Traditional bank loans aren't built for this. Their approval timelines stretch weeks, their eligibility criteria exclude distressed properties, and their documentation requirements assume you have months to spare. Many real estate investors find themselves shut out right when they need capital most.

This guide breaks down exactly how a bridging loan works for property flippers — from application through repayment — so you can evaluate whether it's the right tool for your next deal.

Key Takeaways

- Bridging loans are short-term, asset-secured loans giving property flippers fast access to capital

- Loan terms typically run 6–18 months, with repayment from property sale proceeds or a refinance

- Conditional approval can be issued in 24–48 hours, with funding available within days

- Lenders focus primarily on the property's value and your exit strategy — not your credit score

- A clear, documented exit strategy is non-negotiable before any funds are released

What Is a Bridging Loan?

A bridging loan is short-term financing that covers the gap between an immediate acquisition or renovation need and a longer-term solution: either a sale or a permanent refinance. For flippers, it solves a specific problem: conventional mortgage lenders won't touch distressed or uninhabitable properties, and their approval timelines are far too slow for competitive acquisition windows.

What a Bridging Loan Is Not

These distinctions matter because the terms get conflated in practice:

- Not a traditional mortgage — repayment terms run months, not decades

- Not a personal loan — it's secured against the property

- Not the same as a fix-and-flip loan — fix-and-flip loans bundle acquisition and renovation costs into one product; bridge loans are general-purpose transitional financing, better suited when the flipper plans to hold or refinance rather than sell immediately

Open vs. Closed Bridge Loans

The structure you choose depends on how certain your exit timeline is:

- Open bridge loans — no fixed repayment date; suited when the sale timeline is uncertain

- Closed bridge loans — repayment date is set, typically when a sale contract is already in place; usually carries better rates because the exit is confirmed

In the US market, most investor bridge loan lenders structure terms around the exit strategy rather than using "open" or "closed" as formal labels. The practical implication is the same: a confirmed sale date gets you better pricing, while an uncertain timeline means more flexibility at a higher cost.

How Does a Bridging Loan Work for Property Flippers?

A bridging loan follows a defined lifecycle. Understanding each stage helps you plan project timelines and model costs accurately before committing.

Application and Pre-Approval

Lenders underwrite primarily against the property's value and the viability of your exit strategy, not an exhaustive income or credit review — which is why the timeline is far more compressed than traditional financing.

What you'll typically need to submit:

- Property details and estimated purchase price

- Scope and budget for planned renovations

- Estimated after-repair value (ARV)

- Your exit strategy — sell or refinance

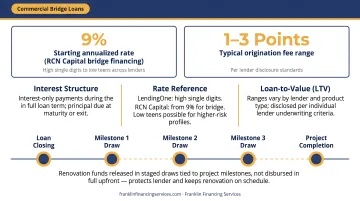

According to RCN Capital, pre-approval determinations can be made in as little as 24 hours, with deals funded in 5–10 business days. Kiavi states qualified investors can close in as few as 7 days.

Loan Structure and Disbursement

Loan-to-value (LTV) ranges vary by lender and product type. Based on lender disclosures from RCN Capital, LendingOne, and Lima One:

| Financing Type | Typical LTV/ARV Ceiling |

|---|---|

| Bridge loans (purchase) | Up to 70% LTV of current property value |

| Fix-and-flip/renovation loans | Up to 75–80% ARV |

| Combined purchase + rehab programs | Up to 95–100% LTC, capped at ARV limit |

Interest structure: Most bridging loans are interest-only during the term. Annualized rates for US investor bridge loans typically run in the high single digits to low teens — LendingOne notes bridge loans often fall in the high single digits, while RCN Capital lists starting rates from 9% for bridge financing. Origination fees commonly run 1–3 points.

For renovation-heavy flips, funds are typically released in staged draws tied to project milestones rather than all upfront. This protects the lender and keeps the renovation progressing on schedule.

The Renovation Phase

Once draws begin, the clock is running. Every week of delay adds to your interest cost and compresses the margin between total borrowing costs and your projected sale price. Tight project management directly determines how much profit survives to closing.

Bridging lenders on renovation projects may require periodic inspections or progress updates before releasing the next draw. Build this coordination time into your project schedule before you accept loan terms.

Repayment and Exit

Property flippers have two primary exit options:

- Sell the renovated property — most common; loan is repaid from sale proceeds at closing

- Refinance into a longer-term product — such as an investment property loan or buy-to-let mortgage, if holding the property

Missing the repayment deadline carries real consequences: higher default interest rates and potential enforcement proceedings. Decide your exit strategy before you draw down the loan, not midway through the renovation.

When Does a Bridging Loan Make the Most Sense?

Not every flip needs a bridge loan. Here are three situations where they're worth every basis point:

Auction purchases. Auction closings in the US are contract-specific and often compressed — Auction.com notes closings can run 30–60 days with time-sensitive deposit requirements. No traditional lender can underwrite and fund within that window. Bridge loans can.

Distressed and uninhabitable properties. Fannie Mae guidelines make conventional financing ineligible for properties with severe structural deficiencies. Bridge lenders evaluate the ARV — the post-renovation value — making deals fundable that banks won't touch.

Competitive acquisitions. NAR reported that all-cash buyers represented 32% of home sales in January 2024, the highest share since 2014. When a motivated seller needs to close fast, bridge financing lets you compete directly with cash buyers.

If your deal fits any of these scenarios, speed and flexibility matter more than rate — and that's exactly where bridge financing has an edge.

Costs and Risks of Bridging Loans

Understanding the Cost Stack

Every cost component must be modeled before you commit. The main components:

- Interest rate — typically annualized in the high single digits to low teens for bridge loans

- Origination/arrangement fees — commonly 1–3 points on bridge loans; 2–5 points on hard-money

- Valuation fees — required to establish the property's current and projected value

- Exit/redemption fees — lender-specific; some charge exit fees, others waive prepayment penalties entirely

What looks modest as individual line items adds up fast on a 6–12 month loan. The 70% Rule gives you a structured way to test whether the deal can absorb those costs and still return a profit.

The 70% Rule as a Sanity Check

Investopedia defines the 70% rule as: pay no more than 70% of ARV minus renovation costs.

Simple example:

- ARV: $300,000

- Renovation costs: $50,000

- Maximum purchase price: ($300,000 × 0.70) − $50,000 = $160,000

At those numbers, you have $90,000 in gross margin to cover borrowing costs, selling costs, holding costs, and profit. A bridge loan that costs $20,000 all-in still leaves meaningful room. When the numbers don't clear this threshold, bridging finance will consume the margin — not just trim it.

Key Risks

- Tight repayment windows — project delays eat directly into profit; ATTOM reported the average time to flip in 2025 was 163 days, leaving minimal buffer in a 6-month term

- Higher overall cost — compared to traditional financing, the all-in cost of a bridge loan can reach 8–15% annualized once fees are included — model it before you sign

- Collateral risk — the property can be repossessed if the loan isn't repaid, so every deal needs a clearly defined exit before funding closes

Tips for Getting Approved and Maximizing Profitability

Run the deal math first. Know your ARV, total renovation budget with contingency, full borrowing costs, and target profit margin before you approach any lender. Borrowers who walk in with documented numbers get better responses.

Strengthen your application:

- Prior flip track record (even 1–2 completed projects helps meaningfully)

- Detailed renovation scope with contractor bids

- Clear, specific exit strategy — lender, timeline, sale price target

First-time flippers can still qualify, but expect tighter LTV ratios until you've demonstrated a track record. If you're struggling to qualify on your own, working with a financing partner gives you access to more options.

Franklin Financing Services offers both Commercial Bridge Loans and Fix & Flip Financing through a network of national lenders, including deals where traditional banks have declined. Their finance specialists can assess your specific deal and match you with appropriate lending partners. Start with a free evaluation at franklinfinancingservices.com/contact.php.

Treat the loan term as a hard deadline. Build your renovation timeline backward from the repayment date. Add contingency for contractor delays, permit timelines, and inspection scheduling. Then decide if the loan term is workable — before you sign.

Frequently Asked Questions

How much does a bridging loan to flip a property cost?

Costs vary by loan size, term, and lender but typically include an annualized interest rate in the high single digits to low teens, plus origination fees of 1–3 points and potential valuation fees. On a $200,000 loan held for 9 months, total borrowing costs can run $20,000–$35,000 or more. Model every component against projected profit before committing.

What kind of loan is best for flipping houses?

Bridging loans and fix-and-flip loans are the two most common options. Bridge loans suit fast acquisitions and transitional needs; fix-and-flip loans bundle purchase and renovation costs into one product. The right choice depends on how much renovation your deal involves and whether you plan to sell or hold after the project.

What is the 70% rule in house flipping?

The 70% rule is a quick viability check: pay no more than 70% of the property's ARV minus your estimated renovation costs. It ensures enough margin to cover the purchase price, borrowing costs, selling expenses, and a profit.

Can you get a bridging loan with bad credit?

Bridge lenders weigh the property's value and your exit strategy more heavily than credit scores, making them more accessible than traditional mortgages for borrowers with credit challenges. Better credit can still improve your rate and terms, but it isn't the primary underwriting factor.

What is a typical LTV ratio for a bridge loan?

US bridge loans for investors typically advance up to 70% of the property's current value. Fix-and-flip programs that also finance renovation costs can reach higher LTC percentages, generally capped at 75–80% of the ARV. A larger equity contribution from the borrower typically improves both the rate and approval odds.

How long does it take to get a bridge loan for a property flip?

Conditional approval can often be issued within 24–48 hours, with funding completed in as few as 5–10 business days. Most qualified investors close in 7–14 days, far quicker than the 30–45 days typical of conventional financing.