Introduction

Many small business owners know the pattern all too well: one merchant cash advance to bridge a slow month, a second to cover the first, and suddenly three separate ACH debits are draining the business account every single morning — before payroll, before rent, before anything else.

According to the Federal Reserve's 2025 Small Business Credit Survey, 37% of small employer firms applied for a loan, line of credit, or MCA in the prior 12 months. Among those denied financing in 2024, 41% cited too much existing debt as the reason — up from just 22% in 2021. That debt-burden spiral often starts with a single MCA.

This guide breaks down exactly how MCA consolidation works in practice:

- The four-stage consolidation process, step by step

- Financing options available based on your credit profile

- Red flags to watch for before signing anything

Key Takeaways

- MCAs are structured as revenue purchases, not loans — making them harder to consolidate than standard business debt

- Consolidation combines multiple advances into one repayment, ideally replacing daily ACH debits with a single monthly payment

- The process follows four stages: assess, identify a lender, pay off existing MCAs, and manage new terms

- Options range from SBA 7(a) loans for strong-credit businesses to specialty programs for those banks have turned down

- Consolidation restructures debt, but the cycle can repeat if underlying cash flow habits don't change

What Is a Merchant Cash Advance — and Why Does It Become a Problem?

How MCAs Actually Work

A merchant cash advance provides a lump-sum payment upfront in exchange for a fixed percentage of future receivables. Because it's legally structured as a purchase of future revenue — not a loan — it falls outside many traditional lending regulations and usury caps. That distinction matters more than most business owners realize.

Instead of an APR, MCA providers use a factor rate (typically 1.2 to 1.5). A $50,000 advance at a 1.3 factor rate means you repay $65,000 total, with a fixed percentage debited from your bank account daily or weekly. The Federal Reserve notes that a 1.15 factor rate alone can translate to an estimated 70% APR — and enforcement actions have documented rates reaching far higher.

That cost is difficult to see clearly when all you're looking at is a factor rate.

The Stacking Problem

When daily withdrawals strain cash flow, the obvious move feels like taking out another MCA. Then another. Each new advance carries its own factor rate, withdrawal schedule, and fees — and the combined daily debits compound faster than revenue can keep up. This is MCA stacking — and once multiple advances are running simultaneously, the contract terms buried in each agreement start to matter a great deal.

Structural Risks That Make Default Costly

Two contract clauses make MCA debt particularly dangerous to ignore:

- Confession of judgment (COJ) clauses — allow MCA funders to obtain a court judgment and freeze accounts without advance notice. The FTC has pursued multiple enforcement actions over abusive COJ practices

- Personal guarantees — put the business owner's personal assets on the line if the business can't repay

Both clauses can activate quickly — often before a business owner realizes default is imminent. Consolidating MCA debt into a structured term loan eliminates these exposure points and replaces unpredictable daily debits with a fixed monthly payment.

What Is MCA Consolidation?

MCA consolidation combines multiple outstanding merchant cash advances into a single new financing arrangement — typically a term loan, business line of credit, or in some cases a new MCA-style product — with the goal of simplifying repayment and reducing total cost.

It's worth distinguishing this from refinancing, since the two terms get used interchangeably:

| What It Does | When It Applies | |

|---|---|---|

| Refinancing | Replaces one debt with a new one on better terms | You have a single MCA and want a lower factor rate |

| Consolidation | Combines two or more debts into one | You're juggling multiple MCAs and want a single payment |

That said, consolidation is not debt forgiveness. It restructures what you owe — it doesn't eliminate it. Without addressing the cash flow issues that led to MCA stacking in the first place, consolidation can become a temporary fix that loops back to the same cycle.

How Does Merchant Cash Advance Consolidation Work?

MCA consolidation follows four stages. Each one plays a direct role in whether the restructuring actually reduces your cost burden — or just moves it around.

Stage 1: Assess Your Current MCA Debt Load

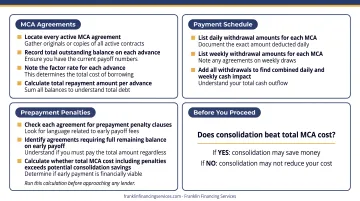

Before approaching any lender, gather every active MCA agreement and calculate:

- Total outstanding balance on each advance

- Factor rate and total repayment amount for each

- Daily or weekly withdrawal amounts across all MCAs

- Whether any agreements include prepayment penalties

Prepayment penalties deserve special attention. Some MCA agreements require the full remaining balance regardless of early payoff — meaning a consolidation loan that doesn't beat the total MCA cost (including penalties) may not actually save money. Run this calculation before you approach a single lender.

Stage 2: Identify a Lender and Loan Type

Lenders evaluating a consolidation application will look at:

- Credit score and credit history

- Time in business

- Monthly revenue and cash flow

- Existing debt obligations and debt-to-income ratio

Businesses with strong financials may qualify for SBA loans or bank term loans at lower rates. Those with lower credit scores or recent bank turndowns need to look at online lenders or specialty financing partners.

Not all lenders handle MCA debt the same way — some pay MCA funders directly, while others disburse funds to the borrower. The direct payoff model is safer, as it eliminates the risk of funds being redirected.

Stage 3: Pay Off Existing MCAs and Activate New Terms

Once approved, the consolidation lender retires the existing MCA balances — eliminating the multiple daily withdrawal schedules. The business then moves to a single repayment structure with the new lender, typically monthly payments.

Instead of three or four ACH debits pulling from the account every morning, the owner makes one predictable payment on a fixed schedule. That operational shift alone makes daily cash flow far easier to track and control.

Stage 4: Manage the New Repayment and Avoid Re-Stacking

Consolidation restructures the debt. What happens next is the business owner's responsibility. Missing payments or taking on additional high-cost advances during the repayment period can undo the benefits and further damage business credit.

This stage is also the best window to build toward lower-cost financing in the future. Consistent on-time payments on the consolidation loan improve credit profile over time. A few habits that protect that progress:

- Avoid new MCAs until the consolidation loan is fully repaid

- Monitor credit score changes quarterly to track improvement

- Work with a financing advisor who can identify lower-cost options as your profile strengthens

Types of MCA Consolidation Options

The right consolidation path depends on credit profile, revenue consistency, and the total MCA debt load. Options range from bank-level products for the most creditworthy to specialty programs for businesses that have been turned down elsewhere.

SBA 7(a) Loans

SBA 7(a) loans can be used to consolidate existing business debt, including MCA obligations. Advantages include:

- Loan amounts up to $5 million

- Repayment terms up to 10 years for working capital, and up to 25 years for real estate

- Lower interest rates than most private lenders (variable-rate caps set by the SBA)

The tradeoff: strong credit, documented financials, and clean personal credit histories are required. Approval timelines are longer than other options. For businesses that qualify, it's the most cost-effective path.

Franklin Financing Services holds a Preferred Financial Services designation from SBA lenders, which enables faster processing than standard SBA lenders.

Business Term Loans

Fixed-rate term loans from banks or online lenders offer predictable monthly payments and clear repayment timelines. The two main sources differ in cost and access:

- Bank term loans carry lower rates but require stronger credit and documented financials

- Online lenders approve faster with more flexible standards, though rates commonly range from 15% to 99% APR depending on risk profile

Franklin's business term loan programs range from $20,000 to $500,000, with a Fast Track option offering approvals in 24–48 hours for amounts up to $100,000.

Business Line of Credit

A revolving line of credit can pay down MCA balances with flexibility — interest accrues only on what's drawn, and repaid funds become available again. This works best for businesses with stable revenue that don't want to lock into a fixed repayment structure.

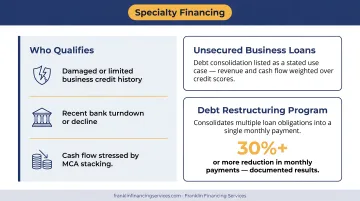

Specialty Financing Partners

Businesses with damaged credit, recent bank turndowns, or financials stressed by MCA stacking often can't qualify for the above options. Specialty financing partners work with national lenders who weigh revenue and cash flow more heavily than credit scores alone.

Franklin Financing Services works in this space directly, connecting businesses to financing solutions even when traditional banks have declined them. Their unsecured business loan program lists debt consolidation as a stated use case, and their debt restructuring program consolidates multiple loan obligations into a single payment, with documented results showing monthly payment reductions of 30% or more.

Reverse Consolidation (Proceed with Caution)

Reverse consolidation is sometimes marketed as a consolidation solution, but it works differently: a new funder advances capital to cover existing MCA payments, leaving the business with one daily payment to the new funder rather than several.

This does not replace existing MCA debt. It adds another layer of high-cost financing on top of what the business already owes, increasing total repayment costs. Reverse consolidation is not a path to stability and should not be confused with true consolidation.

Benefits and Risks of MCA Consolidation

Benefits

- Replaces multiple daily ACH debits with a single monthly payment, immediately reducing administrative friction

- Lowers total borrowing cost when the consolidation rate is meaningfully below the blended MCA factor rates you're currently paying

- Rebuilds business credit through consistent on-time payments on the new loan

- Stops daily account depletion, so operating expenses are covered before debt payments hit

Risks

- A lower monthly payment stretched over a longer term often means paying more in total interest — consolidating $80,000 at 25% APR over 5 years costs more overall than a shorter repayment, even when the monthly figure feels manageable

- MCA stacking often damages the credit profile required to qualify for better consolidation products, making approval harder precisely when it's needed most

- Some lenders market "rescue loans" or "consolidation programs" that are actually reverse consolidations or high-fee products that still pull daily debits

- Before signing, confirm the product replaces ACH debits with fixed monthly payments and discloses a clear APR

Conclusion

MCA consolidation works by replacing multiple high-cost, daily-debit advances with a single structured repayment. The process covers familiar ground: assess the debt load, identify the right lender, pay off existing MCAs, and manage the new terms. What determines success is matching the consolidation product to the business's actual cash flow — not just the one with the lowest factor rate on paper.

Business owners who recognize the warning signs early — multiple daily withdrawals, account balances that barely recover overnight, taking out new MCAs to cover old ones — can consolidate before credit deteriorates further.

Franklin Financing Services helps small businesses across industries evaluate their consolidation options and access financing solutions even when traditional banks have said no. To find out which path fits your situation, reach out for a free financing evaluation.

Frequently Asked Questions

Is merchant cash advance a good idea?

MCAs can work for short-term cash flow emergencies when no other financing is available, but their high factor rates and daily repayment structure make them expensive relative to most alternatives. They become a serious problem when used repeatedly or stacked — which is when consolidation becomes necessary.

What happens if I can't pay back a merchant cash advance?

MCA default can trigger frozen bank accounts, lawsuits, and (where confession of judgment clauses exist) legal action without advance notice — and personal guarantees put the owner's personal assets at risk. Early intervention through consolidation or direct negotiation is far less damaging than waiting until default.

How do I get out of a merchant cash advance?

The main exit paths are consolidating into a lower-cost loan, negotiating with the MCA funder for modified terms or a settlement, or refinancing through a specialty lender. The right option depends on how many MCAs are outstanding and the current state of the business's credit and cash flow.

Is merchant cash advance illegal?

MCAs are legal across most of the U.S. because they're structured as revenue purchases rather than loans, which exempts them from many lending regulations and usury caps. However, states including California, New York, Utah, and Virginia now require cost disclosures, and certain MCA practices (fraudulent terms, unlawful collection tactics) can be legally challenged.

What is the difference between MCA consolidation and refinancing?

Refinancing replaces a single existing MCA with a new one on better terms. Consolidation combines two or more MCAs into one new loan or financing arrangement. If you have one MCA and want better terms, refinancing is the right strategy. Multiple MCAs you want to simplify? That's where consolidation applies.

Can I consolidate MCAs with bad credit or after a bank rejection?

Traditional banks typically require strong credit for consolidation loans. Online lenders and specialty financing partners offer programs that weigh revenue and cash flow more heavily than credit scores alone — making them accessible for businesses with damaged credit or prior bank rejections.