Introduction

Getting turned down by a bank is more common than most business owners realize. According to the Federal Reserve's 2024 Report on Employer Firms, only 43% of small business loan applicants received the full amount they sought — and 23% received nothing at all.

For businesses that don't check every box — two years in business, strong credit, substantial collateral — traditional banks often aren't a viable path. Nonbank lenders fill that gap with more flexible requirements, faster decisions, and a wider range of loan structures.

This guide covers 10 nonbank lenders across different loan types, eligibility tiers, and funding speeds, plus how to match the right lender to your specific situation.

Key Takeaways

- Nonbank lenders approve faster and require less documentation than traditional banks — many fund within 24–72 hours

- The 10 lenders here cover term loans, lines of credit, equipment financing, MCAs, microloans, and SBA-backed options

- Some accept credit scores as low as 550 and businesses as young as 3–6 months

- Higher rates are the trade-off for speed and flexible eligibility — factor rates on MCAs can push effective APRs above 100%, sometimes reaching 200% or more

- Working with a financing intermediary gives you access to 16+ loan products through a single application instead of approaching lenders one by one

What Are Nonbank Lenders and Why Do Small Businesses Use Them?

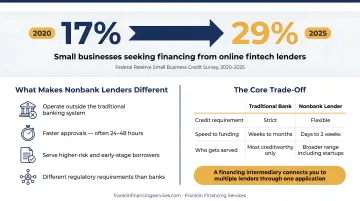

Nonbank lenders are private financing companies — mostly online — that operate outside the traditional banking system. They don't hold deposits and face different regulatory requirements, which lets them serve riskier borrowers and move faster.

The share of small businesses seeking financing from online fintech lenders has grown from 17% in 2020 to 29% in 2025, according to the Federal Reserve's Small Business Credit Survey. That growth reflects real demand from businesses traditional banks decline to serve.

The core trade-off looks like this:

| Factor | Nonbank Lenders | Traditional Banks |

|---|---|---|

| Approval speed | Hours to days | Weeks to months |

| Eligibility | Flexible | Strict |

| Documentation | Minimal to moderate | Extensive |

| Interest rates | Higher | Lower |

| Loan variety | Wide range | Limited |

For businesses that are early-stage, carry imperfect credit, or need capital on a deadline, nonbank lenders are often the only practical option. A financing intermediary can simplify that process by connecting you to multiple nonbank lenders through a single application — rather than approaching each one separately.

10 Nonbank Lenders for Small Business Loans

The lenders below were selected based on loan type diversity, eligibility accessibility, funding speed, and relevance to small and mid-sized businesses.

OnDeck

OnDeck is one of the most widely used nonbank lenders in the U.S., offering short-term loans and revolving lines of credit with same-day funding for applications processed before 10:30 a.m. ET.

It stands out for its loyalty program — repeat borrowers may qualify for a 0% origination fee on renewals — and its ability to fund relatively high loan amounts without requiring excellent credit. One significant caveat: OnDeck's own disclosures show average APRs of 56.4% for term loans and 56.6% for lines of credit (as of mid-2025), so cost comparison matters here.

| Feature | Details |

|---|---|

| Loan Types | Short-term loans, business line of credit |

| Loan Amounts | $5,000–$400,000 |

| Min. Credit Score | 625 FICO |

| Min. Time in Business | 12 months |

Fundbox

Fundbox is built for early-stage businesses, offering a revolving line of credit with a fast automated application that connects directly to accounting software like QuickBooks, FreshBooks, or Stripe.

No origination fees, no prepayment penalties, and funds typically arrive the next business day. The credit limit tops out at $250,000 — lower than most lenders — but the accessibility is unmatched. Note that Fundbox's published time-in-business requirement varies across pages (3–6 months depending on the source); plan for at least 3 months of transaction history.

| Feature | Details |

|---|---|

| Loan Types | Business line of credit |

| Loan Amounts | Up to $250,000 |

| Min. Credit Score | 600 FICO |

| Min. Time in Business | 3–6 months |

Bluevine

Bluevine is a fintech company offering revolving business lines of credit, known for a five-minute application and instant draws for existing Bluevine Business Checking customers.

The revolving structure gives businesses repeated access to funds as they repay, making it well-suited for working capital gaps. One update from current research: Bluevine no longer directly offers invoice factoring — its factoring page now routes to a third-party partner. Also not available in Nevada, North Dakota, or South Dakota.

| Feature | Details |

|---|---|

| Loan Types | Business line of credit |

| Loan Amounts | Up to $250,000 |

| Min. Credit Score | 625 FICO |

| Min. Time in Business | 12 months |

Fora Financial

Fora Financial is a direct working capital lender with a fast, streamlined application process. Approval decisions can come within 4 hours of submitting documentation; funding follows within 24 hours of accepting an offer.

It's a strong option for businesses with lower credit scores or limited history. Pricing uses factor rates rather than APR, which makes cost comparison less intuitive — more on this in the "How to Choose" section below.

| Feature | Details |

|---|---|

| Loan Types | Small business loans, merchant cash advances |

| Loan Amounts | Up to $1,500,000 |

| Min. Credit Score | 570 FICO |

| Min. Time in Business | 6 months |

National Funding

National Funding specializes in fast business funding and equipment financing, with approvals typically within 24 hours and no collateral required for term loans.

Its equipment leasing program includes a Guaranteed Lowest Payment commitment — if a competitor offers a lower payment on a qualifying lease, National Funding pays $1,000 toward the executed lease. This is particularly useful for businesses that need equipment but want payment certainty.

| Feature | Details |

|---|---|

| Loan Types | Short-term loans, equipment financing and leasing |

| Loan Amounts | $5,000–$500,000 (term loans); up to $150,000 (equipment) |

| Min. Credit Score | 600 FICO (new borrowers) |

| Min. Time in Business | 6 months |

Accion Opportunity Fund

Accion Opportunity Fund (AOF) is a nonprofit CDFI (Community Development Financial Institution) serving underserved small businesses, including those owned by women, people of color, veterans, and entrepreneurs in low-to-moderate income areas.

Current term loans go up to $250,000 at rates starting at 9.99%, with terms up to 36 months. No hard credit check for prequalification — AOF focuses on cash flow and business fundamentals rather than score alone. Business coaching is included at no extra cost.

AOF's current eligibility requirements (2 years in business, $300,000 in annual sales) are more stringent than some older sources suggest. Verify current terms directly.

| Feature | Details |

|---|---|

| Loan Types | Small business term loans |

| Loan Amounts | Up to $250,000 |

| Min. Credit Score | Flexible (no hard pull at prequalification) |

| Min. Time in Business | 2 years |

Newtek

Newtek offers SBA 7(a) loans, term loans, lines of credit, and commercial real estate financing. It's unique in combining nonbank accessibility with SBA loan programs — though loans are originated through Newtek Bank, N.A., a bank subsidiary, which matters if pure nonbank status is a priority.

For borrowers, the appeal is SBA loan benefits — longer terms, lower rates, up to $15 million — accessed through a more streamlined process. A strong fit for established businesses that want government-backed terms without traditional bank bureaucracy.

| Feature | Details |

|---|---|

| Loan Types | SBA 7(a), term loans, lines of credit, commercial real estate |

| Loan Amounts | $5,000–$15,000,000 |

| Min. Credit Score | Verified during prequalification |

| Min. Time in Business | 2 years (minimum recommended) |

LendingClub

LendingClub has evolved from its P2P roots into a digital marketplace bank (following the 2021 Radius Bancorp acquisition). Today, it partners with Accion Opportunity Fund to offer small business loans from $5,000–$250,000, plus SBA 7(a) and 504 loans starting at $400,000 through LendingClub Bank.

Businesses that meet AOF's thresholds — at least 12 months in operation and $50,000 in annual sales — will find this a straightforward path to funding.

| Feature | Details |

|---|---|

| Loan Types | Small business loans (via AOF partnership), SBA loans |

| Loan Amounts | $5,000–$250,000 (AOF); $400,000+ (SBA) |

| Min. Credit Score | Flexible (AOF criteria apply) |

| Min. Time in Business | 12 months |

Taycor Financial

Taycor Financial specializes in equipment financing and leasing, offering up to 100% financing with no down payment required. The equipment itself serves as collateral, which lowers qualification barriers for businesses without substantial credit history.

Taycor's FAQ notes that most programs require 2 years in business, though a separate program exists for newer businesses. Application-only financing is available up to $400,000; larger or more complex projects can exceed that.

| Feature | Details |

|---|---|

| Loan Types | Equipment financing and leasing |

| Loan Amounts | $5,000–$400,000+ |

| Min. Credit Score | Not published (varies by program) |

| Min. Time in Business | Typically 2 years; startup program available |

Reliant Funding

Reliant Funding offers merchant cash advances based on future debit and credit card sales, with flexible eligibility suited to businesses with limited credit history or inconsistent revenue. According to Reliant's official FAQ, no minimum credit score is required to apply.

For businesses that can't yet qualify for a traditional loan, Reliant serves as a viable bridge. Daily or weekly automated repayment means cash flow planning is essential — MCA costs can compound quickly.

| Feature | Details |

|---|---|

| Loan Types | Merchant cash advances |

| Loan Amounts | Approximately $10,000–$300,000 |

| Min. Credit Score | None required |

| Min. Time in Business | 6 months |

How to Choose the Right Nonbank Lender

The most common mistake businesses make is applying to the first lender they find — without checking whether the loan type fits their need or whether they actually meet the eligibility criteria.

Match Loan Type to Use Case

- Working capital gaps or payroll: Line of credit (Fundbox, Bluevine, OnDeck)

- Equipment purchases: Equipment financing (Taycor, National Funding)

- Consistent card sales, fast need: MCA (Reliant Funding, Fora Financial, Franklin's Easy Pay)

- Long-term growth capital: SBA 7(a) through Newtek or via Franklin Financing Services

- Underserved ownership categories: AOF, Franklin's Revenue-Based Financing

Match Your Profile to Lender Requirements

Consider these four factors before applying anywhere:

- Credit score — Know your FICO. Applying to a lender whose minimum you don't meet wastes time and can trigger hard pulls

- Time in business — Ranges from 3 months (Fundbox) to 2 years (AOF, Newtek, Taycor)

- Revenue shape — Seasonal businesses should avoid products with fixed daily repayment schedules

- Speed of need — MCAs and short-term loans fund in days; SBA loans take weeks

Understand Total Cost Before Committing

MCA factor rates must be converted to effective APR before comparing against term loan rates. A $50,000 MCA at a 1.4 factor rate means you repay $70,000 total, a $20,000 fee. Spread over a 6-month term, the effective APR can reach 350%, according to NerdWallet.

The Federal Reserve's 2025 SBCS found that 60% of online-lender borrowers reported higher-than-expected borrowing costs, compared to 37% at small banks. Read the terms carefully, convert factor rates to APR, and account for repayment frequency.

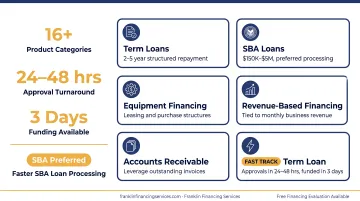

When to Use a Financing Partner

Franklin Financing Services works with a network of national lenders across 16+ product categories — term loans, SBA loans, equipment financing, MCAs, revenue-based financing, accounts receivable, and more. Their SBA Preferred Financial Services designation enables faster SBA loan processing than most channels. Programs like the FAST TRACK Business Term Loan offer approvals in 24–48 hours, with funding in as little as 3 days. For businesses unsure which product they qualify for, a free financing evaluation can save significant time and reduce the risk of applying to the wrong lender.

Conclusion

Nonbank lenders have opened up small business financing to companies that banks routinely decline — startups, businesses with imperfect credit, restaurants, contractors, and healthcare practices. The 10 lenders covered here each serve a different slice of that landscape, from Fundbox for early-stage businesses to Newtek for SBA-backed deals to Reliant for last-resort bridge capital.

The right choice depends on your credit profile, how long you've been in business, what you need the money for, and how fast you need it. If you're unsure where to start, that's where a financing partner can make the difference.

Franklin Financing Services works with businesses across every credit profile — including bank turndowns and early-stage companies. Approvals run 24–48 hours for certain programs, funding arrives in as little as 3–7 days, and no personal guarantee is required on select products. Start with a free financing evaluation to find the right fit.

Frequently Asked Questions

What is the difference between a nonbank lender and a traditional bank for small business loans?

Traditional banks use strict underwriting criteria — credit score, collateral, 2+ years in business — and typically take weeks to fund. Nonbank lenders use more flexible eligibility standards, fund in days, and cover a wider range of business profiles. The trade-off is higher interest rates or fees to offset the added risk.

How much is the monthly payment on a $50,000 business loan?

It depends on rate and term. At 10% APR over 3 years, monthly payments run roughly $1,615. At a higher nonbank rate of 40% APR over 18 months, monthly payments climb to around $3,300. Use an online business loan calculator to model your specific scenario before committing.

Can I get a startup business loan with a 500 credit score?

Options are limited but exist. MCAs from lenders like Reliant Funding require no minimum credit score. Certain nonbank lenders accept scores in the 550–570 range. Revenue-based and invoice-based products may not require a personal credit check at all — qualification depends on business cash flow instead.

What's the easiest small business loan to get?

MCAs and short-term online loans from lenders like Fora Financial or National Funding have the most accessible approval requirements. Fundbox is notable for startup-friendliness — only 3–6 months in business required. Franklin's Easy Pay Cash Advance requires no personal guarantee and accepts poor credit, making it one of the most accessible options on this list.

Can I use my EIN number to get a loan?

Most lenders require both an EIN and a personal credit check, especially for newer businesses. EIN-only lending is rare and generally limited to established businesses with strong commercial credit history. That said, MCAs and revenue-based financing deprioritize personal credit entirely — your business cash flow qualifies you instead.

How fast can you get funding from a nonbank lender?

Many nonbank lenders fund within 24–72 hours after approval, and MCAs can fund same-day or next day. Equipment financing typically takes 1–2 weeks, while SBA-backed products through nonbank channels generally take 1–3 weeks depending on how quickly you can provide documentation.