Introduction

Running a church means holding two responsibilities at once: advancing a spiritual mission and managing real money with real accountability. That tension trips up more congregations than most leaders want to admit. A 2021 Church Law & Tax survey of 700+ church leaders found that nearly one-third had served in congregations that experienced financial misconduct.

The stakes are significant. There are roughly 370,000 religious congregations across the United States, and according to Giving USA 2025, Americans gave $146.54 billion to religious organizations in 2024 alone — making religion the single largest recipient category of charitable giving.

Without the right systems in place, that volume of donated funds is difficult to manage — and easy to mishandle.

This guide covers what church leaders actually need:

- How to build a mission-aligned budget

- Setting up proper accounting systems

- Enforcing financial accountability

- Handling donations compliantly

- Maintaining financial transparency

- Knowing when outside financing makes sense

Key Takeaways

- A church budget should reflect ministry priorities, not just cover expenses

- Fund accounting — not standard business accounting — is the right framework for churches

- Separating financial duties across multiple people is essential to prevent fraud and errors

- 73% of churches increased or maintained digital giving adoption in 2023

- Specialized church financing programs exist for congregations that don't qualify for traditional bank loans

Setting Up a Church Budget

A church budget is a written statement of what your congregation values for the coming year. Build it that way — starting from ministry priorities, not historical spending patterns.

Align the Budget with Annual Goals

Start with ministry goals, not numbers. Before a single dollar is allocated, church leadership should gather input from congregation members on priorities: community outreach initiatives, staffing needs, new programs, and mission commitments.

Goals need to be specific enough to attach a dollar figure. "Grow our youth ministry" is too vague. "Hire a part-time youth coordinator and fund a summer camp for 40 students" gives you something to budget against. Every line item should trace back to a defined objective.

Categorize and Analyze Church Expenses

With goals defined, map each one to a spending category. Standard expense categories for churches include:

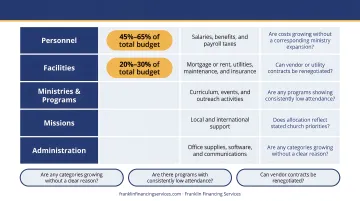

- Personnel — salaries, benefits, and payroll taxes (typically 45%–65% of total budget)

- Facilities — mortgage or rent, utilities, maintenance, and insurance (commonly 20%–30%)

- Ministries and programs — curriculum, events, and outreach activities

- Missions — local and international support

- Administration — office supplies, software, and communications

Review prior-year spending in each category before setting new allocations. A few questions worth asking:

- Are any categories growing without a clear reason?

- Are there programs with consistently low attendance?

- Can vendor contracts be renegotiated?

Build a Financial Reserve Fund

Every church needs a cash cushion. Giving fluctuates seasonally — it dips in summer and surges around the holidays, and emergencies happen. AGFinancial recommends targeting three to six months of operating expenses in reserve.

The practical challenge is getting there. Treat reserve contributions as a non-negotiable budget line — not something funded with whatever is left over. For smaller congregations, building reserves gradually is perfectly reasonable. Even setting aside 2%–3% of income monthly creates meaningful security over time.

Church Accounting Fundamentals

Churches do not account for money the same way businesses do. Where a business tracks profitability, a church tracks accountability — whether each dollar was used for its intended purpose. That difference shapes every financial decision a church makes.

Fund Types Every Church Should Know

Under FASB ASU 2016-14, churches and nonprofits classify resources into two net asset categories:

- Net assets without donor restrictions — funds the church can use for any purpose at its discretion

- Net assets with donor restrictions — funds subject to donor-imposed conditions, either temporary (a gift designated for a specific project, releasable when complete) or perpetual (endowments where only the interest is spent)

Mismanaging restricted funds is not just an accounting error. Spending a donor-designated gift on unapproved expenses is an ethical violation that carries real legal risk. Categorize each gift correctly at the moment it's received — before it ever enters a general account.

Key Financial Documents

The Church Chart of Accounts organizes all financial accounts into five categories: assets, liabilities, net assets, revenue, and expenses. Customize an existing template rather than building from scratch. Overcomplicated structures add maintenance burden without improving clarity.

Churches should produce four core financial statements regularly:

| Statement | What It Shows |

|---|---|

| Statement of Activities | Revenue and expenses over a period |

| Statement of Financial Position | Assets, liabilities, and net assets at a point in time |

| Statement of Cash Flows | Where cash came from and where it went |

| Statement of Functional Expenses | How expenses are allocated across programs and administration |

Tax Obligations

Most churches are exempt from filing Form 990, but that exemption doesn't extend to every compliance requirement. Churches must still:

- Issue W-2s to ministerial and lay employees

- Issue Form 1099-NEC to independent contractors

- File Form 990-T if gross unrelated business income exceeds $1,000

- Follow IRS Publication 517 rules on clergy housing allowance exclusions

State-specific requirements vary, so working with a CPA familiar with church accounting is worth consulting.

Internal Controls and Financial Accountability

Congregants give because they trust their leadership. Internal controls are what make that trust defensible in practice, not just in principle.

Separation of Duties

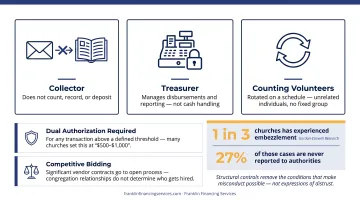

No single person should control the complete financial cycle. The individual who collects offering envelopes should not count, record, or deposit them. The treasurer should focus on disbursements and reporting, not cash handling.

Practical implementation looks like this:

- Rotate counting volunteers — use unrelated volunteers on a rotation so no fixed group controls cash counting

- Require dual authorization for any transaction above a defined threshold (many churches set this at $500–$1,000)

- Use competitive bidding for significant vendor contracts — relationships within the congregation should not determine who gets hired

Gordon-Conwell research reports that 1 in 3 churches has experienced embezzlement, and 27% of those cases are never reported to authorities. Structural controls are not about distrust — they are about removing the conditions that make misconduct possible.

Governance and Accountability Structures

Day-to-day financial management can and should be delegated to a finance committee or qualified staff member. But ultimate authority must remain with the congregation. Significant financial decisions (major expenditures, budget approval, external financing) should be reported to and ratified by the broader membership.

Building that accountability structure requires the right people in the right roles. Church financial leaders should bring both professional competence and demonstrated integrity — not one without the other. The ECFA standard for member organizations requires a governing board of at least five individuals, with a majority independent, meeting no less than twice annually. That structure is a reasonable benchmark for any congregation.

Managing Donations and Diversifying Revenue

Relying entirely on Sunday morning cash and checks creates two problems: fraud risk and income fragility. Digital giving addresses both.

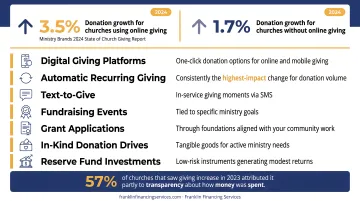

According to Ministry Brands' 2024 State of Church Giving Report, churches using online giving platforms saw a 3.5% increase in donations, compared to just 1.7% for churches without online giving. Automatic recurring donations made up 43% of all transactions in 2023.

Ways to diversify beyond traditional tithes:

- Digital giving platforms with one-click donation options

- Automatic recurring giving — consistently the highest-impact change for donation volume

- Text-to-give options for in-service giving moments

- Fundraising events tied to specific ministry goals

- Grant applications through foundations aligned with your community work

- In-kind donation drives for tangible ministry needs

- Reserve fund investments in low-risk instruments to generate modest returns

Diversifying revenue channels only works alongside donor trust. Ministry Brands found that 57% of churches that saw giving increase in 2023 attributed it partly to being transparent about how money was spent. Donors give more when they can see where their money goes.

Financial Transparency and Reporting

At minimum, churches should share financial reports with the congregation quarterly, with a comprehensive annual review. A standard report should include:

- Income and expense summary for the period

- Progress against budgeted line items

- Reserve fund balance and trajectory

- Any significant variances, with explanation

85% of congregations make their budgets available to participants, according to Lake Institute research — but availability is not the same as proactive communication. Sending a PDF on request is different from presenting a clear summary during a Sunday service or congregational meeting.

Transparent reporting also means staying current on regulatory obligations. Three compliance areas require consistent attention:

- Ministers are generally subject to SECA (self-employment tax), not the employer/employee FICA withholding that applies to most staff

- The clergy housing allowance exclusion under Section 107 is capped at the smallest of three figures: the amount actually spent, the amount officially designated, or the home's fair rental value

- Any income-generating activity not substantially related to the church's exempt purpose may trigger Form 990-T filing obligations under UBIT rules

A qualified CPA with nonprofit or church accounting experience is a practical safeguard, not an optional line item.

When Churches Need External Financing

Even well-managed churches reach moments when internal reserves and donation income cannot cover a major capital need. Building expansions, facility renovations, ministry vehicles, AV infrastructure upgrades — these are legitimate, mission-serving investments that often require external financing.

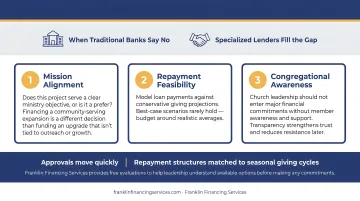

The challenge is that traditional banks frequently decline church applicants. Donation-based income does not fit neatly into standard underwriting models, and many churches lack the conventional credit history or collateral structures that banks require. A bank turndown does not mean financing is unavailable — it means a different lender is needed.

That's where specialized lenders come in. Franklin Financing Services partners with national lenders to connect churches with financing options that traditional banks won't offer — including programs for organizations with limited credit history, non-traditional income structures, or previous bank denials. Approvals can move quickly, and repayment structures can be matched to seasonal giving cycles rather than rigid monthly schedules.

Before committing to any external financing, church leadership should work through three questions:

- Mission alignment: Does this project serve a clear ministry objective, or is it a preference? Financing a community-serving expansion is a different decision than funding an upgrade that isn't tied to outreach or growth.

- Repayment feasibility: Model loan payments against conservative giving projections. Best-case scenarios rarely hold — budget around realistic averages.

- Congregational awareness: Church leadership should not enter major financial commitments without member awareness and support. Transparency strengthens trust and reduces resistance later.

For churches exploring what financing might look like, Franklin Financing Services provides free evaluations to help leadership understand available options before making any commitments.

Frequently Asked Questions

What is the best way to manage church finances?

Set a mission-aligned annual budget, use fund accounting to track restricted and unrestricted funds separately, enforce separation of duties across cash handling and reporting, and share financial summaries with the congregation at least quarterly. Regular review is what keeps any system honest.

Should a pastor be in charge of church finances?

A pastor may provide spiritual oversight of how resources are stewarded, but direct financial management — collecting, counting, disbursing, and reporting funds — belongs with a separate qualified individual or committee. Combining both roles creates conflicts of interest and removes a critical layer of accountability.

What does the Bible say about handling church finances?

Scripture addresses stewardship directly. Luke 16 calls for giving an account of how resources are managed. 2 Corinthians 8:21 instructs that we handle money rightly "not only in the eyes of the Lord but also in the eyes of man." 1 Timothy 5:17–18 affirms that those who serve the church faithfully deserve fair compensation.

What is the 80/20 rule for churches?

The 80/20 principle in church giving refers to the common pattern where roughly 20% of a congregation contributes approximately 80% of total donations. Churches that recognize this pattern are better positioned to invest in generosity education and diversify revenue rather than depending on a small donor base.

What financial reports should a church produce?

Four statements form the core of church financial reporting:

- Statement of Activities

- Statement of Financial Position

- Statement of Cash Flows

- Statement of Functional Expenses

At minimum, the first two should be shared with the congregation annually — quarterly is better.