According to the Federal Reserve's 2025 Small Business Credit Survey, roughly 69% of employer firms carried outstanding debt in 2025. And among those businesses, 56% cited paying operating expenses as a challenge — a clear signal that debt strain is widespread, not exceptional.

Debt restructuring addresses this directly. It's not a last resort, and it's not an admission of failure. Used proactively, it's a strategic tool that realigns your obligations with your actual cash flow — before a crisis forces your hand.

This guide covers what restructuring is, how to recognize when you need it, what your options look like, and how to approach the process step by step.

Key Takeaways

- Restructuring modifies existing debt terms — it doesn't add new debt or increase your overall debt load

- Warning signs appear gradually; catching them early preserves more negotiating options

- Multiple paths exist beyond bankruptcy, including consolidation, term extensions, and rate modifications

- Acting before a missed payment gives you far more leverage with creditors

- Working with a financing intermediary opens access to multiple lenders and restructuring options a single bank typically won't provide

What Is Business Debt Restructuring?

Debt restructuring is the process of renegotiating the terms of existing business debt — interest rates, repayment timelines, or the total balance owed — to make those obligations more manageable based on your current financial situation.

That's different from taking on new debt to fund growth. Restructuring works with what you already owe.

The Three Core Mechanisms

Most restructuring falls into one of three categories:

- Refinancing — Replace an existing loan with a new one on better terms (lower rate, longer term, or both)

- Consolidation — Combine multiple debts into a single loan with one monthly payment

- Direct modification — Negotiate changed terms with your current lender without replacing the loan

Federal banking regulators recognize all three approaches as legitimate workout arrangements. The FDIC's interagency policy statement explicitly supports loan accommodations including payment deferrals, partial payments, forbearance, and contract modifications.

Restructuring Isn't Only for Distressed Businesses

Financially healthy businesses restructure debt too. Common proactive reasons include:

- Preparing for a merger or ownership transfer

- Acting on a lower interest rate environment

- Simplifying a complex mix of obligations before raising additional capital

- Freeing cash flow to fund a growth initiative

The SBA's 7(a) loan program explicitly lists refinancing current business debt as an eligible use of proceeds. That alone signals it's a mainstream financial tool, not a last resort.

Warning Signs Your Business May Need Debt Restructuring

Warning signs rarely arrive all at once. They tend to build gradually, which is exactly why many business owners miss them until the situation is already difficult to manage.

Early-Stage Signals

The first signs are usually subtle cash flow friction:

- Monthly debt payments are consuming cash that used to cover inventory or equipment needs

- There's no buffer left for unexpected expenses — a repair, a slow month, or a vendor invoice

- Routine operating costs are being covered by short-term borrowing

When you're borrowing to pay for day-to-day operations rather than growth, that points to a structural problem, not a timing issue.

Behavioral Red Flags

More visible warning signs include:

- Consistently juggling due dates to decide which bill gets paid first

- Using one credit line to service another

- Declining revenue making fixed monthly payments feel increasingly impossible

- Delaying vendor payments to protect cash

- Avoiding financial statements because the numbers are uncomfortable

Any one of these in isolation might be manageable. When two or three appear together, the pattern is clear.

The Timing Risk

Those behavioral patterns above point to a timing problem as much as a financial one. Most business owners wait until payments are missed or loan covenants are violated before addressing the debt — and by that point, your negotiating position has eroded. Creditors who might have willingly modified terms when the business was current become much less flexible once they're managing a delinquent account.

Addressing the problem while payments are still current gives you the leverage to negotiate modified terms, extended repayment schedules, or consolidation options that simply aren't available after a default.

Types of Business Debt Restructuring Options

Understanding your options before you enter any conversation with a lender or financing partner puts you in a much stronger position.

Loan Term Extension

Extending the repayment period reduces the monthly payment by spreading the balance over more time. If you owe $300,000 at 7% and extend from 3 years to 6 years, your monthly obligation drops substantially, freeing cash for operations.

The trade-off: you'll pay more in total interest over the life of the loan. For many businesses, that's an acceptable cost when the alternative is a cash flow crisis.

It's also typically the easiest modification to negotiate with an existing lender, especially if your payment history has been clean.

Interest Rate Modification

A temporary or permanent rate reduction lowers the cost of the debt directly. This works best when:

- The business has a solid payment history

- Revenue has dropped due to a specific, identifiable disruption

- The lender can see a credible path back to normal operations

When making this request, specificity matters. "We had a major client cancel" is more compelling than "business has been tough." Lenders want to understand the situation and believe it's fixable.

Debt Consolidation

Rolling multiple loans, credit lines, or equipment obligations into one loan simplifies repayment and reduces total monthly outflow. Instead of tracking four separate payments with different due dates and interest rates, you manage one.

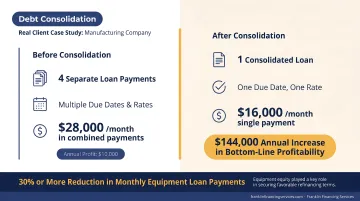

For businesses carrying multiple equipment loans with different maturities, the savings can be significant. Franklin Financing Services' debt consolidation program works by paying off all existing lenders simultaneously and refinancing all equipment into a single loan , a process that can reduce monthly equipment loan payments by 30% or more.

A real example: a manufacturing company carrying $28,000 per month in combined loan payments (generating just $10,000 per year in profit) had all of its obligations consolidated through Franklin Financing Services. Monthly payments dropped to $16,000, translating into a $144,000 annual increase in bottom-line profitability.

The equity built up in the company's equipment played a key role in securing favorable refinancing terms.

Debt-for-Equity Swap

In this arrangement, a creditor receives an ownership stake in your business in exchange for forgiving a portion of the debt. It eliminates payment obligations but costs you equity and some degree of control. This option is more common in larger or more financially distressed businesses, but it's worth understanding if you're evaluating every available path.

Partial Debt Forgiveness / Settlement

When a business is in serious trouble, creditors may agree to accept less than the full balance owed — particularly when a bankruptcy filing is the realistic alternative. Bankruptcy often yields lower creditor recovery than a negotiated settlement, which gives both sides a reason to find middle ground.

This is typically a last resort. To pursue it successfully, you'll generally need to demonstrate:

- Documented proof of financial hardship

- A clear picture of assets, liabilities, and cash flow

- Evidence that a settlement serves both parties better than bankruptcy

How to Restructure Your Business Debt: A Step-by-Step Approach

Step 1 — Audit All Your Debt

Before approaching anyone, build a complete inventory of every obligation:

| Loan | Balance | Interest Rate | Monthly Payment | Maturity Date |

|---|---|---|---|---|

| Equipment loan A | $X | X% | $X | MM/YY |

| Credit line B | $X | X% | $X | Revolving |

Use this as a template — fill in each loan with your actual figures.

Not all debt needs restructuring. The goal is identifying which specific obligations are creating the cash flow strain, so you're solving the right problem.

Step 2 — Calculate What You Can Actually Afford

Work from realistic revenue projections, not best-case scenarios. What can the business genuinely service each month after covering operating expenses? That number determines what you can credibly offer in any negotiation.

Per SBA guidance, lenders assess whether a borrower demonstrates "reasonable ability to repay." If your current cash flow doesn't support that standard, that's useful information — it tells you how urgent the restructuring conversation needs to be.

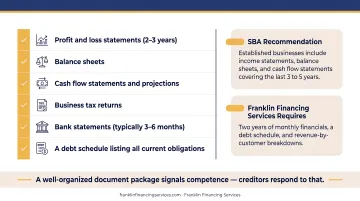

Step 3 — Gather Your Financial Documentation

Creditors require documentation before modifying terms. Expect to provide:

- Profit and loss statements (2–3 years)

- Balance sheets

- Cash flow statements and projections

- Business tax returns

- Bank statements (typically 3–6 months)

- A debt schedule listing all current obligations

The SBA recommends established businesses include income statements, balance sheets, and cash flow statements covering the last 3 to 5 years. Financing intermediaries like Franklin Financing Services typically require two years of monthly financials, a debt schedule, and revenue-by-customer breakdowns.

A well-organized document package signals competence — creditors respond to that.

Step 4 — Prepare a Formal Restructuring Proposal

A written proposal outlining the situation, what the business can realistically pay, and what specific terms you're requesting makes negotiations far more productive than a phone call with vague explanations.

Include:

- What changed and why current terms are unsustainable

- Current cash flow capacity with supporting data

- The specific modification you're requesting (rate, term, payment amount)

- How the business will perform under the new terms

Specific numbers and a clear narrative give creditors something concrete to work with — and a reason to say yes.

Step 5 — Negotiate with Creditors or Work with a Financing Partner

Creditors generally prefer negotiating to losing their investment in a default or bankruptcy. Use that shared interest to anchor your opening conversation.

When direct negotiation stalls — or when credit challenges have already led to bank turndowns — a financing intermediary can expand your options significantly. Franklin Financing Services works with businesses in a wide range of situations, including those with:

- Poor credit history or prior bank rejections

- Complex multi-lender debt structures

- Need for consolidation across multiple obligations

Through its national lender relationships, Franklin Financing Services can identify restructuring solutions that no single bank would offer on its own.

Debt Restructuring vs. Bankruptcy: What SMBs Should Know

These two paths are fundamentally different, and understanding the distinction matters before you're under pressure to choose.

| Debt Restructuring | Chapter 11 Bankruptcy | |

|---|---|---|

| Process | Private negotiation | Court-supervised |

| Public record | No | Yes |

| Speed | Faster | Slower |

| Cost | Lower | Higher (mandatory legal fees) |

| Business relationships | Generally preserved | Often strained |

According to U.S. Courts data, there were 8,408 business Chapter 11 filings in the 12-month period ending June 30, 2025 — a fraction of all business filings, but a significant year-over-year jump.

When Bankruptcy Becomes Relevant

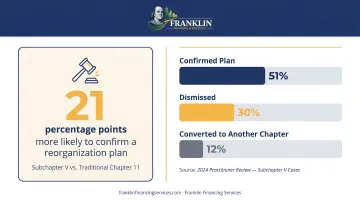

If creditors refuse to negotiate outside of court, Chapter 11 can compel restructuring under judicial oversight. The Subchapter V pathway, designed specifically for smaller businesses, has improved outcomes — one study found Subchapter V cases were 21 percentage points more likely to confirm a reorganization plan than traditional Chapter 11 cases.

Plan confirmation, however, doesn't guarantee survival. A 2024 practitioner review found only about 51% of Subchapter V cases resulted in a confirmed plan — 30% were dismissed and 12% converted to another chapter.

Debts That Can't Be Eliminated

Both restructuring and bankruptcy have limits. Certain debts remain non-dischargeable regardless of the path taken:

- Tax obligations — Certain taxes and customs duties owed to federal and state authorities (11 U.S.C. § 523(a)(1))

- Fraud-related debts — Debts incurred through false pretenses, misrepresentation, or actual fraud (11 U.S.C. § 523(a)(2))

- Fiduciary fraud, embezzlement, or larceny — Debts arising from breach of fiduciary duty or theft

Knowing which debts fall outside any restructuring agreement — or court discharge — shapes what terms are actually achievable at the negotiating table.

Frequently Asked Questions

Is debt restructuring a good idea?

It's a good idea when your cash flow no longer supports current debt obligations, or when proactive term adjustments can strengthen long-term financial stability. It works best alongside an honest assessment of whether the underlying business model is sound — but it can't fix a fundamentally broken operation on its own.

What is the best way to restructure debt?

Start with a complete audit of your existing obligations, then prepare thorough financial documentation. From there, either negotiate directly with creditors or work with an experienced financing partner who can access options beyond what a single lender offers.

What two debts cannot be erased?

In most bankruptcy and restructuring scenarios, certain tax debts owed to the IRS and debts incurred through fraud or intentional misrepresentation are non-dischargeable under federal law. Both must be repaid regardless of what other terms change.

What is the difference between debt restructuring and debt consolidation?

Debt restructuring is the umbrella term for any renegotiation of existing loan terms. Debt consolidation is one specific type of restructuring: combining multiple debts into a single loan to simplify repayment and reduce total monthly obligations.

Does debt restructuring affect my business credit score?

The impact depends on timing and method. Proactive restructuring negotiated before missed payments typically causes less credit damage than a default or bankruptcy filing. Any modification may appear on credit reports, so acting before delinquency sets in is the most effective way to limit the damage.