Introduction

Heavy construction equipment carries a price tag that stops most small and mid-sized contractors cold. A mid-range excavator can run well into six figures. A crane? Considerably more. Purchasing outright isn't realistic for most construction businesses — and it often isn't even the smartest move financially, even when cash is available.

The real challenge isn't affordability. It's knowing which financing option fits your situation, and avoiding the mistakes that strain cash flow, lock up capital, or leave you unable to bid the next job. Many contractors default to calling their local bank, get turned down or underserved, and assume that's the end of it. That assumption leaves real options on the table. According to the Equipment Leasing and Finance Association (ELFA), 82% of U.S. companies use some form of financing when acquiring equipment — and construction consistently ranks among the most active financing categories, representing 17.5% of ELFA member new business volume in 2024.

This article breaks down the three core financing structures, walks through real-world contractor scenarios, and covers the practices that separate contractors who use financing as a strategic tool from those who simply chase the lowest monthly payment.

Key Takeaways

- 82% of U.S. companies use equipment financing — it's the standard acquisition method, not the exception

- Loans, leases, and rentals each serve a different purpose — picking the wrong structure costs more than the rate difference alone

- Your financing strategy shapes cash flow, bid confidence, and long-term profitability

- Bank rejection doesn't close the door — alternative and specialized lenders evaluate applications differently

- Pre-qualifying before bidding large contracts gives contractors a measurable competitive edge

Understanding Your Construction Equipment Financing Options

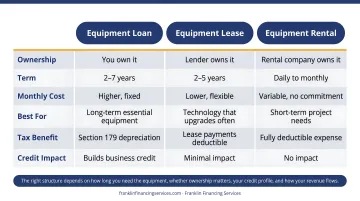

Choosing the wrong financing structure for construction equipment can cost you more than the equipment itself — in unnecessary interest, tax exposure, or cash flow strain. The right fit depends on how long you need the equipment, whether ownership matters to you, your credit profile, and how your revenue flows. Here's how loans, leases, and rentals stack up.

| Option | Best For | Ownership | Upfront Cost |

|---|---|---|---|

| Loan | Long-term, high-value assets | Yes, at payoff | Down payment required |

| Lease | Medium-term or tech-heavy equipment | Optional | Lower than loans |

| Rental | Short-term or one-off needs | No | Minimal |

Loans: Borrow to Own

An equipment loan works simply: a lender provides capital to purchase the equipment, which typically serves as collateral. Once repaid, you own the asset outright.

Loans work best for equipment with strong resale value — excavators, cranes, bulldozers — that you intend to keep or eventually sell. The equity you build matters here. Before committing to a loan, calculate the total cost of ownership (TCO), which goes well beyond the loan payment itself. Per Caterpillar's Performance Handbook methodology, a complete TCO picture includes:

- Fuel and lubricants

- Tire replacement

- Repair reserves

- Insurance and storage

- Operator costs

- Depreciation and eventual resale value

Standard qualification factors include credit score, time in business, annual revenue, and financial documentation such as tax returns and balance sheets. Down payment requirements vary — SBA-backed equipment financing can go as low as 10% down, while used equipment through conventional lenders may require 30–50%.

Leases: Access Without Ownership

Leasing comes in two forms worth understanding:

- Operating leases: You return the equipment at the end of the term with no ownership transfer. Ideal for technology-driven equipment that becomes obsolete quickly.

- Finance (capital) leases: You have the option — or in some cases the obligation — to purchase at end of term. Functions more like a loan from a balance-sheet perspective.

One accounting detail matters here: under FASB Topic 842, leases longer than 12 months require lessees to recognize both the asset and a corresponding liability on their balance sheets. Contractors whose lenders scrutinize financial statements need to account for this before signing.

Leases generally require less upfront capital than loans and carry less stringent credit requirements — making them more accessible for newer businesses or those with limited credit history.

Rentals: Short-Term Flexibility

Rentals are the right tool when you need equipment for less than a year — a one-off contract, a seasonal surge, or a specialized project that won't repeat. The paperwork is minimal and there's no long-term financial commitment.

The tradeoff is cost per period. The U.S. construction rental market hit $80.5 billion in projected 2025 revenue according to the American Rental Association, and rental rates are priced for short-term convenience, not long-term economy. Extend a rental beyond its intended window and the cost can exceed what a lease would have run.

Construction Equipment Financing in Action: Real-World Scenarios

The right financing structure depends on the contractor's situation — their credit profile, cash flow needs, and how long they plan to use the equipment. These three scenarios show how that plays out in practice.

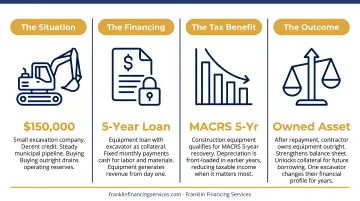

Scenario 1: The Small Contractor Financing a First Excavator

A small excavation company with decent credit and a steady pipeline of municipal work needs a $150,000 excavator. Buying outright would consume most of their operating reserves, leaving almost nothing for labor and materials during the next project cycle.

They pursue an equipment loan with the excavator as collateral. Fixed monthly payments over five years keep cash available for operations while the equipment generates revenue immediately.

The excavator also holds strong resale value. Construction equipment falls under MACRS 5-year recovery for tax purposes, so depreciation is front-loaded in the earlier years — which works in the contractor's favor on paper.

The outcome: After repayment, the contractor owns an asset that strengthens their balance sheet and can be used as collateral for future borrowing. One piece of owned equipment changes their financial profile for years.

Scenario 2: The Mid-Sized Firm Leasing to Stay Current on Technology

A mid-sized general contractor needs GPS-enabled grading equipment. The technology works well today — but it cycles quickly, and ownership of a specific system in five years may mean falling behind competitors using the next generation.

They choose an operating lease. Payments align with project billing cycles, and at the end of the term they can upgrade rather than sell aging equipment into a soft used-equipment market. They never carry obsolete machinery on their books.

The outcome: Capital stays flexible. The firm bids jobs knowing their equipment is current, and they avoid the double cost of owning outdated gear while needing to finance a replacement.

Scenario 3: The Contractor Turned Down by a Bank

A profitable subcontractor wins a large commercial contract requiring a $200,000 skid steer and compactor. Their business generates solid revenue, but their credit history has gaps — some late payments, a thin business credit file. The local bank declines.

They approach a specialized equipment financing partner, get approved in 48 hours, and receive funding within days. The contract gets fulfilled, and the contractor builds a financing track record that opens better terms on future applications.

The result: What felt like a dead end turned into a financing relationship with a partner better suited to the business's profile. Franklin Financing Services specializes in exactly these situations — construction companies with credit gaps, late payment history, or prior bank turndowns — connecting them with national lenders that approve decisions in 24–48 hours.

Best Practices for Securing Construction Equipment Financing

Contractors who use financing well don't just fill out paperwork correctly. They think strategically before they sign anything.

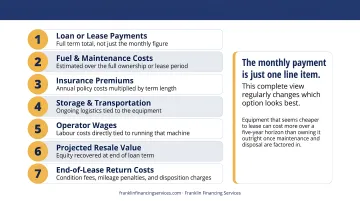

1. Calculate Total Cost of Ownership Before Choosing a Structure

The monthly payment is just one line item — TCO is the full picture. Before deciding between a loan and a lease, add up:

- Loan or lease payments over the full term

- Estimated fuel and maintenance costs

- Insurance premiums

- Storage and transportation

- Operator wages tied to that machine

- Projected resale value (or end-of-lease return costs)

This complete view regularly changes which option looks best. Equipment that seems cheaper to lease can cost more over a five-year horizon than owning it outright once maintenance and disposal are factored in.

2. Align Payment Structures with Project Revenue Cycles

Construction revenue is irregular by nature. A payment schedule built around calendar months may land in your worst cash flow windows. When negotiating financing terms, ask whether the lender can structure payments to match when projects generate income.

Revenue-based financing structures — where payments are a percentage of monthly receipts rather than a fixed dollar amount — work well for contractors with seasonal or project-based income cycles.

3. Match the Loan vs. Lease Decision to Depreciation and Resale

Equipment with strong resale value — cranes, bulldozers, heavy excavators — typically favors a loan. You're building equity in an asset the market will value years from now.

Equipment with rapid technological obsolescence — GPS-integrated machine control, telematics-driven systems — often favors a lease. Owning equipment that's outdated in three years means absorbing depreciation without the benefit of resale value.

4. Read Every Term Before Signing

The monthly payment number is not the deal. The deal includes:

- Total interest paid over the full term

- Early repayment penalties

- What happens if the equipment is damaged or stolen

- Maintenance obligations (some leases require OEM servicing)

- End-of-term options and residual purchase price

A contract that looks affordable at signing can carry penalties, servicing requirements, or residual costs that significantly change the total outlay.

5. Get Pre-Qualified Before Bidding Large Contracts

Knowing your financing capacity before submitting a large bid changes how you approach it. You can commit to equipment needs with confidence rather than scrambling to arrange financing after a win — which creates delays, pressure, and sometimes the wrong deal.

Franklin Financing Services offers free financing evaluations so contractors have a clear picture of their capacity before numbers go on a bid sheet.

What to Do When Traditional Banks Say No

Banks reject construction companies for consistent reasons: credit score thresholds, insufficient operating history, inconsistent revenue documentation, prior delinquencies, or simply being too new. According to the Federal Reserve's 2025 Report on Employer Firms, 24% of applicants received no financing at all, and many more received less than they needed.

A bank rejection means your business didn't fit that lender's specific criteria — not that financing is off the table.

What to explore after a rejection:

- SBA 7(a) loans — Equipment purchases qualify; loans range from $150,000 to $5 million. Franklin Financing Services holds SBA Preferred designation, which speeds up processing compared to standard SBA channels.

- Independent equipment finance companies — Built for construction; evaluate deals most banks won't touch

- Revenue-based financing — Approval is driven by revenue trends and contract history, not credit score alone; suits contractors with recurring project income

- Alternative lenders — Use bank statements, contract history, and business performance rather than pure credit metrics

Working with a financing partner like Franklin Financing Services, rather than a single bank, means one application reaches multiple lenders at once — each with different credit requirements, structures, and terms. That wider reach is often what turns a bank rejection into a funded deal.

How to Choose the Right Construction Equipment Financing Partner

Not every lender that says "yes" to construction financing is the right partner. Evaluate prospective partners on:

- Construction industry experience: Do they understand project cycles, equipment lifecycles, and the difference between a skid steer and a crane?

- Total cost transparency: Can they walk you through what you'll actually pay over the full term — not just the monthly number?

- Access to multiple products: A single-product lender can't adapt when your situation changes. A partner offering loans, leases, SBA, and alternative options can.

- Flexible payment structure: Will they work around your revenue cycle, or does everything have to fit their standard schedule?

Questions to ask any prospective financing partner:

- Do you regularly finance construction companies, or is this occasional?

- Can you show me the full cost of this financing over its entire term?

- If my cash flow fluctuates between projects, how does the payment structure handle that?

- How many lenders are you working with on my behalf?

- What happens if I need to modify the agreement mid-term?

A strong answer to those questions reveals something specific: the partner asked about your business before they started quoting numbers. That's the difference between a lender and an advisor.

Franklin Financing Services works this way — drawing on relationships with national lenders to match construction companies with the right financing structure for their situation, including businesses with credit challenges or prior bank rejections.

Frequently Asked Questions

What credit score is needed to qualify for construction equipment financing?

Requirements vary widely by lender and product. Traditional banks typically require strong credit histories, while alternative lenders and equipment-specific financiers can work with lower scores, prior delinquencies, or thin business credit files. There's no universal threshold — the right starting point is a conversation with a lender who evaluates your full business picture.

How long does the approval process take?

Traditional bank loans often take 30–90 days from application to funding. Specialized and alternative lenders move much faster — some construction equipment financing programs deliver approvals in 24–48 hours and funding within a few days, depending on the lender and product structure.

Is it better to lease or buy construction equipment for a small business?

It depends on three factors: how long you need the equipment, whether it holds resale value, and how your cash flow is structured. Leasing offers lower upfront cost and flexibility to upgrade; buying builds equity in an owned asset. Running a total cost of ownership comparison for your specific equipment and usage pattern will point you toward the right answer.

Can I get financing after being turned down by a bank?

Yes. Alternative and independent lenders evaluate applications using different criteria — revenue trends, contract history, bank statements, and business performance — rather than relying solely on credit score. A bank denial doesn't preclude financing through the right channel.

What documents are typically required to apply?

Common requirements include recent tax returns, several months of bank statements, financial statements, and details about the specific equipment being financed. Alternative lenders often require fewer documents — some programs need only an application and recent bank statements.

Can used construction equipment be financed?

Yes, though not every lender works with used equipment. Those that do will assess the equipment's fair market value and condition to determine how much they'll advance relative to that value. Older or heavily used equipment may require a larger down payment or carry higher rates than new equipment financing.