The numbers back this up. According to BizBuySell's 2025 Year in Review, the median sale price for a small business reached $350,000 in 2025 — and that figure doesn't include post-closing working capital, transition costs, or any deal-related fees. For most buyers, some form of financing isn't optional.

The good news: there are four well-established ways to finance an existing business purchase. Understanding how each one works — and what lenders evaluate — puts you in a much stronger position to close.

Key Takeaways

- Most successful acquisitions blend two or three financing sources, not just one

- SBA 7(a) loans are the most accessible option for small business acquisitions, with down payments as low as 10%

- Seller financing can bridge funding gaps and may count toward your equity injection requirement

- Lenders focus heavily on the business's cash flow, your credit history, and your down payment

- A prior bank turndown doesn't close the door — lenders who specialize in acquisitions often have programs traditional banks won't offer

Why Buying an Existing Business Makes Financial Sense

Starting from scratch means building everything from scratch — customers, processes, and credibility — while burning through capital with nothing coming in.

When you acquire an operating business, you step into:

- Existing cash flow from day one

- Trained employees who know the operation

- Established vendor and supplier relationships

- A customer base that doesn't need to be built from zero

- Historical financials you can actually verify

The higher upfront cost of acquisition is often offset by a much shorter path to profitability. Financing makes this accessible: rather than depleting your savings to cover the full purchase price, you preserve personal cash reserves for post-closing working capital — and that reserve matters as much as the acquisition price itself.

This applies across a wide range of industries — restaurants, franchises, gas stations, convenience stores, healthcare practices, retail stores, and service businesses are all routinely acquired using financing. The four options below cover each of them.

The 4 Ways to Finance the Purchase of an Existing Business

Financing Option 1: SBA Loans

SBA loans — particularly the SBA 7(a) program — are the most widely used financing tool for small business acquisitions in the US. The SBA guarantees a portion of the loan, which reduces lender risk and opens the door for buyers who wouldn't qualify for a conventional bank loan on its own.

Key program details:

- Maximum loan amount: $5 million

- Minimum down payment: 10% of total project costs

- Repayment terms: up to 10 years for most acquisitions (including goodwill and working capital); up to 25 years if real estate is involved

- Proceeds can cover the purchase price, working capital, equipment, and related costs

The lower down payment requirement is particularly important for buyers who want to preserve liquidity post-closing. A 10% injection on a $500,000 acquisition means you're putting in $50,000 — not $100,000 to $150,000 as a conventional bank might require.

For acquisitions involving significant real estate or heavy equipment, the SBA 504 loan is worth considering. It offers fixed interest rates and favorable terms for asset-heavy deals, with a maximum of $5.5 million. One important limitation: the 504 program cannot be used for working capital or goodwill — it's strictly for fixed assets.

Franklin Financing Services holds a Preferred Financial Services designation from SBA lenders, which enables faster loan processing than non-preferred lenders. Their SBA 7(a) program covers acquisitions from $150,000 to $5 million, with no points charged and no balloon payments — a meaningful advantage for buyers managing post-acquisition cash flow.

Financing Option 2: Seller Financing

Seller financing happens when the business owner agrees to accept a portion of the purchase price over time, acting as the lender for that amount. It's more common than many buyers expect — according to BizBuySell, seller financing often carries rates between 8% and 10%, with terms negotiated between buyer and seller.

Why sellers agree to this arrangement:

- It demonstrates confidence in the business's future performance

- It can make the business more attractive to qualified buyers

- It often results in a higher eventual sale price

For buyers, the practical advantages are significant:

- Reduces the amount you need to borrow from a third-party lender

- Can count toward the SBA equity injection requirement (when structured properly — more on this below)

- Gives you a lender who's genuinely motivated to see you succeed

Key terms to negotiate:

- Interest rate and repayment period

- Whether a personal guarantee is required

- Subordination to your senior lender (typically required)

One important SBA rule: for a seller note to count toward your equity injection, it must be on full standby — meaning no principal or interest payments are made on it during the entire life of the SBA loan. This is a common structure in small business acquisitions, but it must be properly documented.

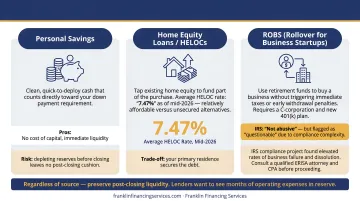

Financing Option 3: Personal Funds and Alternative Sources

Three sources fall under this category, each with distinct tradeoffs:

1. Personal savings The most straightforward equity source. Cash from savings is clean, quick to deploy, and counts directly toward your down payment requirement. The risk: depleting too much liquidity before closing leaves you without a cushion when you need it most.

2. Home equity loans or HELOCs Some buyers tap home equity to fund part of the purchase. Average HELOC rates sat at 7.47% as of mid-2026, making this a relatively affordable option compared to unsecured alternatives. The trade-off is real: you're putting your home on the line.

3. ROBS (Rollover for Business Startups) ROBS allows you to use retirement funds to purchase a business without triggering immediate taxes or early withdrawal penalties. It requires establishing a C-corporation and a new 401(k) plan, then rolling existing retirement funds into it to purchase company stock.

The IRS is clear that ROBS arrangements are not considered abusive tax avoidance transactions — but also flags them as "questionable" due to compliance complexities. The IRS's own compliance project found elevated rates of business failure, bankruptcy, and dissolution among ROBS-funded businesses.

If you're considering ROBS, work with a qualified ERISA attorney and CPA before proceeding.

Whichever personal funding source you use, resist the temptation to go all-in. Most lenders want to see that you'll have enough cash post-closing to cover at least a few months of operating expenses.

Financing Option 4: Private Equity and Investor Funding

Bringing in an outside investor or private equity partner provides acquisition capital without traditional debt — but the trade-off is ownership. Investors typically receive an equity stake and, depending on the deal, may want input on business decisions or a defined exit path.

This option works best when:

- The acquisition price exceeds what SBA or conventional lending can cover

- The buyer wants to reduce monthly debt service obligations

- The business model appeals to investors seeking returns over a defined horizon

For typical main-street acquisitions — restaurants, service businesses, retail stores — private equity involvement is uncommon. Investor expectations around returns often don't align well with owner-operated businesses where the buyer wants full control.

For larger acquisitions ($2M+), or deals where the buyer has limited personal capital and strong deal flow, outside investors can be a legitimate piece of the capital stack. Weigh the reduced debt burden against the long-term cost of diluted ownership before committing.

What Lenders Look For When You Apply for a Business Acquisition Loan

Credit Score and Financial History

Most SBA-approved and conventional lenders look for a personal credit score of 670 or higher, though some SBA programs have flexibility down to around 650. The score itself is only part of the picture — lenders also examine your full credit history, including delinquencies, bankruptcies, and any federal debt obligations.

Business Cash Flow and DSCR

Lenders use the target business's historical financials — typically three years of tax returns and profit-and-loss statements — to calculate the Debt Service Coverage Ratio (DSCR). A DSCR of 1.15 to 1.25 is the standard threshold, meaning the business must generate enough profit to cover loan payments with a reasonable cushion left over.

A business generating $200,000 in annual net operating income with $160,000 in annual debt service has a DSCR of 1.25 — right at the acceptable floor for most lenders.

Down Payment and Liquidity

Most acquisition loans require 10–20% of the purchase price as an equity injection. SBA 7(a) loans sit at the 10% minimum. Conventional bank loans often require 20–30%.

Beyond the down payment itself, lenders check whether you'll have enough cash remaining after closing. Arriving at the closing table with the exact minimum — and nothing left in reserve — is a red flag.

Business Plan and Relevant Experience

Lenders want confidence that you can run and grow what you're buying. A strong acquisition application typically includes:

- A written business plan with realistic financial projections

- Evidence of management or industry experience

- For buyers new to the sector: relevant leadership history or a qualified advisory team

Collateral and Personal Guarantee

Most acquisition loans are secured by the business's assets — equipment, inventory, and real estate if applicable. A personal guarantee from the principal owner is standard across most programs, meaning your personal assets are on the hook if the business defaults.

Some specialty programs may waive this requirement under specific conditions. Ask your lender directly which programs qualify and what documentation is required.

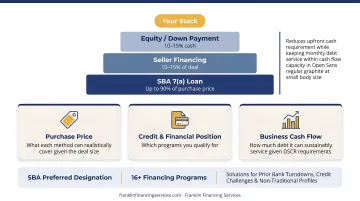

How to Choose the Right Financing Mix

Most successful acquisitions don't rely on a single source. A common structure looks like this:

| Source | Role | Typical Contribution |

|---|---|---|

| SBA 7(a) loan | Primary financing | 80–90% of purchase price |

| Seller note | Secondary layer | 5–15% (on full standby) |

| Buyer cash | Equity injection | 10% minimum |

This layered approach reduces the cash you need upfront while keeping monthly debt service within the business's cash flow capacity.

Before selecting your financing mix, assess three things:

- Purchase price : what each method can realistically cover given the deal size

- Your credit and financial position : which programs you qualify for

- The business's cash flow : how much debt it can sustainably service given the DSCR requirements

A bank rejection doesn't end the search. Franklin Financing Services holds SBA Preferred designation and works with a national lender network across 16+ financing programs — including options for buyers with prior bank turndowns, credit challenges, or non-traditional financial profiles.

Frequently Asked Questions

Is it difficult to get a loan to buy a business?

Difficulty varies significantly by lender type. Traditional banks apply strict credit and collateral requirements that many buyers don't meet. SBA-backed lenders and specialized financing companies like Franklin Financing Services offer more flexibility, including programs for buyers with prior bank turndowns or credit challenges.

How much is the monthly payment for a $100k business loan?

It depends on your rate and term. At a maximum SBA 7(a) variable rate of approximately 12.75%, a $100,000 loan over 5 years runs roughly $2,263/month; over 10 years, that drops to approximately $1,478/month. Actual payments vary based on your specific rate and lender terms.

What is the minimum down payment to buy an existing business?

SBA 7(a) loans require a minimum 10% equity injection of the total project costs. Conventional bank loans often require 20–30%. Seller financing, when structured on full standby, can sometimes be applied toward the required injection.

Can seller financing and an SBA loan be used together?

Yes — this is a common structure in small business acquisitions. The seller note must typically be placed on full standby (no principal or interest paid during the SBA loan term) to count toward the equity injection requirement. The exact structure must meet SBA guidelines, so confirm the details with an experienced loan packaging specialist before finalizing your deal.

What documents do I need to apply for a business acquisition loan?

Core documents typically include:

- Personal and business tax returns (three years)

- Personal financial statement

- Target business's financial statements and P&L

- Signed purchase agreement or letter of intent

- Business plan with financial projections

- Business valuation report (if required)

Your lender may request additional items depending on deal complexity.