Introduction

If your SBA 7(a) loan feels like it's working against you — high payments, tight cash flow, terms that no longer fit your business — refinancing may be the fix. It means replacing your existing loan with new financing (either a restructured 7(a) or an SBA 504 loan) to secure better terms and free up capital.

Many business owners assume SBA loans simply can't be refinanced. Others know it's possible but miss a critical detail: there are two distinct regulatory pathways, each with its own eligibility rules, payment tests, and asset requirements. Missing these distinctions leads to premature applications and unexpected denials.

According to SBA.gov, "refinancing current business debt" is an explicitly permitted use of 7(a) loan proceeds. That permission, however, comes with specific conditions that vary by pathway. The governing document is SOP 50 10 Version 8, effective June 1, 2025.

This guide breaks down both pathways, the real eligibility rules (including some commonly misquoted figures), and how the process works from start to close.

Key Takeaways

- SBA 7(a) loans can be refinanced — into a new 7(a) loan or an SBA 504 loan

- For a 7(a)-to-7(a) refinance, the debt must have been current for 12 months (or the life of the loan, whichever is less)

- The 504 pathway requires the debt to be at least 6 months old and secured by eligible fixed assets

- The standard 7(a) refinance requires a 10% reduction in monthly installment payments

- Prepayment penalties on 7(a) loans over 15 years follow a 5%/3%/1% schedule, which differs from the "2% rule" often cited elsewhere

What Does It Mean to Refinance an SBA 7(a) Loan?

Refinancing uses new SBA-guaranteed loan proceeds to pay off an existing debt obligation. The goal is typically to reduce the cost of capital, extend repayment terms, convert from variable to fixed rates, or better align debt structure with current business conditions.

This is distinct from two things borrowers sometimes confuse it with:

- Loan modification adjusts terms with the same lender without issuing new debt. Under SOP 50 10 Version 8, same-lender 7(a) refinancing is only permitted through non-delegated processing in narrow circumstances — for example, when a secondary-market investor prevents modification.

- Debt consolidation is not the same as refinancing in SBA terms. While refinancing can consolidate multiple debts as a secondary outcome, SBA guidelines use the term "debt refinancing" and apply the rules to each debt obligation individually.

Before any refinance can be approved, it must satisfy three SBA thresholds: current-payment standards, payment-benefit tests, and reasonable-terms restrictions.

Your Two Main Options for Refinancing an SBA 7(a) Loan

SOP 50 10 Version 8 permits two refinancing options for existing 7(a) debt. The right choice depends on your collateral type, current debt structure, and long-term financial goals.

Refinancing Into a New SBA 7(a) Loan

A 7(a)-to-7(a) refinance works best when you need to restructure business debt that isn't tied to a specific fixed asset (high-interest business loans, multiple obligations with mismatched maturity dates, or debt carrying unfavorable terms).

Key rules under the current SOP:

- The debt must not already be on reasonable terms — the lender must document why the existing terms justify a refinance

- Existing debt must have been current for at least 12 months, or for the life of the loan if less than 12 months old ("current" means no payment was more than 29 days past due)

- The new installment payment must be at least 10% lower than the existing payment

- Maximum loan amount: $5 million

- Rate structure: fixed or variable; for loans over $350,000, the variable rate cap is base rate plus 3.0% — based on the June 2026 Prime Rate of 6.75%, that cap is 9.75%

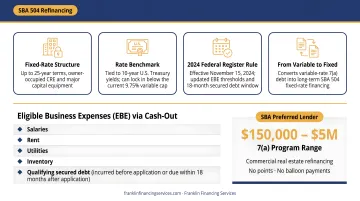

Refinancing Into an SBA 504 Loan

The 504 pathway is designed specifically for fixed-asset debt : owner-occupied commercial real estate and major capital equipment. It converts variable-rate 7(a) debt into a fixed-rate, long-term loan with terms up to 25 years.

Under the 2024 Federal Register direct final rule (effective November 15, 2024), several key thresholds changed:

| Rule | Current Standard |

|---|---|

| Eligible asset test | 75% or more of original proceeds used for fixed assets ("substantially all") |

| Payment benefit test | New installment must be less than existing installment (no 10% minimum) |

| LTV with eligible business expenses | Up to 90% of fair market value of fixed assets |

| EBE cap | Eliminated — no fixed percentage cap |

| Seasoning requirement | Debt incurred and secured by eligible fixed assets for at least 6 months |

Eligible Business Expenses (EBE) that can be accessed through cash-out include: salaries, rent, utilities, inventory, and qualifying secured debt incurred before application or due within 18 months after application.

The fixed-rate structure is the main draw for borrowers currently on variable 7(a) terms. SBA 504 rates are tied to 10-year U.S. Treasury yields, which can lock in rates below the current 9.75% variable cap when Treasury rates run below Prime.

If you're unsure which option fits your situation, Franklin Financing Services can walk through both pathways with you. As an SBA Preferred designation holder, their 7(a) program covers loans from $150,000 to $5 million — including commercial real estate refinancing with no points and no balloon payments.

SBA Eligibility Requirements for Refinancing a 7(a) Loan

Core Requirements

These conditions apply across refinancing pathways:

- Two-year operating history — verified under SOP 50 10 Version 8 for 504 debt refinance without expansion; confirm applicability for your specific scenario with your lender

- Business purpose only — all original loan proceeds must have been used exclusively for eligible business purposes, not personal use

- Debt not on reasonable terms — for 7(a)-to-7(a) refinancing, the existing debt must demonstrably require improvement; debt already carrying favorable terms doesn't qualify

The Substantial Benefit Requirement

The SBA will not approve a refinance that simply shifts risk onto a government-backed loan without meaningfully benefiting the borrower. The tests differ by pathway:

- 7(a) refinance: New installment must be at least 10% lower than the existing payment

- 504 refinance: New installment must simply be lower than the existing payment — no minimum percentage required under current rules

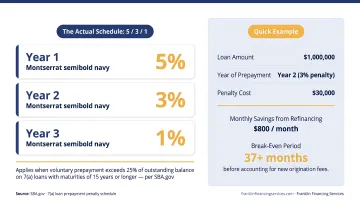

The Prepayment Penalty: What the "2% Rule" Actually Means

The commonly cited "2% rule" is a simplification, and it's often misapplied. According to SBA.gov, 7(a) loans with maturities of 15 years or longer carry prepayment penalties if the borrower voluntarily prepays 25% or more of the outstanding balance within the first three years:

- Year 1: 5%

- Year 2: 3%

- Year 3: 1%

The "2% rule" is a colloquial reference to the year-two penalty — but the actual schedule is 5/3/1. Knowing the full schedule matters when you're refinancing early in a loan's term.

A lower rate doesn't guarantee net savings if penalties and closing costs exceed your monthly payment reduction over the break-even period.

Quick example: On a $1 million 7(a) loan in year two, a voluntary prepayment triggering the penalty would cost $30,000 (3%). If refinancing saves $800/month, you'd need 37+ months just to recover that cost — before accounting for any new origination fees.

How the SBA 7(a) Refinancing Process Works

The refinancing process follows three stages: eligibility review, document preparation, and underwriting. Here's what to expect at each step.

Step 1: Assess Eligibility and Choose a Refinancing Pathway

Evaluate the existing loan against SBA criteria:

- Loan age and current-payment history (12 months for 7(a); 6 months for 504)

- Purpose of original proceeds — were they used for eligible fixed assets?

- Whether the refinance will satisfy the applicable payment-benefit test

- Whether the existing debt is already on "reasonable terms"

This is where working with an experienced SBA lender makes the largest difference. Incomplete eligibility review is the most common cause of application delays. Franklin Financing Services holds a Preferred Financial Services designation through SBA lenders, which enables faster processing at this stage.

Step 2: Gather Required Documentation

Typical documentation for a 7(a) refinance application includes:

- Existing loan note, amendments, and 12-month payment history

- Business and personal financial statements

- Business tax returns (2–3 years)

- Collateral appraisal

- Environmental assessment (if applicable — required for certain property types)

- For 504 refinances: written notice to the existing 7(a) lender at least 10 business days before application, per SOP 50 10 Version 8

Step 3: Submit Application and Complete Underwriting

Once the full document package is submitted, the lender orders any required third-party reports and moves into underwriting. The SBA publishes internal turnaround times of 5–10 business days for Standard 7(a) loans and 2–10 business days for 7(a) Small loans — though overall closing timelines also depend on lender processing and document assembly. Underwriting evaluates:

- Cash flow adequacy to service the new debt

- Collateral value relative to loan amount

- Whether the transaction meets the applicable substantial benefit test

- SBA eligibility across all borrower and loan criteria

Environmental reports must generally be dated within one year of SBA loan number issuance. Appraisals are subject to SBA threshold requirements — confirm current standards with your lender.

Common Mistakes and Misconceptions

Misquoting the Seasoning Requirement

The 6-month rule applies to 504 Qualified Debt — specifically, the commercial loan must be incurred and secured by eligible fixed assets for at least 6 months before application. For a standard 7(a)-to-7(a) refinance, the applicable standard is a 12-month current-payment history (or life of loan if shorter). Applying the wrong rule to the wrong pathway leads to premature applications and avoidable denials.

Getting the seasoning rule wrong isn't the only trap. Borrowers often misread what their existing lender can actually do for them.

Confusing Refinancing with Modification

Some borrowers approach their existing lender expecting to simply adjust their rate or extend their term. Under SOP 50 10 Version 8, same-lender modifications are permitted only in specific situations — and they require non-delegated processing, which many lenders won't pursue.

That's different from a full refinance. If your current lender can't or won't rework the terms, refinancing with a new lender is often the more practical path.

Even when a modification isn't possible, jumping straight to refinancing has its own pitfall: overlooking what the switch actually costs.

Ignoring Prepayment Penalties and Closing Costs

A lower rate doesn't guarantee net savings. Before proceeding, calculate:

- Prepayment penalty on the existing loan (5%/3%/1% in years 1/2/3 for loans ≥15 years)

- New loan origination costs — SBA guaranty fee (1.70%–2.60% of loan amount), appraisal, environmental, and packaging fees

- Monthly payment savings under the new loan

- Break-even point = Total upfront costs ÷ Monthly savings

If your break-even point lands at month 36 but you plan to pay off the loan in 24 months, the rate improvement doesn't justify the upfront cost. Run the numbers before you apply — not after.

Frequently Asked Questions

Can I refinance my SBA 7(a) loan?

Yes. SBA 7(a) loans can be refinanced into a new 7(a) loan or an SBA 504 loan. The transaction must meet eligibility requirements: passing the payment-benefit test, maintaining a current payment history, and not refinancing debt already on reasonable terms.

How soon can you refinance an SBA 7(a) loan?

It depends on the pathway. For a 7(a)-to-7(a) refinance, the debt must have been current for at least 12 months (or the life of the loan if shorter). For a 504 refinance, the qualifying debt must be at least 6 months old and secured by eligible fixed assets for that same period.

What is the 2% rule for refinancing an SBA 7(a) loan?

The "2% rule" is shorthand for the prepayment penalty applied in year two of a 7(a) loan. The actual SBA schedule for loans with maturities of 15 years or longer is 5% in year 1, 3% in year 2, and 1% in year 3 — triggered when 25% or more of the outstanding balance is voluntarily prepaid within the first three years.

What documents are needed to refinance an SBA 7(a) loan?

Core documentation includes the existing loan note and payment history, business and personal financial statements, 2–3 years of tax returns, and a collateral appraisal. For 504 refinances, written notice to the existing lender is required at least 10 business days before application.

Can you get cash out when refinancing an SBA 7(a) loan?

Cash-out is available through the SBA 504 refinancing pathway. Eligible Business Expenses — including payroll, rent, utilities, and inventory — can be funded through the refinance, subject to a combined LTV cap of 90% of the fair market value of fixed assets serving as collateral.

Is it better to refinance into an SBA 504 loan or stay with a 7(a)?

A 504 refinance is the stronger option when the original 7(a) financed owner-occupied real estate or major equipment — you get fixed rates, terms up to 25 years, and potentially lower payments. A 7(a)-to-7(a) refinance fits better when consolidating mixed business debt or when the collateral doesn't meet the 504 program's fixed-asset requirements.