According to the Brewers Association's 2025 industry data, U.S. craft beer generated $28.0 billion in retail dollar sales and contributed $71.8 billion to the U.S. economy, supported by over 415,000 jobs. Despite market contraction — with 9,578 operating breweries in 2025, down 2.9% from 2024 — craft brewing remains a substantial industry with active lender participation.

This guide covers every major loan type available to brewery owners, what lenders look for, and how to position your application — whether you're launching your first batch or scaling to meet rising demand.

Key Takeaways

- Equipment financing is often the first loan a brewery pursues, with the equipment itself serving as collateral

- SBA 7(a) loans offer up to $5 million for equipment, working capital, real estate, and debt refinancing

- Taproom-model breweries outperformed distribution-focused operations by 1–2 percentage points in the first half of 2025

- Lenders typically want 640+ credit scores, though alternative products exist for scores in the 580s

- Working with a financing intermediary gives you access to 10+ loan types — far more than any single bank can offer

Why Breweries Need Specialized Financing

Breweries don't fit neatly into standard small business lending boxes. The capital structure is unusual: high upfront equipment costs, revenue that lags well behind production, and cash flow gaps caused by ingredient purchasing cycles.

Consider what a brewery faces before opening day:

- Brewing systems, fermenters, and kegging equipment require significant capital before a drop is sold

- Hop contracts are often locked in months before production begins

- Licensing and permits create upfront costs with no corresponding near-term revenue

- Seasonal demand swings create cash flow gaps even for established operations

The Brewers Association reported 529 closures and 430 openings in 2024 — the first year since 2005 that closures exceeded openings nationwide. Rising ingredient costs, tight margins, and capital pressure were cited as key factors. For brewery owners, that means financing structure isn't just a back-office detail — it directly determines whether the business survives its first few years.

Many brewery owners struggle at traditional banks because of startup costs, irregular cash flow, or limited credit history. SBA-backed programs and alternative financing products have since expanded access for craft beverage businesses — giving owners more viable paths than a traditional bank rejection used to allow.

Types of Small Business Loans for Breweries

Different loan products serve different purposes. Choosing the right one depends on your stage of business, funding amount, timeline, and credit profile. Most established breweries use more than one product simultaneously.

Here's how the main options compare.

SBA 7(a) Loans

The SBA 7(a) program is the most versatile financing option for breweries. Key details:

- Maximum loan amount: $5 million

- Eligible uses: Equipment, working capital, real estate acquisition, leasehold improvements, and debt refinancing

- Repayment terms: Up to 10 years for equipment and working capital; up to 25 years for real estate

- Structure: Government-backed, with competitive rates and no balloon payments

Franklin Financing Services holds a Preferred Financial Services designation with SBA lenders under the 7(a) program, which enables faster and more efficient loan processing than many other channels. For breweries under a deadline to close on equipment or lock in a space, that processing speed can be the difference between moving forward and losing the deal.

SBA 504 Loans

The SBA 504 program targets major fixed-asset purchases — an ideal fit for breweries acquiring a building or installing large-scale production infrastructure. Key details:

- Maximum loan amount: $5.5 million

- Eligible uses: Land, building purchase or construction, long-term machinery with at least a 10-year useful life, facility modernization

- Repayment terms: 10-, 20-, and 25-year maturities available

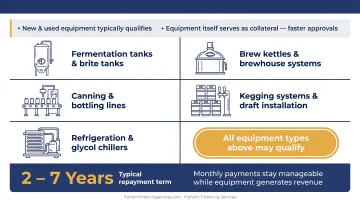

Equipment Financing

Equipment loans are often a brewery's first financing product, and for good reason. The brewing equipment itself serves as collateral, which makes approval faster and more accessible than most other loan types.

What you can finance:

- Fermentation tanks and brite tanks

- Brew kettles and brewhouse systems

- Canning and bottling lines

- Kegging systems and draft installation

- Refrigeration and glycol chillers

Both new and used equipment typically qualify. Repayment terms generally run 2 to 7 years, keeping monthly payments manageable while the equipment generates revenue.

Business Lines of Credit and Working Capital Loans

A revolving business line of credit gives breweries flexible, on-demand access to funds — with interest charged only on what's drawn. Common uses:

- Seasonal ingredient purchasing

- Payroll gaps during slow periods

- Unexpected equipment repairs

- Marketing and promotional campaigns

Working capital loans are shorter-term solutions for day-to-day operational needs. They approve faster than SBA loans, often in 24–48 hours, and some products require no hard collateral. That matters for breweries whose balance sheets are tied up in tanks and kegs rather than real property.

Franklin Financing Services offers Business Term Loans from $20,000 to $500,000 with a Fast Track option that funds in as little as 3 days, requiring only an application and four months of bank statements.

Term Loans and Revenue-Based Financing

Traditional term loans (lump sum, fixed repayment schedule, 2–10 year terms) work well for one-time large expenses: a major expansion, additional production capacity, or a second location.

Revenue-based financing takes a different approach — repayments scale as a percentage of monthly sales (typically 3–9%), which means payments shrink during slow months and increase during strong ones. This structure fits breweries with consistent but seasonal revenue. Franklin Financing Services offers this product ($50K–$1M) for qualifying business owners, including women-owned, veteran-owned, minority-owned, LGBTQ+-owned businesses, and companies in low-to-moderate income areas.

What You Can Use a Brewery Business Loan For

Brewery financing applies across the full business lifecycle, from pre-launch to multi-location expansion.

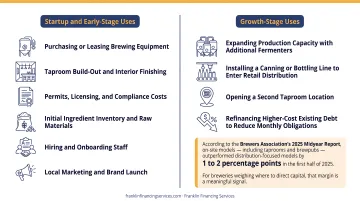

Startup and early-stage uses:

- Purchasing or leasing brewing equipment

- Taproom build-out and interior finishing

- Permits, licensing, and compliance costs

- Initial ingredient inventory and raw materials

- Hiring and onboarding staff

- Local marketing and brand launch

Growth-stage uses:

- Expanding production capacity with additional fermenters

- Installing a canning or bottling line to enter retail distribution

- Opening a second taproom location

- Refinancing higher-cost existing debt to reduce monthly obligations

Of those growth-stage investments, taproom build-outs carry particularly strong financial backing. According to the Brewers Association's 2025 midyear report, on-site models — including taprooms and brewpubs — outperformed distribution-focused models by 1 to 2 percentage points in the first half of 2025. For breweries weighing where to direct capital, that margin is a meaningful signal.

How to Qualify for a Brewery Business Loan

Credit Score

Most traditional lenders and SBA programs prefer a personal credit score of 640–680 or higher. Equipment lenders and alternative lenders may work with scores in the 580–630 range, though at higher rates.

Franklin Financing Services can work with breweries that have experienced credit challenges, prior bank turndowns, or late payment history — unlike traditional banks that restrict approval to the most creditworthy applicants.

Time in Business

| Lender Type | Minimum Time in Business |

|---|---|

| Traditional banks | 2 years |

| SBA programs | Startups can qualify with strong credit, business plan, and industry experience |

| Equipment lenders | 6–12 months |

| Alternative lenders | 6–12 months |

Revenue and Cash Flow

General small business lending benchmarks suggest:

- Unsecured term loans and lines of credit: $100,000+ in annual revenue (Bank of America public guidelines)

- Secured equipment loans and larger term loans: $250,000+ in annual revenue

Positive cash flow trends and consistent bank statements strengthen any application.

Collateral and Personal Guarantees

| Loan Type | Collateral Requirement |

|---|---|

| Equipment loans | Self-collateralized by the purchased equipment |

| SBA loans | General business lien and personal guarantee above certain thresholds |

| Working capital products | No hard collateral required in many cases |

Documentation Lenders Typically Require

These qualification factors come together in your application package. Lenders will typically request:

- Government-issued ID for all owners

- Business and personal tax returns (2–3 years)

- Recent bank statements (3–6 months)

- Profit and loss statements and balance sheets

- Business plan with financial projections

- Equipment quotes (for equipment-specific loans)

- Lease agreements or letters of intent

Startups should supplement these with pre-sales evidence, taproom lease agreements, or distribution letters of intent to demonstrate viability when financial history is limited.

How to Apply for a Brewery Business Loan: Step-by-Step

Step 1 — Determine Your Funding Need

Before applying, calculate total capital requirements across four categories:

- Equipment and assets — brewing systems, tanks, packaging lines

- Facility costs — lease deposits, build-out, renovation

- Licensing and permits — federal, state, and local approvals

- Operating reserves — cash to cover the first 6–12 months

Add a 15–20% contingency buffer for unexpected costs, then subtract available equity. The result is your borrowing target.

Step 2 — Choose the Right Loan Type

Match the product to the purpose:

- Equipment loan → new brewing system or production line

- SBA 7(a) → multi-purpose expansion, real estate, or larger working capital needs

- Line of credit → seasonal cash flow and recurring operational gaps

- Working capital loan → fast operational needs without pledging collateral

Many breweries use a combination of products — equipment financing for the brewhouse, an SBA loan for real estate, and a line of credit for ingredients.

Step 3 — Gather Your Documentation

Organized, clearly labeled documents speed up approval significantly. Core requirements:

- Business plan with financial projections

- 2–3 years of business and personal tax returns

- Recent bank statements (3–6 months)

- Equipment vendor quotes

- Entity formation documents

- Owner IDs

- Lease agreements or real estate contracts

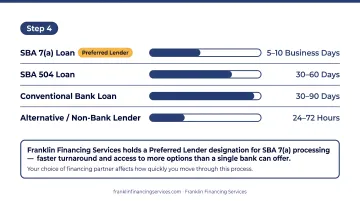

Step 4 — Submit and Receive Approval

Approval timelines vary by loan type:

| Loan Type | Approval Timeline | Funding Timeline |

|---|---|---|

| Alternative/working capital | 24–48 hours | 3–7 days |

| Equipment financing | 2–5 business days | 1–2 weeks |

| SBA 7(a) | 60–90 days | 30–60 days post-approval |

Your choice of financing partner also affects how quickly you move through this process. Franklin Financing Services works with national lenders across all of these loan types and holds a Preferred Lender designation for SBA 7(a) processing — which means faster turnaround and access to more options than a single bank can offer.

Frequently Asked Questions

How do I get funding for a brewery?

The main pathways are SBA loans, equipment financing, business lines of credit, and alternative working capital lenders. The best route depends on your brewery's stage, credit profile, and what you need the funds for — most owners combine more than one product as they grow.

Can I get a brewery loan with bad credit?

Yes. Equipment loans, revenue-based financing, and certain working capital products are available to borrowers with lower credit scores, though rates will be higher. Financing partners like Franklin Financing Services specialize in finding solutions for breweries turned down by traditional banks.

What can I use a brewery business loan for?

Common uses include equipment purchases, taproom build-outs, ingredient and inventory purchasing, staffing, marketing, expanding production capacity, opening additional locations, and refinancing existing higher-cost debt.

How much does it cost to start a brewery?

Startup costs range from roughly $100,000 for a small nanobrewery to $1M+ for a full production facility with taproom. The major cost categories are equipment, facility build-out, licensing and permits, and first-year operating reserves.

What documents do I need to apply for a brewery loan?

Core requirements typically include:

- Government-issued ID

- Business and personal tax returns

- Recent bank statements

- Business plan with projections

- Vendor quote (for equipment loans)

SBA loans require the most documentation; fast-track working capital products may need only an application and bank statements.

Is taproom or distribution more profitable for a brewery?

Taproom-model breweries generally produce stronger margins than distribution-only operations. Recent Brewers Association data confirmed on-site models outperformed distribution-focused breweries by 1–2 percentage points — meaningful when margins are already tight industry-wide.