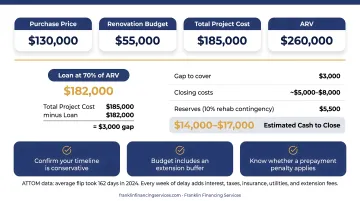

Example deal:

- Purchase price: $130,000

- Renovation budget: $55,000

- Total project cost: $185,000

- ARV: $260,000

- Loan (at 70% of ARV): $182,000

Cash needed:

- Total project cost ($185,000) minus loan amount ($182,000) = $3,000 gap

- Plus closing costs: ~$5,000–$8,000

- Plus reserves (10% contingency on rehab): $5,500

- Estimated cash to close: ~$14,000–$17,000

This example assumes ideal conditions. Real deals often require more equity contribution depending on experience level, property condition, and lender terms.

Equity isn't the only variable that inflates costs — time is just as expensive. ATTOM data shows the average flip took 162 days to complete in 2024, and every week of delay adds interest, taxes, insurance, utilities, and potentially extension fees.

Before you sign, confirm three things: your timeline is conservative, your budget includes an extension buffer, and you know whether a prepayment penalty applies.

How to Choose the Right Rehab Loan for Your Investment Strategy

Match the loan to the deal — not the other way around.

If you're flipping for profit: Hard money or bridge loans are your category. Speed and flexibility matter more than rate when you're competing for distressed inventory that conventional lenders won't finance.

If you're house hacking a multifamily property: FHA 203(k) deserves serious consideration. The lower down payment and longer renovation window (12 months for Standard) make it a strong tool if you're willing to occupy one unit and navigate the documentation process.

If you're buying a single-unit investment property and qualify for conventional financing: HomeStyle or CHOICERenovation may offer a better long-term cost structure — but budget for a slower close and full income documentation. These aren't tools for time-sensitive acquisitions.

If you're building a buy-and-hold portfolio via BRRRR: Use hard money to acquire and renovate, stabilize the property with a tenant, then refinance into a DSCR loan. The exit refinance works when projected rent covers debt service at the required DSCR ratio — underwrite that before you buy, not after.

If you've been turned down by a traditional bank — or you're working with imperfect credit, complex tax returns, or non-traditional income — you still have viable paths forward. Franklin Financing Services connects real estate investors with national lenders across programs including Fix & Flip Financing and Commercial Bridge Loans, with approvals available in 24–48 hours for qualifying deals.

Conclusion

There is no single best rehab loan. The right product depends on your strategy (flip, hold, or house hack), timeline, exit plan, and financial profile. Defaulting to the most familiar option — or the one your last lender offered — is how investors undercut their own returns.

The more important move is to evaluate your options before you're under contract. Lender relationships and pre-qualification work are a competitive advantage, especially in markets where distressed inventory moves fast.

The right financing structure depends on three factors: your deal type, your exit timeline, and what you can qualify for today.

Franklin Financing Services works as a financing intermediary with access to multiple national lenders — which means they can match your deal to the right product, not just the one a single bank happens to offer. If traditional financing hasn't worked out, or you want to compare structures before going under contract, reach out for a no-pressure evaluation. They work with real estate investors at all experience levels, including those with credit challenges or prior bank turndowns.

Frequently Asked Questions

How do you get a loan for a rehab house?

Identify the property and get an ARV estimate from comparable sales. Then choose the appropriate loan type based on your strategy and qualifications. Apply with supporting documentation — typically a renovation budget, contractor estimates, purchase contract, and an exit strategy.

How much down payment is needed for a rehab loan?

FHA 203(k) requires 3.5% down for borrowers with 580+ credit scores, or 10% for scores between 500–579. Hard money lenders work differently: your cash contribution covers the gap between their ARV-based loan cap (typically 70–75% of ARV) and your total project cost. True 100% financing is rare and comes with significant trade-offs.

How difficult is it to get a 203(k) loan?

It's a document-heavy process. You need an FHA-approved lender, a HUD-approved 203(k) Consultant for the Standard version, contractor plans, and firm occupancy intent. Many sellers and agents are cautious accepting offers contingent on this financing due to its longer timeline and complexity.

What is after-repair value (ARV) and why does it matter for rehab loans?

ARV is the estimated market value of a property after renovations are complete. Hard money lenders cap loan amounts at 70–75% of ARV rather than the as-is value, which is what makes financing a distressed property possible. Your ARV estimate must be supported by real comparable sales.

Can I get a rehab loan with bad credit?

Hard money and bridge loans are asset-based and typically have flexible or minimal credit requirements — making them accessible even with imperfect credit. FHA 203(k) and conventional products (HomeStyle, CHOICERenovation) have defined credit thresholds that must be met. Matching your borrower profile to the right loan type is the most practical path forward.

What is the difference between a rehab loan and a construction loan?

Rehab loans fund the purchase and renovation of an existing structure. Construction loans finance new builds from the ground up — they typically require approved plans and permits before funding, and draw down a credit line as construction progresses. HUD's 203(k) program, for example, applies specifically to properties at least one year old, not new construction.