Introduction

Engineering firms operate in a financial paradox. Projects require significant capital upfront — for staffing, software, equipment, and mobilization — yet payment often arrives weeks or months after work is complete. According to Deltek's 2025 Clarity Architecture & Engineering Industry Study, the median collection period for A&E firms is 73.47 days. That's two-and-a-half months of operating expenses running before a single dollar arrives.

For most firms, this isn't a temporary problem — it's a structural one. The Federal Reserve's 2025 Small Business Credit Survey found that 51% of employer firms cited uneven cash flows as a financial challenge.

The right financing strategy signals operational maturity, not distress. This guide covers:

- The specific cash flow pressures engineering firms face

- Loan products best suited to their billing cycles

- How to qualify and what lenders look for

- How to move from application to funding, including options for firms traditional banks have declined

Key Takeaways

- Engineering firms face structural cash flow gaps tied to project billing cycles — business loans are a practical tool, not a last resort

- Loan options include SBA loans, term loans, lines of credit, equipment financing, and working capital loans — each suited to different needs

- Most lenders require 1–2 years in business, $100K–$250K in annual revenue, and a 600+ credit score

- Alternative and SBA-preferred lenders can approve and fund in as little as 3–7 days

- Proceeds can cover payroll, technology, project bids, expansion, and debt consolidation

Why Engineering Firms Have Unique Financing Needs

The Project-Based Cash Flow Gap

Most engineering firms invoice on milestones or upon project completion — and then wait. With a median collection period of 73+ days across A&E firms, payroll, rent, insurance premiums, and software subscriptions come due long before client payments land.

This creates a recurring gap that compounds over time. A firm juggling three or four active projects can carry $200,000 or more in outstanding receivables while still facing weekly operating costs. Without a financing buffer, firms are forced to delay hiring, defer software upgrades, or pass on new bids entirely.

High Upfront Capital Demands

Winning a contract costs money before any revenue materializes. Common pre-revenue expenses include:

- Bid preparation and proposal development costs

- Professional liability insurance premiums

- Licensing and professional credential fees

- Project mobilization expenses

- Specialized software or equipment purchases

For small and mid-sized firms without large cash reserves, these costs can strain operations before a single hour of billable work is logged.

Growth-Stage Capital Needs

Surviving the pre-revenue phase is only part of the challenge. Firms that want to grow — hiring licensed engineers, expanding to a new region, investing in BIM or advanced CAD platforms, or acquiring a smaller specialty firm — rarely generate enough retained earnings to self-fund that growth at a competitive pace.

The U.S. engineering services industry reached an estimated $360.6 billion in revenue in 2026, according to IBISWorld, with public infrastructure demand driving steady expansion. The firms winning those contracts are the ones with capital ready to deploy — which is exactly where the right financing structure makes the difference.

Types of Business Loans Available to Engineering Firms

The best loan product depends on what the funds are for. Here's how the major options stack up.

Term Loans

Term loans deliver a lump sum repaid over a fixed schedule — typically 1 to 10 years. They work best for defined, high-value investments: acquiring a competitor, opening a regional office, or funding a major technology overhaul.

The main advantage is predictability. Fixed monthly payments make budgeting straightforward, and the loan is fully amortized — no balloon payments, no surprises at maturity. Franklin Financing Services offers conventional fixed-rate term loans from $20,000 to $500,000, with a FAST TRACK option that funds $20,000–$100,000 in as little as 3 days using just an application and four months of bank statements.

Business Lines of Credit

A line of credit is a revolving facility — draw what you need, pay interest only on what you use, and reuse the credit as you repay it. This makes it ideal for managing recurring gaps between project invoicing and client payment.

Think of it as a standing financial cushion rather than a one-time purchase tool — best suited for firms navigating multiple billing cycles simultaneously.

SBA Loans

SBA loans come in two primary forms relevant to engineering firms:

| Loan Type | Max Amount | Best For |

|---|---|---|

| SBA 7(a) | $5 million | Working capital, equipment, acquisitions, expansions |

| SBA 504 | $5.5 million | Real estate, long-term machinery, facility improvements |

SBA 7(a) loans offer broad eligible uses — from working capital to changes of ownership — with longer repayment terms and competitive rates. SBA 504 loans are purpose-built for major fixed assets and cannot be used for working capital or inventory.

For firms where timing is critical, working with an SBA Preferred lender can shorten the process considerably. Franklin Financing Services holds that designation, meaning 7(a) loans can be processed and closed without prior SBA review — cutting weeks off a standard approval timeline.

Equipment Financing

Purpose-built for acquiring specific assets: high-performance CAD workstations, BIM software licenses, drones with LiDAR sensors, testing instruments, or field survey equipment. The equipment itself typically serves as collateral, which often makes qualification easier than unsecured products.

There's also a tax angle worth noting. Under IRS Publication 946, the Section 179 deduction limit is $1,250,000 for tax year 2025, allowing firms to deduct the full cost of qualifying equipment in the year it's placed in service. Leased equipment, by contrast, becomes a deductible operating expense instead of a depreciating asset on your balance sheet.

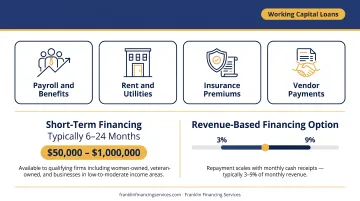

Working Capital Loans

Short-term financing (typically 6–24 months) designed to cover day-to-day expenses during revenue gaps:

- Payroll and benefits

- Rent and utilities

- Insurance premiums

- Vendor payments between project milestones

Revenue-based financing is a related option where repayment scales with monthly cash receipts — typically 3–9% of monthly revenue. Franklin Financing Services offers this product in amounts from $50,000 to $1 million for qualifying firms, including those that are women-owned, veteran-owned, or located in low-to-moderate income areas.

Key Benefits of Business Financing for Engineering Firms

Stabilizing Cash Flow

The most immediate benefit: keeping operations running when client payments are delayed. A line of credit or working capital loan lets a firm meet payroll, pay overhead, and continue project work without dipping into personal funds or halting operations.

With 51% of employer firms reporting uneven cash flows as a challenge, having a pre-arranged credit facility — rather than scrambling for capital mid-crisis — is a meaningful operational advantage.

Investing in Technology That Wins Contracts

Financing enables firms to acquire the platforms that make them competitive on complex, higher-margin work:

- Structural analysis software

- BIM platforms

- Remote inspection tools

- AI-assisted design environments

These aren't optional upgrades — they're often prerequisites for being shortlisted on significant commercial or government projects.

Unlocking Access to Larger Contracts

Federal Acquisition Regulation FAR 9.104-1 requires prospective contractors to demonstrate adequate financial resources to perform the contract, or the ability to obtain them. State DOTs have parallel requirements — Illinois DOT and Missouri DOT both require financial statements as part of consultant prequalification.

A secured line of credit or documented working capital position can determine whether a firm qualifies to bid on public infrastructure work — or gets excluded before the process begins.

Supporting Strategic Growth

Hiring a PE-licensed engineer, opening a second office, or acquiring a specialized competitor requires capital beyond what most firms accumulate from retained earnings alone. Financing makes proactive growth possible without waiting years for profits to build.

The ACEC Research Institute's 2024 Economic Assessment reported engineering and design services grew 5.5% in 2023, driven by public infrastructure demand. Firms with capital to act now stand to capture a disproportionate share of that expanding market.

How to Qualify for a Business Loan as an Engineering Firm

Baseline Criteria

Most lenders evaluate a standard set of factors:

- Time in business: Typically 1–2 years minimum (some alternative products accessible with 6–12 months)

- Annual revenue: Often $100,000–$250,000 minimum; SBA and revenue-based products may require higher thresholds

- Credit score: 600+ is a common floor; scores of 680 or higher typically unlock better terms and lower rates

- Cash flow: Positive and consistent, as evidenced by bank statements and P&L statements

What Lenders Look Beyond Credit Score

Beyond those baseline numbers, underwriters also assess:

- Existing debt obligations and debt-to-net-worth ratios

- Client mix (government vs. private sector clients signal different risk profiles)

- Active project pipeline

- Professional credentials and licensing status

- Specific, documented purpose for the loan

Options for Firms With Imperfect Financials

A prior bank turndown doesn't close the door. Several financing structures are designed specifically for firms that fall outside traditional bank criteria:

- Equipment financing uses the asset itself as collateral, lowering the credit requirement

- Revenue-based financing evaluates monthly cash receipts rather than credit history

- Alternative lenders work with firms that have lower credit scores, limited operating history, or previous rejections

Franklin Financing Services specializes in matching engineering firms to these options — even when traditional banks have already said no.

Documents Typically Required

| Document | When Required |

|---|---|

| 3–6 months of business bank statements | All loan types |

| 1–2 years of business tax returns | Standard and SBA loans |

| Year-to-date P&L statement | Standard and SBA loans |

| Balance sheet | Standard and SBA loans |

| Business plan and financial projections | SBA loans and larger loans |

Having these documents ready before you apply can cut weeks off the approval timeline — lenders often issue conditional approvals pending document receipt, so gaps here are the most common source of delays.

How to Apply for an Engineering Firm Business Loan

The Application Process

The application process is straightforward, whether you're pursuing a short-term working capital line or a multi-million-dollar SBA loan.

- Submit an inquiry — basic firm details, loan amount, and intended purpose

- Consult with a funding specialist — reviews your goals and presents suitable product options

- Submit documentation — underwriting review based on loan type

- Receive a decision — alternative lenders and SBA-preferred providers can approve in 24–48 hours

- Accept the offer and receive funds — qualifying programs fund in as little as 3–7 days

Franklin Financing Services works with engineering firms on loans from $20,000 for working capital up to $5 million for SBA-backed acquisitions or real estate, with terms structured to match the firm's cash flow cycle.

Tips to Strengthen Your Application

A stronger application leads to better terms and faster approvals. Before submitting, consider these steps:

- Maintain a dedicated business bank account separate from personal finances

- Resolve any outstanding tax liabilities before applying

- Document a specific, clear purpose for the loan — vague requests signal risk

- Review business credit reports for errors and dispute any inaccuracies

- Highlight existing client contracts or a strong project pipeline as evidence of repayment capacity

Frequently Asked Questions

How can an engineering firm qualify for a business loan?

Lenders typically assess credit score (600+ minimum for most products), time in business (1–2 years), annual revenue, and cash flow. Firms turned down by traditional banks may still qualify through alternative and specialty lenders like Franklin Financing Services, which use broader eligibility criteria.

What will the monthly payment be for a $100,000 business loan?

Monthly payments depend on the rate and term. At 10% interest over 5 years, a $100,000 loan carries a monthly payment of approximately $2,125, with roughly $27,500 in total interest. For a precise figure based on current rates, consult a lender directly — bank business loan rates ranged from 6.8% to 11% as of June 2026, per NerdWallet.

Can engineering firms with bad credit still get a business loan?

Yes. Equipment financing uses the asset as collateral, reducing the weight lenders place on credit scores. Revenue-based financing evaluates monthly receipts rather than credit history. Specialty lenders serve a broader credit range than traditional banks and don't require strong scores to qualify.

How fast can an engineering firm get funded?

Working capital loans and lines of credit through alternative lenders can be approved in 24–48 hours and funded in 3–7 days. SBA loans and traditional bank loans typically take several weeks, though SBA Preferred lenders like Franklin Financing Services process applications faster than standard channels.

What can business loan funds be used for in an engineering firm?

Common uses include payroll and staffing, CAD/BIM software and hardware, project bidding and mobilization costs, professional liability insurance, office space, business expansion, and debt consolidation.

What is the difference between a business line of credit and a term loan for an engineering firm?

A term loan delivers a lump sum repaid on a fixed schedule — best for defined, one-time investments. A line of credit is revolving: the firm draws what it needs, pays interest only on that amount, and reuses the credit as it repays. Lines of credit are better suited to managing recurring cash flow gaps tied to project billing cycles.